Best Checking Accounts

Based on In-Depth Reviews

A helpful review of checking accounts, their characteristics, and how to select one that benefits you.

Last Updated:July 07, 2026

- 200+Hours of research

- 40+Sources used

- 20Companies vetted

- 3Features reviewed

- 10Top

Picks

Our Team of Researchers:

Our Site is Referenced By

Consumer Advocacy

What you need to know

Checking Accounts

- Online banking has lower fees and higher interest rates

- Some banks have a minimum balance and withdrawal limits

- Choose a bank that offers ATM or service fee refunds

- Test the website to determine its user-friendliness

Our Approach

How we analyzed the best Checking Accounts

Account Features

Fees & Restrictions

Support, Reputation, & Financials

Our list of the best Checking Accounts

State

All States

We receive compensation from these partners

- Additional Companies:

- Ally Bank

- Alliant Credit Union

- Barclays Bank Savings Account

- Sofi Checking and Savings

- Varo

- CIT Bank

- Truist

- SoFi High-Yield Savings

- CIT Bank Platinum Savings

- Key Smart

- UFB Freedom Checking + Savings

- chime-sponsorship

- Capital One

- Chase Bank

- U.S. Bank

- Bank of Internet

- Wells Fargo

- Citibank Priority Account

- Bank5 Connect

- PNC Virtual Wallet Pro

- EverBank

- Bank of America

- USAA Checking Accounts

- Schwab.com

- nbkc Everything Account

- Discover™ Online Savings Account

- Synchrony Bank

- Simple

- BBVA Free Checking

- Axos Bank

- Huntington Personal Checking

- PenFed

- Consumers Credit Union

- BBVA Premium Checking

- Lending Club

- M&T Bank

- Acorns

- Level

- Wealthfront

- BMO Bank

- PNC Virtual Wallet Student

- TD Bank Beyond Checking

- PNC Virtual Wallet®

- Lili

- Quontic

- Upgrade Checking Account

- Axos Bank

- SoFi Plus Checking Accounts

- E*TRADE

- Empower Finance

Don't see the business you are looking for?

Suggest a BusinessSoFi's Disclaimers:

1. Up to $400 Bonus Tiered Disclosure

New and existing Checking and Savings members who have not previously enrolled in Direct Deposit with SoFi are eligible to earn a cash bonus of either $50 (with at least $1,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more) OR $400 (with at least $5,000 total Eligible Direct Deposits received within 25 calendar days of your first Eligible Direct Deposit of $1 or more). Cash bonus amount will be based on the total amount of Eligible Direct Deposit received within 25 calendar days of your first Eligible Direct Deposit of $1 or more. If you have satisfied the Eligible Direct Deposit requirements but have not received a cash bonus in your Checking account, please contact us at 855-456-7634 with the details of your Eligible Direct Deposit. Direct Deposit Promotion begins on 5/15/2026 and will be available through 12/31/26. See full bonus and annual percentage yield (APY) terms at sofi.com/banking/checking-offer/

2. APY disclosures

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 5/28/26.. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet.

3. Fee Policy

We do not charge any account, service, or maintenance fees for SoFi Checking and Savings. We do charge transaction fees for outgoing wire transfers, Instant Transfers, and global remittance transfers. Our fee policy is subject to change at any time. See the SoFi Bank Fee Sheet for details at sofi.com/legal/banking-fees/.

4. Additional FDIC insurance

SoFi Bank is a member FDIC and does not provide more than $250,000 of FDIC insurance per depositor per legal category of account ownership, as described in the FDIC’s regulations. Any additional FDIC insurance is provided by the SoFi Insured Deposit Program. Deposits may be insured up to $3M through participation in the program. See full terms at SoFi.com/banking/fdic/sidpterms. See list of participating banks at SoFi.com/banking/fdic/participatingbanks.

5. ATM Access

We’ve partnered with Allpoint to provide you with ATM access at any of the 55,000+ ATMs in the Allpoint network. You will not be charged a fee when using an in-network ATM, however, third-party fees may be incurred when using out-of-network ATMs. SoFi’s ATM policies are subject to change at our discretion at any time.

6. Early Access to Direct Deposit Funds

Early access to direct deposit funds is based on the timing in which we receive notice of impending payment from the Federal Reserve, which is typically up to two days before the scheduled payment date, but may vary.

