Best Medicare Supplement Insurance

Based on In-Depth Reviews

-

120+Hours of research

-

25+Sources used

-

15Companies vetted

-

4Features reviewed

-

5Top

Picks

- Medicare Supplement Insurance helps you manage out-of-pocket costs for covered services

- Also called Medigap because it covers “gaps” in costs after Medicare Parts A and B pay their share

- Medigap Plans C and F, which cover the Medicare Part B deductible, are being discontinued in 2020

- Sign up for Medigap during Open Enrollment to lock in the best premium for your plan

How we analyzed the best Medicare Supplement Insurance

Our Top Picks: Medicare Supplement Insurance Reviews

United Medicare Advisors review

Best Medicare Supplemental Dental and Vision Insurance

Screenshot unitedmedicareadvisors.com, July 2, 2019.

UnitedHealthcare is a prominent multi-line health insurer offering comprehensive dental and vision plans. Its dental coverage, provided by Golden Rule Insurance Company, offers zero-deductible coverage for preventive care and a variety of plans tailored to different ages and needs, such as specific plans for older individuals covering dentures and for children covering orthodontics. The company's dental plans are competitively priced and can be bundled with vision coverage for additional savings. The plans cover a broad range of procedures, from preventive care like routine examinations and cleanings to major services like implants and dentures.

United Healthcare's vision insurance is also provided by Golden Rule Insurance Company and covers ongoing expenses such as routine eye exams, prescription glasses, and contact lenses. You can buy standalone vision insurance or bundle it with dental. Both vision and dental insurance are available for all ages, so you can get coverage for your family, as well.

A.M. Best has rated UnitedHealthcare’s financial strength “A+ (Superior)”, which indicates the overall stability of the company's finances and strong ability to pay out claims.

Humana review

Humana Company Overview:

Humana is a leading health and well-being company that has been serving Medicare beneficiaries for decades. The company offers a wide range of health insurance options, including Medicare Advantage, Medicare Supplement, and prescription drug plans, designed to provide affordable and reliable coverage.

- Plan Options

- Plans A, B, C, F*, G, K, L, and N, with high-deductible options for F and G in some states.

- Immediate Coverage

- No waiting period for preexisting conditions when enrolled during guaranteed issue.

- Eligibility

- Open to most Medicare beneficiaries with Parts A & B; some states also offer coverage for those under 65 with disability or ESRD.

- Nationwide Access

- Use any doctor or hospital in the U.S. that accepts Medicare patients.

- Transferable Plan

- Keep your plan if you move to another state within the U.S.

- Household Discount

- Potential savings when a spouse or household member is also enrolled; additional discounts may apply for electronic payments.

USAA review

Best for Low Medicare Insurance Premiums

Screenshot Usaa.com June, 2023

USAA is a financial services company founded in 1922 by members of the U.S. Army. Originally intended to insure personal vehicles, it’s now grown to offer all kinds of insurance and banking products. However, it still maintains its commitment to servicemembers: its products are only available for former and current members of the military and their family members.

USAA offers Medicare Supplement Insurance policies to people who are not eligible for TRICARE for Life, the Armed Forces’ health program for Medicare beneficiaries. To view the plans offered, you have to log in as a USAA member. All you need for this free membership is the military sponsor’s name, date of birth, USAA membership number, and Social Security number. The sponsor can be you, your current spouse, your parents, or your parents-in-law.

Once you complete the membership, you’ll be able to see the plans available to you and apply for Medicare Supplement Insurance. Though your premium may vary depending on several factors, the average USAA premium for Plan G starts at $100, making it lower than the national average. Their Medigap Plan N is the most affordable option, with copays as low as $20 for a doctor visit and $50 for an emergency department visit.

USAA Life Insurance Company has excellent financial strength ratings: AA+ from A.M. Best and Standard & Poor’s, with a Stable outlook according to both. It also enjoys a very low complaint ratio according to NAIC, with zero complaints for Medicare Supplement in 2022.

If you are eligible for USAA membership, we strongly urge you to check out the health insurance coverage plans and rates offered by the company. The only reason they’re not higher on our list is that the strict membership requirement limits the number of consumers who can enroll. As for everything else, they get our stamp of approval.

See our USAA Medicare supplement insurance review for more.