7. Overdraft Coverage

Overdraft Coverage is a feature automatically offered to SoFi Checking and Savings account holders who receive at least $1,000 or more in Eligible Direct Deposits within a rolling 31 calendar day period on a recurring basis. Eligible Direct Deposit is defined in the SoFi Bank Rate Sheet, available at https://www.sofi.com/legal/banking-rate-sheet.

Members enrolled in Overdraft Coverage may be covered for up to $50 in negative balances on SoFi Bank debit card purchases only. Overdraft Coverage does not apply to P2P transfers, bill payments, checks, or other non-debit card transactions. Members with a prior history of unpaid negative balances are not eligible for Overdraft Coverage. Eligibility for Overdraft Coverage is determined by SoFi Bank in its sole discretion. Members can check their enrollment status, if eligible, at any time by logging into their account through the SoFi app or on the SoFi.

8. 0.70% Savings APY Boost

Earn up to 3.80% Annual Percentage Yield (APY) on SoFi Savings with a 0.70% APY Boost (added to the 3.10% APY) for up to 6 months. Open a new SoFi Checking & Savings account with Eligible Direct Deposit by 12/31/26. Rates variable, subject to change. Terms apply at sofi.com/banking#2. SoFi Bank, N.A. Member FDIC.

Chime Disclaimers:

*Chime is a financial technology company, not a bank. Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC.

*Terms apply. Click to learn more. Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC.

^Early access to direct deposit funds depends on the timing of the submission of the payment file from the payer. We generally make these funds available on the day the payment file is received, which may be up to 2 days earlier than the scheduled payment date.

**Out-of-network ATM withdrawal and over the counter advance fees may apply except at FCTI® ATMs in a 7-Eleven® or Speedway, or any Allpoint® or Visa® Plus Alliance ATM participating in the Allpoint network.

You can automatically transfer part of your direct deposits of $1 or more from your Checking Account into your selected Chime account(s).

1SpotMe® on Debit is an optional, no fee overdraft service attached to your Chime Checking Account. To qualify for the SpotMe on Debit service, you must receive $200 or more in qualifying direct deposits to your Chime Checking Account each month and have activated your physical Chime Visa® Debit Card or secured Chime Visa® Credit Card. Qualifying members will be allowed to overdraw their Chime Checking Account up to $20 on debit card purchases and cash withdrawals initially but may later be eligible for a higher limit of up to $200 or more based on Chime Account history, direct deposit frequency and amount, spending activity and other risk-based factors. The SpotMe on Debit limit will be displayed within the Chime mobile app and is subject to change at any time, at Chime's sole discretion. Although Chime does not charge any overdraft fees for SpotMe on Debit, there may be out-of-network or third-party fees associated with ATM transactions and fees associated with OTC cash withdrawals. SpotMe on Debit will not cover any non-debit card transactions, including ACH transfers, Pay Anyone transfers, or Chime Checkbook transactions. SpotMe on Debit Terms and Conditions.

Truist Disclaimers

Terms and Conditions for Truist One Checking

2The Balance Buffer is only available with Truist One Checking and allows clients to overdraw their account up to $100. There is no decision required as this feature is automatically available when a client qualifies.

To INITIALLY QUALIFY for the Balance Buffer, the requirements below must be met:

- Account must be opened for a minimum of 35 calendar days

- Account must be funded with a positive balance

- A single direct deposit of at least $100 made within the last 35 calendar days

To REMAIN QUALIFIED for the Balance Buffer, the requirement below must be met:

- A single direct deposit of at least $100 made within the last 35 calendar days. After qualifying, if 35 calendar days pass without a Direct Deposit of at least $100, you will no longer have access to the Balance Buffer.

For accounts that qualify for the Balance Buffer, once the account is overdrawn by $100, additional transactions will typically be declined or returned.

For accounts that qualify for the Balance Buffer and also have Overdraft Protection, Truist will use the Balance Buffer first. If the account has neither, transactions that exceed the account balance will typically be declined or returned.

Truist Bank, Member FDIC. ©2026, Truist Financial Corporation. Truist, Truist Purple and the Truist Logo are service marks of Truist Financial Corporation.

13 People found this helpful.

We receive compensation from these partners, which impacts the order they appear on the page. That said, the analyses and opinions on our site are our own and we believe in editorial integrity.

Our Top Picks: Checking Accounts Reviews

Chime® review

Chime®️ Checking Account Overview:

Chime’s®️ Checking Account is a modern, mobile-first account designed for everyday banking without the hassle of traditional branches. It comes with a Chime Visa® Debit Card and full access through Chime’s intuitive mobile app, making money management easy and accessible from anywhere.

Account Fees:

Chime does not charge monthly maintenance fees, overdraft fees, or minimum balance penalties. However, third-party fees may apply for out-of-network ATM use or cash deposit services at retail locations.

Perks & Benefits:

Chime offers a variety of standout features including early direct deposit (up to two days faster), SpotMe® fee-free overdraft for eligible members1, and access to over 47,000 fee-free ATMs. The account also includes real-time transaction alerts, automatic savings tools, and no foreign transaction fees, all backed by FDIC insurance through partner banks.

Current review

Current Checking Account Overview:

Current makes banking simple with a quick online sign-up process—no credit check required. Your Visa® debit card will arrive within a few business days, and you can start using your account right away. Eligible users can access their paycheck up to 2 days early with direct deposit.

Account Fees:

No monthly fees, no minimum balance requirements, and no overdraft fees. Eligible users can overdraft up to $200 fee-free with Current Overdrive™. Standard transactions, such as ATM withdrawals at in-network locations, are also free.

Perks & Benefits:

Current offers cash back on debit card purchases at participating retailers. Users can also create Savings Pods to organize and grow their savings with competitive interest. The app provides real-time spending insights, instant transaction alerts, and quick money transfers to friends. Plus, with access to over 40,000 fee-free ATMs nationwide, you can withdraw cash without extra charges. All accounts are FDIC-insured up to $250,000 through Choice Financial Group, Member FDIC.

Alliant Credit Union review

Alliant High-Rate Checking Account Overview:

The Alliant High-Rate Digital Checking Account is built for those who want a modern, no-frills approach to managing their money. With a fully digital experience and easy account access through Alliant’s top-rated mobile app, it's a smart choice for everyday banking.

Account Fees:

There are no monthly service fees, no minimum balance requirements, and no overdraft or non-sufficient funds (NSF) fees. Alliant also reimburses up to $20 per month in out-of-network ATM fees when you meet basic account requirements.

Perks & Benefits:

Earn 0.25% APY* on your checking balance when you opt for eStatements and have at least one electronic deposit per month. The account includes contactless debit cards, mobile check deposit, Zelle® transfers, and access to 80,000+ surcharge-free ATMs nationwide.

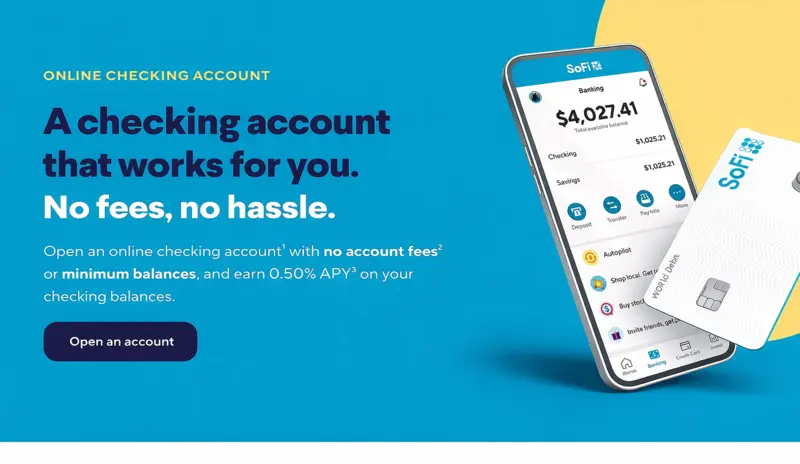

Sofi Checking and Savings review

SoFi Checking & Savings Account Overview:

SoFi Checking & Savings is an all-in-one online banking account with no account fees or minimum balance requirements. Customers can open an account quickly and manage finances through a user-friendly mobile app, with features like early direct deposit and automated savings tools. Deposits are FDIC-insured up to applicable limits, with additional coverage available through SoFi’s extended insurance program.

Account Fees:

There are no monthly maintenance fees, overdraft fees, or minimum balance fees. Customers also get access to 55,000+ fee-free Allpoint® ATMs nationwide. Some fees may apply for select services, such as cash deposits at third-party locations.

Perks & Benefits:

Customers can earn up to 3.30% APY on savings and 0.50% APY on checking with qualifying direct deposit, with lower rates otherwise. Features like savings Vaults, roundups, and recurring transfers help automate saving, while early paycheck access, a large ATM network, and integrated financial tools enhance everyday money management.