AARP review

Most Supplemental Medicare Insurance Plans

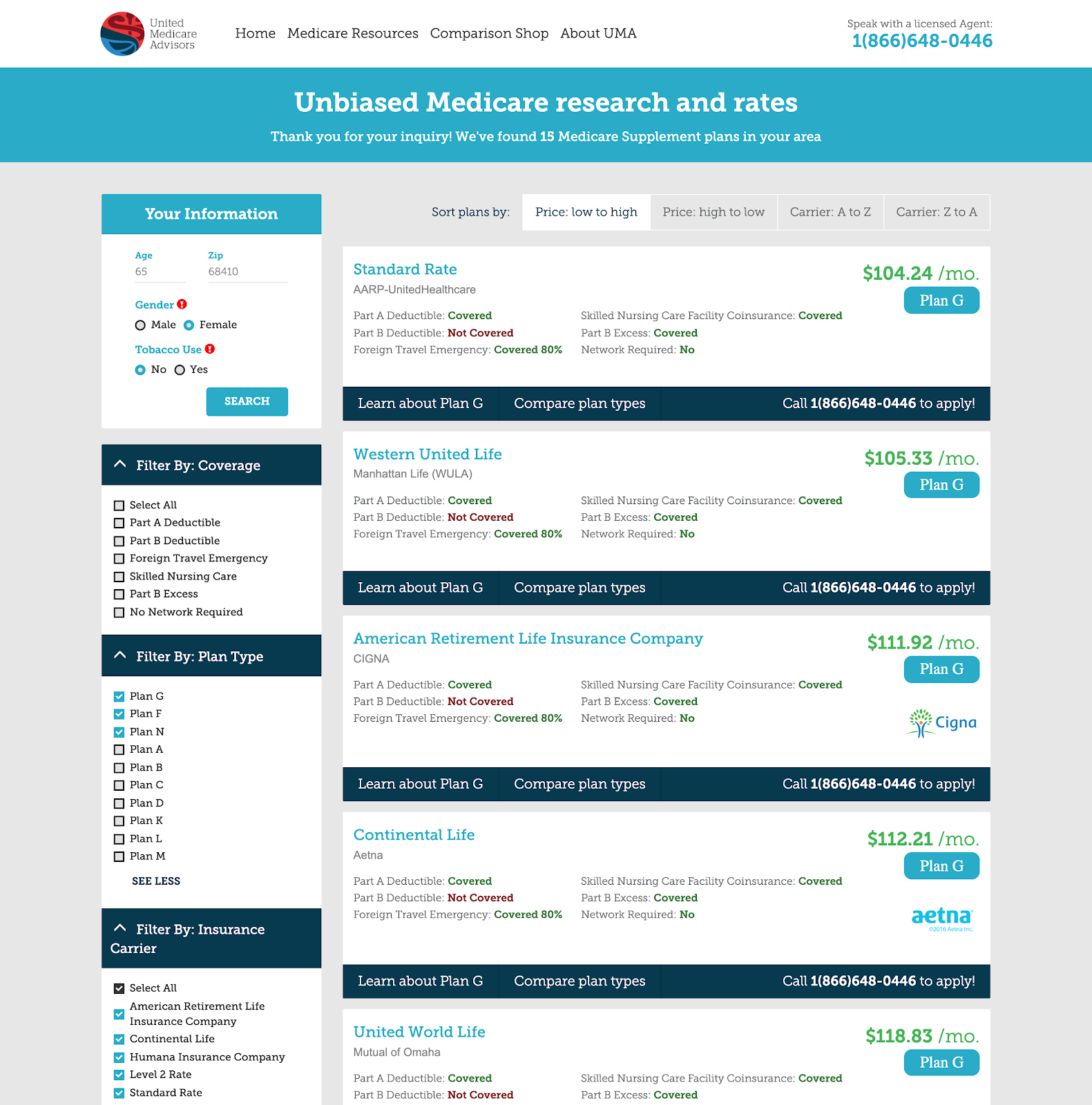

(The image above shows price quotes for a non-smoking woman in Nebraska [ZIP code 68410].)

Screenshot https://www.aarpmedicareplans.com July 2, 2019.

AARP is one of the most well-known brands in the United States. Since 1997, it has lent its name to a catalog of Medicare Supplement policies issued by UnitedHealthcare. Medigap through AARP Medicare Plans is only available to AARP members.

Currently, AARP Medicare Plans (AARPMP) offers eight Medicare Supplement options: Plans A, B, C, F, G, K, L, and N, though the offerings could change by state or zip code. We requested a quote for an almost-65-year-old woman in Nebraska to see what you would see when requesting a quote. We were impressed, first, by the well-organized and comprehensive display of all the plans available.

Users can view a summary of what each plan covers. By clicking on “Plan Details” they can see even more information about what that Medigap plan pays for and what the beneficiary is responsible for. Back on the online quotes page, users can compare up to four plans to see the differences in coverage and plan pricing. You can compare Medigap Plan G high-deductible plans with other plans that offer more comprehensive coverage as well as the cost-per-benefit period.

Another thing we like about AARPMP’s site is its resource database. There are dozens of pages with valuable information about Medicare and Medicare Supplement Insurance policies, Medicare enrollment periods, and other topics in a clear and user-friendly way.

Customers can apply for their insurance directly on the website. The form asks for information about your AARP membership and allows you to enroll if you are not yet a member (AARP membership only costs $16/year and comes with many member benefits and discounts). It also asks for general contact information, and details pertinent to your eligibility. The application is easy to read and navigate. A code lets you save your application and come back to it later.

Now, it should be made clear that AARP is not an insurance company and they do not underwrite the policies sold under the AARP Medicare Plans brand. The underwriter for these policies is UnitedHealthcare, which we cover in more detail in the next section.

Overall, we liked the wide range of Medigap plans offered by AARP Medicare Plans and the simplicity of their website. We were impressed by their resources section, which is very comprehensive and covers many Medicare-related topics. Finally, having the backing of a company like UnitedHealthcare should inspire confidence in the brand. If it makes sense for you from a financial standpoint, AARP Medicare Plans is a good place to look for Medigap Insurance.

See our full AARP Medicare supplement insurance review for more information.

Anthem review

Anthem Company Overview:

Anthem is a leading health benefits provider with decades of experience supporting Medicare beneficiaries. Backed by strong financial ratings, Anthem serves millions of members nationwide and offers Medicare Supplement plans that provide reliable access to doctors and hospitals that accept Medicare. The company emphasizes member support, wellness resources, and additional programs that enhance value beyond core coverage.

- Plan Options

- Plans A, G, and N available (Plan F only if Medicare-eligible before 2020). Some states offer “Select” or “Innovative” options with extra benefits.

- Enrollment Timing

- Enroll during your Medigap Open Enrollment Period (when 65+ and Part B active) to avoid health questions or denial.

- Eligibility

- Must have Medicare Parts A & B. Some states allow those under 65 with a disability. Plan F restricted to pre-2020 Medicare eligibility.

- Nationwide Access

- Use any U.S. doctor or hospital that accepts Medicare.

- Transferable Plan

- Plans remain valid if you move states, though pricing and availability may vary.

- Household Discount

- Discounts available when multiple household members enroll. Added perks include SilverSneakers®, prescription savings, and wellness discounts.

Mutual of Omaha review

Mutual of Omaha Company Overview:

Mutual of Omaha is an insurance provider headquartered in Omaha, Nebraska. It was founded in 1909 and offers a range of products, including life insurance, long-term care insurance, dental insurance, and Medicare Supplement insurance.

- Medigap Plan Options

- Popular choices like Plan G, Plan N, and more.

- Immediate Coverage

- No waiting periods for pre-existing conditions when you enroll during guaranteed issue periods.

- Nationwide Access

- See any doctor or hospital accepting Medicare.

- No Referrals Needed

- Visit any specialist who accepts Medicare. No approval or referral required.

- Household Discount

- Potential savings when family members enroll together.

- Easy Enrollment Process

- Apply online or on the phone.

- Trusted Experience

- With over 100 years of experience in the field, Mutual of Omaha and its affiliates brings considerable financial strength.

MedicareSupplement.com review

About MedicareSupplement.com:

Looking for the right Medicare Supplement (Medigap) plan can feel overwhelming—but MedicareSupplement.com is here to make it easier. This trusted online platform, run by TZ Insurance Solutions LLC (a licensed insurance agency), helps you compare Medigap plans side by side and connect with licensed agents who can guide you every step of the way. While the site offers a broad selection of plans, it’s a smart idea to explore additional sources too, so you can be confident you're seeing all your options.

- Compare Plans Easily

- Compare plans from multiple insurers in your state.

- Wide Plan Selection

- Access popular plans like G, N, and more.

- No Obligation Quotes

- Get free quotes without commitment.

- Transparent Costs

- See premiums and benefits upfront.

- Licensed Agents

- Speak with experts for guidance on your options.

- Simple Process

- Apply online or by phone in minutes.

Extra Help & Resources:

MedicareSupplement.com isn’t just for plan comparisons—you’ll also find helpful articles, guides, and a free Medicare guide to give you extra clarity as you explore your options. It’s a great place to start learning and take the next step with confidence.