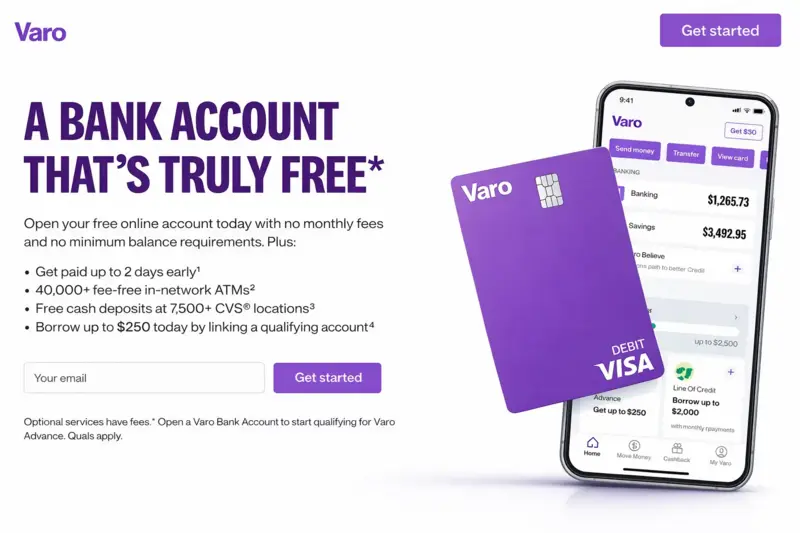

Varo review

Varo Bank Account Overview:

Varo Bank Account is a fully digital checking and savings solution with no minimum opening deposit and a quick mobile sign-up process. As an FDIC-insured national bank, Varo holds deposits directly and provides standard protection up to applicable limits, all within a mobile-first experience.

Account Fees:

Varo has no monthly fees, no minimum balance requirements, and no overdraft fees. Customers also get access to 40,000+ fee-free ATMs nationwide. Cash deposits are available through third-party retailers and may include a fee depending on the location.

Perks & Benefits:

Customers can earn up to 5.00% APY on savings balances up to $5,000 with qualifying direct deposit, with lower rates on higher balances. Additional features include early direct deposit, automatic savings tools like roundups, cashback offers, cash advances, credit-building tools, and a mobile app with real-time alerts and budgeting features.

BMO Bank review

BMO Checking Account Overview:

BMO offers a range of personal checking accounts designed for everyday banking, with options suited for students, low-fee seekers, and those with higher balances. Accounts can be opened online and are supported by user-friendly digital tools and nationwide ATM access.

Account Fees:

BMO Smart Advantage Checking has no monthly maintenance fee. BMO Smart Money Checking carries a $5 monthly fee, automatically waived for customers under 25. BMO Relationship Checking includes a monthly fee that can be waived by maintaining a minimum combined balance. Overdraft protection options are available, and standard ATM or service fees may apply depending on usage.

Perks & Benefits:

New customers may qualify for a $400 cash bonus by opening an eligible account and receiving at least $4,000 in qualifying direct deposits within 90 days. Additional benefits include mobile check deposit, bill pay, early direct deposit, and access to over 40,000 fee-free ATMs. Relationship Checking customers may receive extra perks like rate discounts and service fee waivers. All accounts include FDIC insurance up to legal limits.

TD Bank Beyond Checking review

TD Beyond Checking Account Overview:

TD Bank’s Beyond Checking account is designed for customers seeking premium features, rewards, and flexibility. It offers interest-earning capabilities, fee reimbursements, and added perks for those who maintain higher balances or set up qualifying direct deposits.

Fees:

- Monthly Maintenance Fee: $25, waived with $5,000+ in direct deposits, a $2,500 minimum daily balance, or $25,000 in combined eligible TD accounts.

- ATM Fees: Free at TD and non-TD ATMs with reimbursement for fees when a $2,500 minimum daily balance is maintained.

Perks & Benefits:

- Interest Earnings: Earns interest on account balances.

- Overdraft Payback: Automatically refunds the first two overdraft fees per calendar year.

- Free Services: Includes standard checks, money orders, official bank checks, stop payments, and one outgoing wire transfer per cycle.

- TD Early Pay: Access eligible direct deposits up to two days early.

- Linked Savings Benefits: Waives monthly fees on linked TD personal savings accounts.

CIT Bank review

CIT Bank eChecking Account Overview:

CIT Bank’s eChecking account is tailored for everyday banking needs, offering an interest rate of 0.25% APY¹ on balances over $25,000 and 0.10% APY on lower balances. It is designed for those who prefer online and mobile banking.

Account Fees:

Opening a CIT Bank eChecking account is free, though a $100 minimum deposit is required. There is no ongoing minimum balance requirement and no monthly maintenance fees. Additionally, there are no fees for online transfers or incoming wire transfers. CIT Bank also reimburses up to $30 per month for non-network ATM fees, making cash access more convenient. While overdraft protection is offered, applicable fees may apply.

Perks & Benefits:

Features include mobile check deposits, unlimited withdrawals, online bill pay, and transfers via Zelle®, Bill Pay, Samsung Pay and Apple Pay.² The eChecking account combines interest-earning potential, minimal fees, and digital banking tools.

Upgrade Checking Account review

Account Overview:

Upgrade’s standard Rewards Checking account is a no-fee online checking option that offers 1% cash back on everyday purchases. This rate applies to expenses such as gas, groceries, dining, and recurring payments like utilities and subscriptions. All other purchases earn 0.5% cash back. Unlike the Rewards Checking Plus account, this option does not require a qualifying direct deposit to access these rewards, making it a flexible choice for those who want consistent cash back benefits without additional requirements.

Fees:

No monthly fees, no minimum balance requirements, and no overdraft fees. Additionally, Upgrade charges no ATM fees for in-network transactions, but third-party ATM fees are not reimbursed under this account option.

Perks & Benefits:

Customers can enjoy early direct deposit, receiving their paycheck up to two days early. The account provides access to over 55,000 fee-free Allpoint® ATMs nationwide. Additional features include mobile check deposits, automated savings tools, and secure digital banking. All funds are FDIC insured up to $250,000 through Cross River Bank.

UFB Freedom Checking + Savings review

Account Overview:

Opening a Freedom Checking account with a Portfolio Savings account offers up to 3.60% APY.** Combining these accounts can increase your savings APY by up to 0.20%.** Additionally, the Freedom Checking account provides 2.00% APY.* (Checking rates 25x the national average.†) UFB Direct also features fewer fees and faster transaction processing.

Fees:

UFB Direct offers no monthly maintenance fees and requires no minimum deposit to open an account, making it an easy and cost-effective banking option for new customers.

Perks & Benefits:

Customers enjoy fee-free online and mobile banking services, such as mobile deposits, transfers, and bill pay. Move money instantly between your Portfolio Savings and Freedom Checking accounts. Account is FDIC insured up to the maximum allowance limit. Access to over 90,000 fee-free ATMs.

Cash Management Accounts

An Online Banking and Cash Management Alternative

The traditional way of thinking about banking is to have separate checking, savings, and investment accounts -- your bank handles the first two, and your brokerage firm would deal with the third. But some financial institutions are offering a new product that combines some features of all three: the cash management account. While it's technically a brokerage account, it's designed to enable consumers to handle their cash and make payments, all while earning interest. Offering a consolidated view from which to manage all your cash movements, these FDIC-insured accounts usually include a debit card, checkbook, and online bay pill services, just like a regular checking account. As an added bonus, though, you can also buy and sell shares. By eliminating the need to transfer funds between accounts, cash management accounts not only save time but also give users a clear, one-stop view of their money. Indeed, many consumers use them to bundle multiple investment accounts, thereby streamlining their finances and facilitating the implementation of financial strategies. While these accounts do pay interest, these are oftentimes a bit lower than those you can get with an online bank, though still higher than with a brick-and-mortar institution.

Many of the biggest players in Fintech have begun offering cash management accounts, such as SoFi Money, PNC, Chime, and Betterment. All four offer very reasonable minimum deposits of less than $25, and only PNC has a minimum account balance ($500).

What should I look for in a cash management account?

There are some basics you should make sure are included in your account:

- free debit card

- ATM access

- unlimited check writing

- easy access, either online or via app

Some firms go above and beyond the basics mentioned above to offer add-ons such as ATM rebates (mostly limited to specific networks in the US, though some do offer these worldwide), mobile deposits, account activity alerts, and links to external banks. This last feature is particularly useful since it means you can do even more to manage your money efficiently -- by depositing excess cash in an account with a higher APY, for instance.

What to keep in mind-

While cash management accounts have monthly fees, many have very low ones or eliminate them altogether, so make sure to read the fine print carefully. Since all these accounts are different, there may also be a minimum balance or deposit, or other requirements that can vary between providers. Additionally, keeping money in these accounts may mean limiting your higher-yield investments.