More insight into our methodology

Level of Coverage

Medicare Supplement Insurance plans are tightly regulated by the Centers for Medicare and Medicaid Services (CMS), a government agency. CMS determines what each letter plan will cover, and it requires each insurance company to offer the plan as is, without modifications. Since all Medigap plans are the same across insurance companies, deciding between all your options will come down to, among other things, what each insurance company can offer you that others can’t.

Perhaps you’ve decided that Plan N is the best alternative for you after doing all the research (and reading this guide!). That means that any company that doesn’t offer Plan N is out of the running. For this reason, we’ve listed all the plans offered by the companies in their respective reviews.

Some insurance companies offer SELECT Medicare plans which modify standard letter plans by limiting services to a network, for example, as well as high-deductible plans, which cost less than traditional letter plans in exchange for an increased deductible. They also offer additional coverages, such as dental care, which isn’t covered by Medicare. We’ve made a note of these plans so you know whether they are more suitable for you in place of the usual letter plans.

Services

Almost as important as the coverage offered by each company are the services they provide. We looked into the extra perks insurance companies offer their Medicare Supplement insurance customers, such as wellness clinics, free preventive services, and fitness programs, as well as any discounts that could lower your premiums.

We also researched how every company “rates” or assigns prices to their Medicare Supplement insurance policies. Are they attained-age, issue-age, or community rated? The answer determines whether you’ll be charged more as you age. For example, an attained-age-rated policy will increase your premium every year based on the age you’ve reached (or attained). An issue-age-rated policy, on the other hand, bases your policy cost on your age when the policy was issued. If your premium increases, it’s because of inflation or operational costs, not because of how old you are. You should know how a company rates their policies so you can plan accordingly.

Another factor that could affect your premium is whether the company does medical underwriting. Going through a medical examination before signing up for a policy could result in a higher (or lower!) cost. There may also be a waiting period for people with pre-existing conditions, which could prevent you from getting necessary medical services for as long as six months.

Reputation & Customer Experience

Reputation is key when it comes to deciding which company to go with. After all, no one wants to deal with a company with a consistent history of denying claims, delaying payments, or simply providing bad customer service.

The National Association of Insurance Commissioners has a helpful Consumer Insurance Search that allows the public to view the number of complaints filed against an insurance company, the reason for those complaints, and how they compare with the national complaint index. This is an objective measure of how well the insurer does with consumers. We have provided this data for every insurance company on our list.

We have also sifted through customer reviews online for common complaints in order to give you a preview of what to expect or watch out for when dealing with a particular company. When reading this data, however, we kept in mind that customers leave more negative than positive reviews, and that larger companies will always have more complaints than smaller companies. This information alone shouldn’t be used to make a decision but can be important when viewed as part of the larger picture.

As for customer service, we considered how easy it is for a customer to get in touch with a company—having extended hours of operation, web chats, and an online system to report any problems is key to keeping the lines of communication open with consumers. Being able to file claims or check on claims status online is also a bonus.

Financial Strength

Financial strength is a company’s ability to meet its financial obligations. In the case of insurance companies, it means how likely they are to, now and in the near future, pay claims from policyholders, providers, beneficiaries, and third parties. Nevertheless, enrolling with a company that has low financial strength ratings—as determined by a credit rating company such as A.M. Best or Standard & Poor’s—doesn’t mean you’ll be left in the lurch if they go under. Most insolvent insurance companies are bought out by companies in better standing which take over the defunct company’s policies. There are also state Insurance Guaranty Associations, legally tasked with continuing coverage for affected policyholders.

Though it’s not a common occurrence, an insurance company’s bankruptcy is definitely not ideal, and it will probably cause you a lot of needless headaches. The best thing to do, then, is to find a company that has a stable financial outlook and that won’t let you down when you need them the most.

Helpful information about Medicare Supplement Insurance

What is Medicare?

In the simplest terms, Medicare is a health insurance plan subsidized by the federal government. It was originally created to help Social Security beneficiaries receive healthcare services, but it’s now been expanded to cover everyone who is:

-

Age 65 or older

-

Under 65 and has a disability

-

A patient of end-stage renal disease (needs continuing dialysis or a transplant)

Together, Medicare Part A and Part B are usually called Original Medicare. With Part A and Part B, you can receive services from any provider (doctor, hospital, or other facility) that accepts Medicare. Unlike private insurance companies, you don’t have to restrict yourself to a network.

Part C was introduced in 1997 and it’s more commonly called “Medicare Advantage”. It lets beneficiaries get Medicare benefits through private insurance.

Part D is the optional drug coverage that was introduced in 2003. Part D is offered through private insurers, and beneficiaries aren’t automatically enrolled.

Part A

Part A covers inpatient hospital services, as well as care in a hospice or skilled nursing facility and some home health care expenses. Most people don’t have to pay a premium for Part A (premium-free Part A), but if you’re 65 and you didn’t pay the Medicare tax for 10 years or more, you may have to pay a premium.

The Part A premium is calculated based on whether you paid the Medicare tax and for how long you did. If you didn’t pay the Medicare tax, you’ll pay $437/mo. in 2019. If you paid the Medicare tax for less than 30 quarters, you’ll pay $437. If you paid the Medicare tax for 30 to 39 quarters, you’ll pay $240.

Part B

Part B covers medical services, like the ones you would get from your doctor. It can also cover some home health services, medical equipment such as wheelchairs, outpatient services, and preventive services. All beneficiaries pay a premium for Part B. For 2019, it is $135.50/mo., but it depends on your income and it tends to increase a little every year.

In addition to the premium, Part B includes a deductible. This is the amount you have to pay out of your own pocket before the insurance kicks in and covers some of your costs. For 2019, the deductible for Medicare Part B is $185. After the deductible, you’ll pay 20% of most medical expenses.

Part C

Also known as Medicare Advantage, Part C refers to a healthcare plan offered by a private insurance company that offers the same benefits as Medicare Parts A and B. However, you still need to enroll in Part A and Part B to enroll in a Medicare Advantage plan.

Depending on the type of plan you choose, you’ll have to go to the providers in the insurance company’s network in order to avoid paying high out-of-network costs. Some Medicare Advantage plans help you pay the Part B premium. In addition, Medicare Advantage plans have a premium of their own, but it can be as low as $0 in many places and is usually considerably lower than non-Medicare insurance. Part C plans may offer prescription drug coverage, though this varies depending on the type of plan you have.

Part D

Medicare Part D helps you pay for prescription drugs. Depending on your plan, you may have to shop at preferred pharmacies to get the best price. You may also have to pay an out-of-pocket deductible before the insurance begins paying. Part D drug plans carry a premium which you must pay in addition to the Plan B premium.

You cannot be automatically enrolled in Part D. You must specifically enroll in Part D when you choose your Medicare coverage. If you don’t select Part D, your prescription drugs will not be covered by Part A or Part B.

Screenshot from "Choosing a Medigap Policy," July 8, 2019.

When and How to Enroll in Medicare

As we mentioned above, people who want to enroll in Medicare must be at least 65 years old; if they are under 65, they must either have a covered disability or suffer from end-stage renal disease. Here we’ll discuss these requirements in full.

If You’re Age 65 or Older

As you near your 65th birthday, you must start thinking about Medicare.

If you receive benefits from the Social Security Administration or the Railroad Retirement Board (RRB), you will be automatically enrolled in Parts A and B.

If you don’t receive these benefits yet, you’ll have to enroll yourself. You’ll have three months before your birthday month, the month of your birthday, and three months after your birthday month to submit the paperwork. This total of seven months is called the Initial Enrollment Period.

If you’re 65 but you’re covered by your or your spouse’s employer’s group health plan, you don’t have to enroll in Medicare immediately. You can choose to enroll at any point during your coverage or you can enroll within eight months of the employment termination date.

For example, if you’re still working, you’re enrolled in your workplace group plan, and you turn 65, you can choose to enroll while you still have coverage but you’re not obligated to. Once your job ends, because you retire or you’re terminated, you have eight months to enroll in Part A and Part B from the date the employment or the coverage ends. This is called a Special Enrollment Period or SEP.

Keep in mind that if you leave your job, you may be entitled to COBRA coverage. However, this doesn’t count as employment coverage and the eight-month Special Enrollment Period runs concurrently with the period during which you have COBRA. This means that, if you wait until your COBRA ends, your Special Enrollment Period may already be over and you’ll be subject to a penalty.

If You’re Under 65 With a Disability

If you have a disability and you’re receiving disability benefits from the Social Security Administration, you’ll automatically be enrolled in Parts A and B of Medicare once you’ve been receiving benefits for 24 months.

This waiting period is waived for patients with amyotrophic lateral sclerosis (Lou Gehrig’s disease). Once disability benefits start, you are automatically enrolled in Medicare Parts A and B.

If You Have End-Stage Renal Disease

If you have end-stage renal disease (ESRD), regardless of your age, you can elect to enroll in Medicare Parts A and B. ESRD refers to permanent kidney failure that requires kidney dialysis or a kidney transplant. Medicare can help pay for these services. Typically, Medicare will begin to pay for treatment on the fourth month of your dialysis. You still have to meet other requirements, like having worked a minimum of 10 years under Social Security or being the spouse or minor dependent of someone who has.

Other Enrollment Periods

Apart from the 7-month period when you are initially eligible to enroll in Medicare Part A and Part B, you can also enroll during the General Enrollment Period, which runs from January 1 to March 31 of every year. The General Enrollment Period is available to you if you (a) didn’t enroll when you were first eligible and (b) you didn’t qualify for a Special Enrollment Period. Keep in mind that enrolling during a General Enrollment Period might mean paying a late enrollment penalty, which is explained below. When you enroll during the General Enrollment Period, your coverage doesn’t start until July 1 of that year.

Special Enrollment Periods are other times when you are able to enroll in Medicare Parts A and B without paying a penalty.

-

If you’re covered under a group health plan through your workplace or union and you turn 65, you can enroll in Medicare Part A and Part B at any time while you’re still working or covered by the plan.

-

If your employment ends or your coverage through your job ends, you have eight months to enroll in Medicare Part A and Part B.

-

If you receive social security disability benefits and you’re covered by a group health plan through your job or your spouse’s job, you can enroll in Medicare Part A and Part B at any time while you or your spouse are still working or you are covered by the plan.

-

If you’re a volunteer serving in a foreign country, you may be eligible for a special enrollment period when you return to the United States.

If you qualify for what Medicare calls “Extra Help”, which means you need help paying for the prescription drug costs that Medicare Part D doesn’t cover because of your income or other financial situations, then you may qualify for additional Special Enrollment Periods. You may also qualify for additional SEP if you qualify for both Medicare and Medicaid or you’re enrolled in a State Prescription Assistance Program (SPAP). Visit Medicare.gov for more information on these instances.

Late Enrollment Penalties

In order to encourage people to enroll in Medicare, the federal government imposes a penalty on people who enroll in Medicare after their Initial Enrollment Period has passed and if they don’t qualify for any of the Special Enrollment Periods described above.

Part A Late Enrollment Penalty

If you don’t enroll in Part A (inpatient hospital services) when you initially qualify, you may find yourself saddled with a 10% late enrollment penalty on your Part A premium. Says the Medicare website, “You'll have to pay the higher premium for twice the number of years you could have had Part A, but didn't sign up.”

That means, if you’ve been without Part A for three years, you’ll have to pay the penalty for six years. If you’ve been without Part A for five years, you’ll have to pay for 10 years. And so on.

Part B Late Enrollment Penalty

The Part B (outpatient medical services) late enrollment penalty is more severe. “Your monthly premium for Part B may go up 10% of the standard premium for each full 12-month period that you could have had Part B, but didn't sign up for it.”

The longer you wait to enroll in Part B, the higher your penalty will be. For every 12-month period you go without Part B, your penalty goes up by 10%. If you are without Part B for three 12-month periods, that’s a 30% penalty. And this penalty will be charged for as long as you have Part B. You’ll also have to wait until the next General Enrollment Period, which usually takes place in the spring.

Part D Late Enrollment Penalty

Calculating the penalty you might pay on your premium for enrolling in Part D after your initial enrollment period is more complicated.

Medicare says, “[multiply] 1% of the ‘national base beneficiary premium’ ($33.19 in 2019) times the number of full, uncovered months you didn't have Part D or creditable coverage. The monthly premium is rounded to the nearest $.10 and added to your monthly Part D premium.”

Here’s an example: If your initial enrollment period ended on January 1, 2018 and you didn’t enroll until March 1, 2019, you spent 14 full months without coverage. Calculating 1% of the national base beneficiary premium for 2019 gives us 0.33. Multiplying this by 14, the time you were without coverage gives us $4.62. This is the amount you’ll pay on top of the base premium.

Medicare Summary

We know this is a lot of information to take in, so, in short:

-

You are eligible for Medicare if you’re 65 or older, if you get disability benefits, or if you have end-stage renal disease.

-

You must enroll in Medicare Part A and Part B (and Part D if you want) when you’re first eligible (Initial Enrollment Period) or you’ll have to pay a penalty (Late Enrollment Penalty).

-

In some cases, the penalty can be waived but you need to enroll during a certain time frame (Special Enrollment Periods). Otherwise, you’ll have to pay a penalty.