Our Research

More insight into our methodology

Account Features

Banks have a wide variety of checking accounts available that can help you manage your money; the trick is finding the one that truly meets your financial needs while charging the lowest fees. These fees and features can vary widely so it's important to know what each account can give you (and charge you) before committing to one.

First, it's useful to know the types of checking accounts that are available, which include basic, free, interest-bearing, joint, and accounts for seniors or students. Basic checking accounts allow consumers to pay bills and own a debit card for transactions. Customers have a limited number of checks per cycle, and usually need a qualifying direct deposit transaction or consistent minimum balance in order to avoid maintenance fees. This type of account seldom earns interest. An interest-bearing checking account, on the other hand, typically pays interest once a month, but does assess a monthly maintenance fee and has a minimum balance requirement as well.

Free checking accounts are the most popular option available, and for good reason. Customers who select a free checking account will have no monthly maintenance fee and won't have to worry about keeping a particular minimum balance. Another option is a joint account, with two or more people who share expenses. These can be basic, free, or interest-bearing; it depends on the bank. This type of account is used mostly by couples and families. Finally, senior and student accounts are designed for people who meet the age requirement established by the institution (student accounts are typically for college-age customers). The perks vary by bank and can include free checks, discounts, and better rates on other products offered by the financial institution.

Fees & Restrictions

One of the most important aspects of choosing a checking account is knowing exactly the kind of fees that will be assessed and why.

The most commonly incurred fee is the maintenance fee. Unless they provide a free checking account, most banks will charge an either monthly or yearly maintenance fee. In most cases, this fee is charged if the account holder does not maintain a particular minimum balance in the account and/or does not sign up for direct deposit with the bank. Many online banks and credit unions are now offering accounts that do not charge this fee, however, even when the bank account has a very low balance.

There are other fees that apply even to free checking accounts however. One of them, the overdraft fee, is one that can affect your account in significant ways. First, it's essential to know your bank's policy on overdraft fees as some banks charge exorbitant fees for each overdraft - even if posted in the same day - which can lead many customers to face steep deficits in their accounts that are harder to recover from. If overdrafts are a worry, it's important to look for banks with a lower overdraft fee and a low maximum number of transactions per day that will incur a fee.

There are, of course, a number of other transactions that can also be charged by a bank, such as wire transfers, replacement cards, and obtaining additional checks, among others. It's important to assess your banking habits and see what is truly a deal-breaker when it comes to fees.

Support, Reputation, & Financials

One surefire way to understand how a financial institution works is by reading customer reviews. Potential customers can learn about bank practices and perks, as well as how current customers feel about the attention and care they receive at their bank. Agencies such as the Better Business Bureau (BBB) give customers an outlet to comment about a business, whether or not they are accredited by the organization. The BBB comments include positive, neutral, and negative reviews, and any complaints a company receives. The agency also reports on how quickly customer complaints on their website are handled and resolved.

With all the tools available today, it's easier than ever for customers looking to research financial institutions before committing to one. Customers can learn about a company's stability from federal and state regulators, as well as rating agencies, all of which offer in-depth looks at financial institutions. One of these regulating agencies, the Consumer Financial Protection Bureau (CFPB) establishes and enforces rules that protect consumers against predatory practices. On the agency’s website, consumers can access tools to help them manage their finances and can submit complaints and see first hand how companies respond.

Helpful information about Checking Accounts

These days, it might be more accurate to think of checking accounts as "spending" accounts. Gone are the days where it was necessary to write checks to pay for services, or where you had to wait in line at a bank to withdraw funds. Although you can still do this of course, debit cards, ATMs, and online banking have made paying with your checking account simpler than ever before. In fact, digital baking has become an essential part of everyday life.

Traditional checking accounts come with various fees, and most don’t gain interest like savings accounts do. Brick-and-mortar banks try to spice things up by offering a variety of perks for their checking accounts, but with the rates they offer, these are hardly enough. However, there is a cheaper alternative to traditional checking that offers better benefits.

Living in a digital age, it’s no surprise that people have embraced online banks. They offer the same benefits traditional banks do, but with some of the most competitive rates available. Online banks can do this because they don’t pay to maintain a physical presence, minimizing their operating costs. For checking accounts, they offer fewer and cheaper fees, along with additional features like increased interest rates, free online bill pay, and 24 hour access. Interest rates earned by online checking accounts are not as high as their online savings counterparts. However, some online banks do offer high promotional APYs, and because most online banks are insured by the Federal Deposit Insurance Corporation (FDIC), you can rest assured that all your funds are safe.