-

Otherwise, you can enroll in Part A and Part B from January 1 to March 31 of every year (General Enrollment Period), but, again, you’ll be subject to that penalty.

-

To avoid paying the penalty, enroll in Medicare Part A and Part B as soon as you’re eligible or as soon as you’re able, since the penalties add up the longer you are without Medicare.

-

Part A covers inpatient/hospital services. Most people qualify for Premium-free Part A, but some don’t.

-

Part B covers outpatient/medical services. You pay a monthly premium and an annual deductible for Part B. Once you meet the deductible, you only pay 20% of most services.

-

Part A and Part B are collectively known as Original Medicare. You can see any doctor that accepts Medicare, regardless of their network.

-

Part C refers to Medicare Advantage plans, which you buy from a private insurer. These plans replace Part A and Part B, but you may have to pay a premium and meet a deductible. Most of the time you also have to see doctors in the insurance company’s network.

-

Part D covers prescription drugs. You also get this plan from a private insurance company, and you may have to pay a premium and meet an annual deductible.

-

Part A and Part B do not cover prescription drugs, so you need to enroll in Part D if you want drug coverage. If you have a Medicare Advantage plan, you might already have drug coverage.

-

If you have Medicare Part A and Part B, you’re still responsible for paying premiums, deductibles, copayments, and coinsurances. Medicare Supplement Insurance can help you pay for these costs.

What is Medicare Supplement Insurance?

Medicare Supplement Insurance, also known as Medigap insurance, was created to fill in the “gaps” in costs left behind by Medicare Part A and Part B. Medicare Part A and Part B sometimes require you to pay deductibles, copays, and coinsurances. A Medicare Supplement policy can help you cover these costs.

A Medigap policy only supplements, not replaces, your Medicare Part A and Part B. That means you must enroll in Original Medicare before you can purchase a Medigap policy.

Medigap plans are named after letters, just like Medicare parts. This gives way to some confusion.

Remember, Medicare has Part A, Part B, Part C, and Part D.

Medicare Supplement Insurance has Plan A, Plan B, Plan C, etc., up to Plan N.

Medicare Supplement plans are standardized across almost all states. This means insurance companies can’t change the plans to offer more or less benefits. Insurers can, however, decide which plans they will offer, though the government requires them to offer certain plans.

Every insurance company that offers Medicare Supplement insurance has to offer Plan A. If they offer any plan in addition to Plan A, they must also offer either Plan C or Plan F to current Medicare beneficiaries and either Plan D or Plan G to new Medicare beneficiaries.

As we mentioned earlier, Medigap plans are the same in almost every state, except Massachusetts, Minnesota, and Wisconsin. We’ll discuss the differences later.

The federal government discontinues Medigap plans periodically. That’s why you’ll see the list of plans skip a few letters. Currently, two plans are on their way out: Plan C and Plan F. The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) now forbids Medicare Supplement policies from covering the Part B deductible. Newly eligible beneficiaries won’t be able to enroll in Plan C and Plan F as of January 1, 2020.

However, current beneficiaries with either plan will be able to keep their policies. Also, current beneficiaries who are already enrolled in Original Medicare or a Medigap plan may be able to switch to a Plan C or Plan F in 2020 if they have a guaranteed issue right, which are special circumstances when you can enroll in Medicare or Medigap without any penalties. If you are enrolled in Medicare and want to switch to Plan F or Plan C, visit Medicare.gov to see if your situation applies.

There are many options for Medicare supplement insurance. In addition to the providers mentioned in our top picks, you may also want to check out other insurance companies that may fit your needs. Read our reviews for Aetna Medicare supplement insurance and Physicians Mutual Medicare supplement insurance review, or you may want to check out our reviews of online Medicare plan marketplaces such as Health Insurance Online and Medigap.com.

How Does Medicare supplemental insurance work?

Medicare Supplement Insurance helps you pay for the gaps in Medicare coverage. Once Medicare pays its share of the services you are receiving, Medigap will help you pay the rest.

If your Part B policy says it covers 80% of a doctor’s visit, Medicare will pay that. Medigap kicks in for the other 20%. Let’s suppose your Medigap Plan says that it will pay 75% of your Part B coinsurance. That means you will only pay one-quarter of the total cost of your doctor’s visit.

Here’s an example with numbers: if the doctor’s visit had a Medicare-approved cost of $100, Medicare would pay $80, your Medigap would pay $15, and you would only have to pay $5. If you didn’t have Medigap, you would be responsible for paying the entire $20 that was left over after Medicare paid its share.

Depending on the plan you select, Medicare Supplement Insurance can help you pay for the Part A and Part B deductibles. It can also help you pay for medical expenses if you have a medical emergency outside of the United States.

Standardized Medicare Supplement Plans

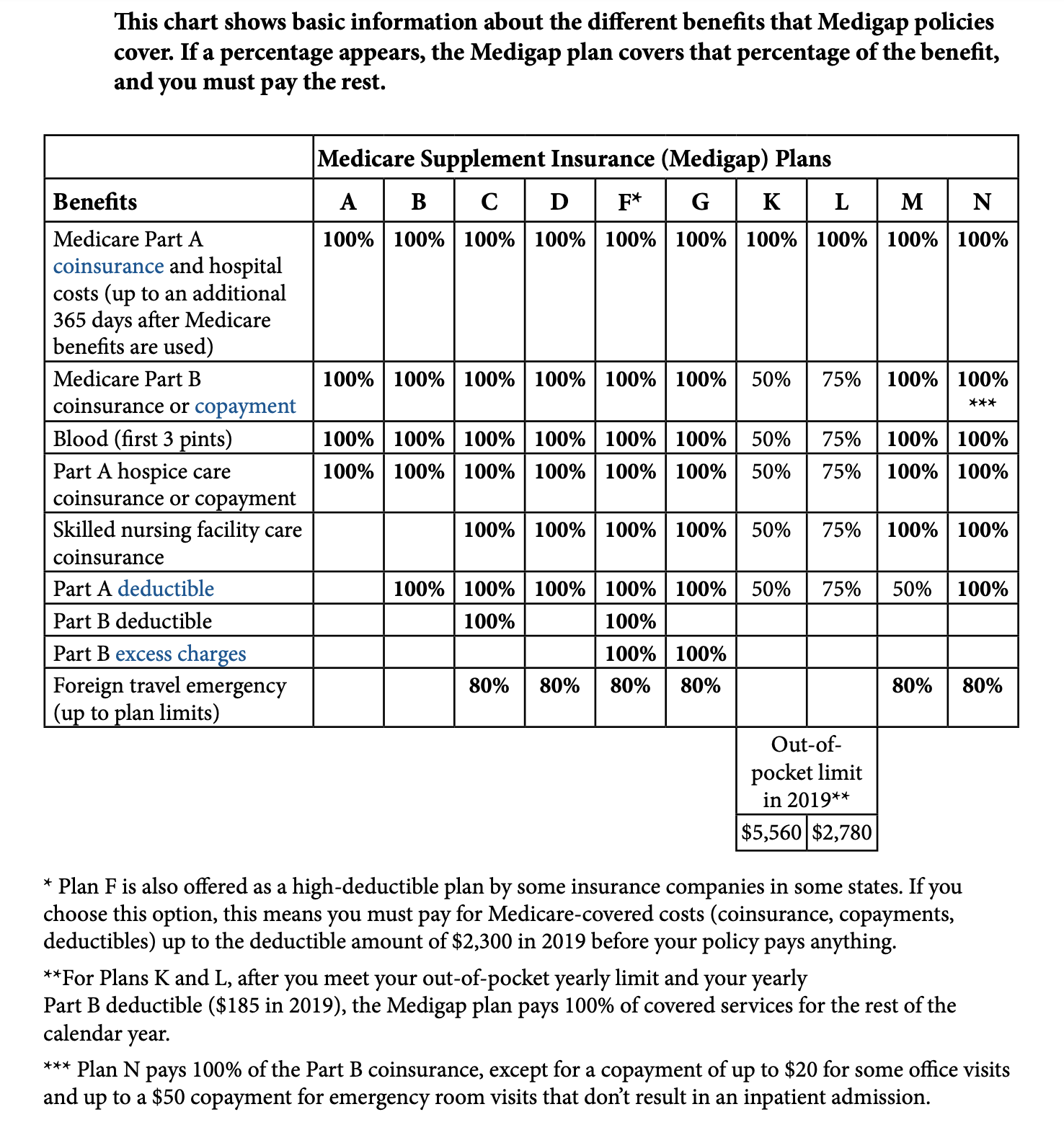

Screenshot from "Choosing a Medigap Policy," July 8, 2019.

As you can see in the table above, Medicare Supplement insurance plans can cover the following costs:

-

Part A - coinsurances and hospital costs, hospice care coinsurance or copayment, and the Part A deductible

-

Part B - coinsurances or copayments, the Part B deductible, and any Part B excess charges

-

Skilled nursing facility coinsurance

-

The first three pints of blood for transfusions

-

Emergency medical costs during foreign travel

No Medicare Supplement plan covers prescription drugs. You’ll have to enroll in Medicare Part D for drug coverage.

Plan A

Plan A is the standard Medicare Supplement plan. All other plans build upon the benefits offered by Plan A, adding other benefits or modifying the coverage amounts.

Like all Medigap plans, Plan A covers Medicare Part A coinsurances and hospital costs 100%. That means you won’t pay anything for Part A costs.

Plan A also covers 100% of coinsurances or copayments for hospice care services, 100% of Medicare Part B coinsurances or copayments for medical outpatient services, and 100% of the cost of the first three pints of blood you are administered during a procedure.

Best for: People who are looking for the lowest cost and the lowest level of coverage, especially those who don’t pay the Medicare Part A deductible and can comfortably afford the Part B deductible.

Plan B

Plan B covers everything Plan A covers. It also covers 100% of the Medicare Part A deductible.

Best for: People who are looking to pay the least for Medigap, but who have to pay the Medicare Part A deductible.

Plan C

Plan C is one of the most extensive plans. It covers 100% of Medicare Part A coinsurance and Medicare Part B coinsurance and copayments, as well as the entirety of the Medicare Part A and Part B deductibles.

Like most other plans, Plan C does not cover Part B excess charges. Excess charges are the difference between the Medicare-approved amount for a service and what the provider is legally allowed to charge. Since Medicare will only cover the amount it approves, you are responsible for covering these additional costs.

Plan C also covers 100% of skilled nursing facility care coinsurance and the first three pints of blood. It also covers 80% of medical costs incurred during travel in a foreign country, once you meet certain requirements.

Best for: People who want a high level of coverage but who don’t expect to incur in excess charges, or can afford to pay them.

Plan D

Plan D covers everything Plan C covers, except the Medicare Part B deductible. This plan will replace Plan C for new enrollees. Plans that cover the Medicare Part B deductible are being discontinued.

Best for: People who want a high level of coverage but can afford Part B excess charges.

Plan F

Plan F is the most extensive Medicare Supplement Insurance plan available. It covers everything the other plans cover, in addition to 100% of Medicare Part B excess charges.

Plan F also covers 80% of medical emergency expenses when you travel outside of the country.

Because Plan F covers the most out of all Medigap plans, it also tends to be the most expensive plan offered by insurance companies. To offset the costs of Plan F, some insurers offer a high-deductible Plan F.

With a high-deductible Plan F, you pay all costs for Part A and Part B expenses (copays, coinsurances, and deductibles) until you meet the annual deductible amount ($2,300 in 2019). Once you’ve spent that amount, the Medigap policy will pay your costs in the way described for Plan F.

Best for: People who want the most coverage possible and aren’t afraid to spend a little more in premiums or who can easily afford the annual deductible. This plan is also good for people who frequently visit doctors that charge more than the Medicare-approved amount and may have to pay excess charges.

Plan G

Plan G is identical to Plan F, except it does not cover the Part B deductible. This plan will replace Plan F for new enrollees and will include a high-deductible option for 2020, which will likely function just like the high-deductible Plan F described above. Plans that cover the Medicare Part B deductible are being discontinued.

Best for: People who want a high level of coverage and may face excess charges from their Medicare Part B services.

Plan K and Plan L

Plan K and Plan L are similar in that they both cover Medicare Part A coinsurance and hospital costs at 100%.

Both plans also cover Medicare Part B coinsurances and copays, the first three pints of blood, Part A hospice care coinsurances or copays, skilled nursing facility care coinsurances, and the Part A deductible, but not at 100% like other plans.

Plan K covers these benefits at 50% and Plan L covers them at 75%.

Neither plan covers the Part B deductible, Part B excess charges, or travel emergency medical costs.

Since Plan K and Plan L don’t cover the total amount of costs, these plans come with an out-of-pocket yearly limit to keep these costs affordable for beneficiaries. For Plan K, this limit is $5,560. For Plan L, the limit is $2,780.

While beneficiaries are paying up to the yearly limit, the plan will only pay 50% or 75% (depending on the plan). Once beneficiaries meet the out-of-pocket yearly limit and the Medicare Part B deductible, the Medigap plan will pay 100% of all covered costs for the rest of the year.

Best for: People who want a medium level of coverage and can afford to pay for costs until they reach the out-of-pocket limit.

Beneficiaries who don’t require much care and who don’t expect to need a lot of help paying for costs may want to go with Plan K, since it is generally less expensive than the alternative.