Now, there are some slight drawbacks to online banks. For one, not having a physical location means that all queries will need to be addressed online or by phone. Another drawback is that some online banks don’t offer direct ATM access, which means that customers rely on ATMs from other banks to withdraw funds, which may mean additional fees. However, online banks are aware of these inconveniences, and most take adequate measures to solve them, like having various means of communication (phone, email, live chat) and refunds in the case of ATM fees.

If you feel that online banking is right for you, your first step is to compare all of your available options. First, look for banks that offer high APY rates, but make sure you read their terms and conditions to know if these are promotional rates or if they depend on specific conditions. For example, some banks offer a high APY for a specific amount of time, but drop them afterwards. Others offer high APYs if your account balance is high, but discontinue it if you go below a specific number.

Next, compare the number of standard fees that come with the checking account, their costs, and if they waive options. Some online banks waive maintenance fees if you keep a certain balance, while others waive them if you deposit a specific amount per month. Also, check if there is a minimum balance requirement, if there are any added fees or penalties, and if they limit the amount of cash you can spend or withdraw daily. Keep an eye out for any additional features companies offer, such as free physical checks and debit cards, points or rewards systems, free online banking, and whether or not they have a mobile app.

If you withdraw money often, you should look for online banks that give you easy access to ATMs, or that can reimburse ATM fees. Some online banks are an extension of traditional banks, meaning that their ATMs and banks allow free in-person withdrawals. Other online banks partner with regular banks so that customers have access to their ATMs without fees. Some offer refunds for any fee customers have to pay, while others refund up to a certain amount per month. Always look for banks that have these features, since they guarantee a headache-free experience when withdrawing from your checking account.

FAQs about Checking Accounts

Can I have more than one checking account with my bank?

In almost every single case, you can have as many accounts of as many different types as you want with a single bank. Very few banks limit the number of accounts you can hold with them, and if they do, the limits are very high, usually over 20. Additionally, you can open accounts with more than one bank.

Can I open checking and savings accounts with different banks?

Nothing keeps you from opening accounts with different banks. In fact, you may find, for example, that the savings accounts offered by Bank X are more favorable than Bank Y’s, while Bank Y’s checking accounts charge less fees than Bank X’s. In this case, having a savings account with one bank a checking account with another would be a smart move. One thing to keep in mind, however, is that many banks offer benefits for keeping all your accounts with them. It’s common to see banks that don’t charge a fee when transferring money from one account to another if they are both in the same bank. You may also find it convenient to hold a single debit card for both your checking and savings accounts.

What is a checking line of credit?

A checking line of credit (previously called overdraft line of credit) is a loan attached to your checking account. If you run out of money and you’ve been approved by your bank, the line of credit protects from overdrafts and from having transactions denied for non-sufficient funds. Plus, it’s a convenient line of credit when you need quick access to cash. Any money you use is provided as a standard loan from your bank, so you’ll pay interest on the amount you borrow. However, checking lines of credit are often less expensive than traditional overdraft protection programs, which usually charge around $35 for each rejected transaction. Depending on the bank it can also include flexible repayment options and a low-interest rate.

Can I be turned down for a checking account?

A bank or credit union can deny your application for a checking account when a checking account reporting company such as ChexSystems or Early Warning has negative information in its files about your checking history. These agencies share their reports with banks and credit unions, which use the information in deciding whether to approve accounts. According to the Consumer Financial Protection Bureau, there are several reasons why you to be denied a checking account: (1) having an unpaid negative balance on a previous checking account, such as from an overdraft from an account closed by the bank or credit union that you did not repay, (2) if you were suspected of fraud related to a checking account, or (3) if you have shared a joint account with someone who had these types of problems.

What is a high-yield checking account and do I need one?

With a high-yield checking account or interest-bearing checking account, the bank pays your interest on the money in your account, much like it pays interest on a savings account. Banks that offer a high APY (2,3, or even 4 percent) tend to be regional banks or local credit unions. They are looking to draw people in with the possibility of high rates, but don’t want those customers treating these accounts like savings, where the money just sits there and does nothing but earn interest. Banks basically want you to treat your high-yield checking account like a regular checking account, in which you deposit money, pay bills, and use your debit card.

However, high-yield checking accounts come with a lot more strings attached than a regular checking account. Many have a minimum number of debit card transactions allowed per month, usually 10. While others require electronic receipt of checking statements and a direct deposit set up to go into the account. Also, make sure the bank has a reasonable balance cap and that it refunds your ATM fees. So, if this is not a problem for you, consider giving a high-yield checking account a try.