Beneficiaries who do expect to get more use out of the policy but who can’t afford a plan that covers at 100% may want to select Plan L.

Plan M

Plan M sort of acts as a middle ground between a plan with a high level of coverage and a plan with partial coverage. Plan M is nearly identical to Plan D except it only covers the Medicare Part A deductible at 50%.

Best for: People who want a high level of coverage but who can comfortably afford half of the Part A deductible. Since Part B excess charges aren’t covered, it’s also good for people who don’t expect to pay these costs often.

Plan N

Plan N is identical to Plan D (and subsequently, almost identical to Plan M), except it passes some costs over to the beneficiary. Though it covers Medicare Part B coinsurances and copays at 100%, it may require you to pay a maximum copay of $20 for select office visits and $50 for ER visits (except those that result in you being admitted to the hospital; those are covered entirely by your insurance).

This cost-sharing feature results Plan N having a lower average cost than Plan D, while also covering your Medicare Part A deductible at 100%.

Best for: People who want a lot of coverage and have to pay the Medicare Part A deductible, but want to pay lower Medigap premiums.

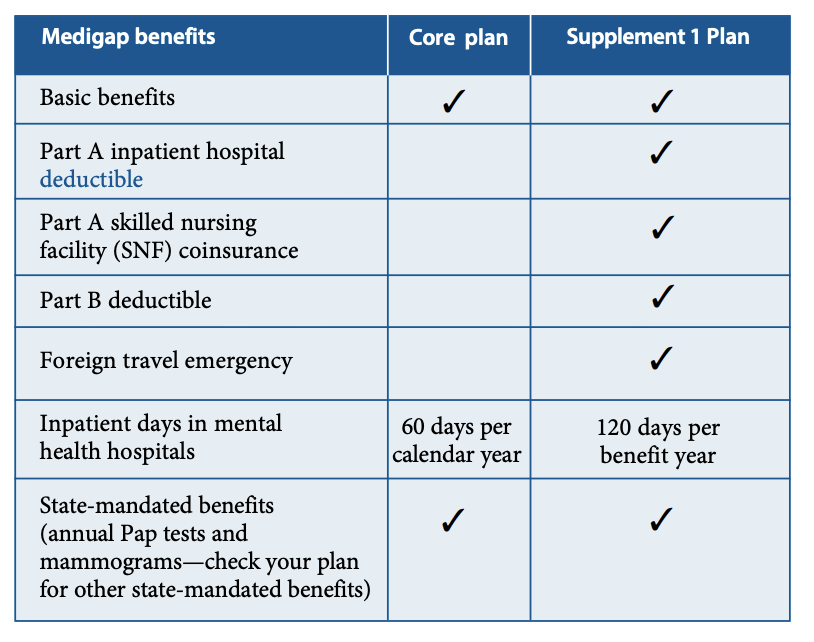

Medicare Supplement Plans (Medigap) In Massachusetts

As we mentioned above, Medicare Supplement Insurance plans are structured differently in Massachusetts. Residents of the Bay State only have two plans to choose from: the Core Plan and the Supplement 1 Plan.

Both plans cover basic benefits:

-

Coinsurance for Part A services plus 365 additional hospital days

-

Coinsurance and copayments for hospice costs under Part A

-

Coinsurance for medical services under Part B

-

First three pints of blood

Screenshot from "Choosing a Medigap Policy," July 8, 2019.

Additionally, both plans cover state-mandated insurance benefits, such as annual Pap smears and mammograms. A full list of mandated insurance benefits can be seen here. The state government establishes maximum benefit amounts for some of these benefits. You can find complete plan details for 2019, along with plan premiums, on this link.

In addition to the basic benefits and mandated benefits, the Core plan covers 60 days of hospitalization in a mental health facility. It does not cover any deductibles for Medicare Part A or Part B.

Best for: People who can afford their Part B deductible, especially those who do not have a history of mental health hospitalizations and who do not foresee a need for nursing home or inpatient care. Depending on the insurer, premiums for the Core plan can be much lower than the Supplement 1 plan.

The Supplement 1 plan covers 120 days of mental health hospitalization and the state-mandated benefits, plus the deductibles for Medicare Part A and Part B, co-insurances for services at a skilled nursing facility under Part A, and emergency medical costs when traveling outside of the U.S.

Best for: People who travel often and those who want the most coverage in case of a tragic situation that could leave them financially exposed. Some insurers, like Blue Cross Blue Shield of Massachusetts, offer SELECT Medigap plans, which restrict you to providers in their network in exchange for lower premiums.

Medicare supplement insurance in Minnesota

Medicare Supplement Insurance plans also have a different structure in Minnesota. The two standardized plans exclusive to Minnesota are the Basic plan and the Extended basic plan.

Basic benefits are included in both plans:

-

Part A coinsurance for inpatient hospital services

-

Part B coinsurance for outpatient medical services

-

First three pints of blood

-

Cost-sharing for Part A hospice and respite care

-

Cost-sharing for Part A and Part B home health services and supplies

Additionally, there are state-mandated benefits—services that the state requires insurance companies to cover, such as diabetes management equipment and supplies, vaccinations, and routine cancer screenings.

Screenshot from "Choosing a Medigap Policy," July 8, 2019.

The Basic plan further covers 100% of the Part A coinsurance for 100 hospital days in a skilled nursing facility and preventive care already covered by Medicare. It also covers 80% of medical emergency services during foreign travel, 20% of costs for outpatient mental health services, and 20% of physical therapy services.

The Basic plan does not cover deductibles for neither Part A nor Part B or what the state government calls “usual and customary fees” (a vague term for any costs you may incur that Medicare does not cover). However, policyholders are able to purchase additional riders to cover the deductibles, usual and customary fees, and preventive care that is not covered by Medicare.

Best for: People who want flexibility in creating a plan. Someone who can afford the Part B deductible but needs help covering the Part A deductible might like to choose the Basic plan and add on the rider that covers the Part A deductible. This lowers their out-of-pocket costs while avoiding paying for benefits they are fairly sure they won’t use.

The Extended Basic plan covers everything the Basic plan covers, but increases the limit of skilled nursing care to 120 days. It adds coverage for both Parts A and B deductibles, as well as 80% of the usual and customary fees, 80% of coverage in foreign countries, and 80% of emergency medical care. These last three benefits will be covered at 100% once you meet the $1,000 out-of-pocket maximum.

Best for: People who travel often or who split time between two countries, those who frequently come upon “usual and customary fees”, and those who have to pay a Part A deductible.

In addition to these two plans, there are also versions of standard Plans K, L, M, N, and high-deductible F in Minnesota, as well as SELECT plans offered by some insurers.

Visit the Minnesota Commerce Department website for more information on their Medigap plans.