What should I do with my check after I deposit it online?

With the convenience of mobile banking services, it’s pretty easy to deposit checks by just taking a couple of photos with your phone. Once you have deposited the check successfully—which means that you see the money in your account and can also access an image of the scanned check online—you should write “Mobile deposit on Date” on the front of your check. The date should be the month, day, and year of the deposit. Then securely store your check for 5 days. This allows sufficient time in case the original check is required for any reason. Then, you can destroy the check or mark it “VOID.”

Do I need paper checks anymore?

Paper checks can seem out of date but you might need to write one occasionally. Your landlord may insist that you pay him with a check, and some small businesses don’t accept credit or debit cards. Also, paper checks help you stay disciplined with your spending, avoid convenience fees for electronic payments, and also have old-school security, so your money is safe. On the downside, checks cost money and processing takes longer. Overall, checks can be convenient, so if your checking account offers free checks, you might as well order a pack.

How do I avoid monthly service charges?

Fees and rules vary by institution, but you might be able to avoid monthly service charges by meeting one of the following requirements. (1) Maintain a minimum balance. Keep enough money in the account or pay the service fee for each month-long statement cycle when you don’t meet the minimum balance requirements. (2) Enroll in direct deposit, whereby your paycheck, pension, Social Security benefits, or other regular monthly income is automatically deposited into your checking account. Bear in mind that each bank might have different qualifying criteria. (3) Link your accounts. Most banks will waive the monthly service fees for customers who use a debit card linked to the account a certain number of times each month, usually around ten transactions.

Do online checking accounts have ATMs?

These days, many online banks offer ATM access with their checking accounts. In many cases, online banks partner with traditional banks and offer access to the other bank’s ATM free of charge. When there is not a partnership in place, many online banks will offer to reimburse any fees charged by the ATM’s bank (up to a certain amount every month or for a specific number of instances). Finally, some online banks will provide a checking debit card to their customers but charge hefty fees when customers use it to withdraw money from an ATM. In any case, if having access to ATMs is important to you, make sure you read the terms of your checking account closely to see what your bank’s policy is.

Are online checking accounts secure?

Online banks are secure in several ways. First, your data is secure if the bank's website is protected by SSL encryption. One way to check this is to see if the URL in the address bar is preceded by "HTTPS" instead of "HTTP". The "S" indicates that the site is secured by an SSL certificate. You can read more about web encryption here.

Secondly, your money is safe because all major online banks are insured by the Federal Deposit Insurance Corporation (FDIC). This agency was founded during the Great Depression when many banks failed and customers lost the money they had deposited.

Nowadays, if an FDIC-insured bank fails, the agency guarantees that the money in your accounts will be safe. One thing to keep in mind is that only the first $250,000 in any given account is secure. If your balance exceeds this limit, it may be a good idea to check with a financial advisor to find out how you can keep your money secure.

Secondly, your money is safe because all major online banks are insured by the Federal Deposit Insurance Corporation (FDIC). This agency was founded during the Great Depression when many banks failed and customers lost the money they had deposited.

Nowadays, if an FDIC-insured bank fails, the agency guarantees that the money in your accounts will be safe. One thing to keep in mind is that only the first $250,000 in any given account is secure. If your balance exceeds this limit, it may be a good idea to check with a financial advisor to find out how you can keep your money secure.

What information do I need when applying for an online checking account?

Most online banks have a simple application that you’ll need to complete to open an online checking account. You will likely need to provide personal and contact information such as your full name, date of birth, and mother’s maiden name. The bank will also ask you to provide your Social Security number or another identification number like an Individual Taxpayer Identification Number, a state-issued ID or a valid driver’s license, or a passport or other government-issued ID. In addition, some banks might ask you to provide your debit card information, or routing and account numbers for another account that you own. You’ll need this information to make the initial deposit to your new account. Finally, you will need to provide your email address and phone number.

Why should I open an online checking account?

Opening an online bank account is easy. It takes just minutes, and you can do it from the comfort of your own home. With an online checking account, you can check balances, pay bills, deposit checks, transfer funds, and even send money—with your tablet or smartphone. Also, it’s an easy way to keep track of your spending habits. Other advantages include 24-hour access to your account, lower rates, lower fees, and some banks offer an extensive set of online tools such as tax forms, budgeting tools, investment analysis tools, loan calculators, among others. Additionally, some banks offer interest-bearing online checking accounts, which pays you interest for the money in your account.