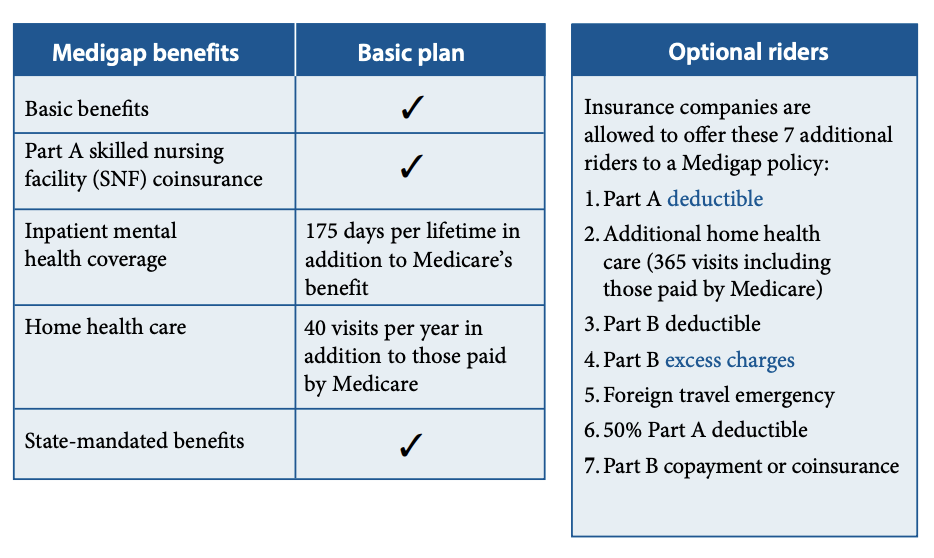

Medicare supplement insurance plans in Wisconsin

Wisconsin standardizes its Medicare Supplement Insurance very differently. For one thing, there is only one major Medigap policy available, the Basic plan.

This plan covers basic benefits:

-

Part A coinsurance for inpatient hospital services

-

Part B coinsurance for outpatient medical services

-

First three pints of blood

-

Part A coinsurance or copayment for hospice care

It also covers coinsurance for stays in skilled nursing home facilities under Part A, as well as 175 days per lifetime in inpatient mental health care, and 40 visits/year for home health care (these in addition to the days/visits Medicare itself covers).

Beneficiaries can add riders to their policy to make it fit their needs better. The riders available are:

-

100% Part A deductible

-

50% Part A deductible

-

Part B deductible

-

Part B copayment or coinsurance

-

Part B excess charges

-

Foreign travel emergency

-

Additional home health care (365 visits including those paid by Medicare)

There are also plans called “50% and 25% cost-sharing plans” in Wisconsin. Like Plan K and Plan L (see above), these plans cover only a percentage of benefits, leaving it up to you to pay the amount owed. The 50% and 25% refers to the amount you would have to pay under one of these plans. There is also a high-deductible Medigap plan in Wisconsin. Additionally, some insurers offer SELECT plans.

Screenshot from "Choosing a Medigap Policy," July 8, 2019.

More details are available on the website of the Wisconsin Department of Health Services, including premium tables for each insurance company in the state.

When Can I Enroll in a Medicare Supplement Plan?

Just like with Original Medicare, there are certain times when you are able to enroll in Medicare Supplement Plans and still enjoy the full benefits.

But first, you must enroll in Medicare Parts A and B in order to enroll in Medigap.

Open Enrollment Period

Open Enrollment is the principal time you will be able to enroll in Medicare Supplement Insurance. This open enrollment period runs for six months, starting on the month when you are first covered by Medicare Part B. If your Part B coverage began on January 1, you have from January 1 to June 30 to enroll in a Medigap plan. This Open Enrollment period will never be repeated, so don’t confuse it with the annual open enrollment period used by the Healthcare Marketplace about non-Medicare plans.

Purchasing a Medigap plan during the Open Enrollment Period means no insurer can refuse to sell you a policy, not even if you have a pre-existing medical condition. Not only do they have to sell you a Medigap policy, they can’t charge you more than they would charge a healthy person.

There are two exceptions to this rule. First, insurance companies can refuse to cover your pre-existing conditions if the condition was diagnosed or treated during the “look-back period” of six months before the Medigap coverage started. For example, if your Medigap coverage started in September and you were diagnosed with diabetes in July, it’s possible the insurance company will exclude your diabetes treatment from coverage. In this case, Medicare continues to cover their part of any eligible services but you’ll have to pay the out-of-pocket difference.

Second, the insurance company can make you wait for up to six months before they’ll cover your pre-existing conditions. During this time, you’ll have to pay the out-of-pocket costs after Original Medicare pays out. Once the waiting period is over, Medigap will begin to cover services related to your condition. You can skip all or part of this waiting period if you had “creditable coverage” before you enrolled in Medigap.

If you don’t enroll in Medigap when you’re first eligible, you can enroll at any other time, but you’ll have to go through a medical underwriting process. Insurance companies do medical underwriting to see how healthy their clients are. If you have a medical condition, they may use this information to increase your premium or even deny your application. That’s why it’s so important to enroll in Medigap during the 6-month Open Enrollment period.

Guaranteed Issue Rights

Now, there are special circumstances that would allow you to enroll in Medigap as if you were still in your Open Enrollment period. These are called guaranteed issue rights or Medigap protections. If you have guaranteed issue rights:

-

You can’t be denied a policy by an insurance company

-

All your pre-existing conditions must be covered

-

You can’t be charged more because of these conditions

That also means that, with guaranteed issue rights, your coverage can’t be put on hold because of your pre-existing conditions. Many states offer additional guaranteed issue rights, so check with your state insurance department to see a full list.

Below are some of the situations in which you have guaranteed issue rights:

-

If you have Medicare Advantage and your plan stops covering Medicare o stops offering coverage in your area, or if you move out of the plan’s service area

-

If you have Medicare Parts A and B and group health insurance through your job or union which covers what Medicare doesn’t cover, and that group coverage is ending

-

If you have Medicare Parts A and B and a Medicare SELECT plan and you’re moving out of the plan’s service area

-

If you enrolled in a Medicare Advantage plan or PACE when you became eligible for Medicare and you decide to switch to Original Medicare within the first year.

-

If you enrolled in Medigap and dropped the plan to enroll in a Medicare Advantage or Medicare SELECT plan and you decide to switch back to Medigap within the first year (this only applies the first time you switch to a Medicare Advantage plan)

-

If your Medigap insurer declares bankruptcy and you lose coverage or your coverage ends due to circumstances out of your control

-

If you drop Medicare Advantage or a Medigap policy because the company has broken the rules or lied to you

In these instances, you may be able to enroll in any Medigap plan or in a limited number of Medigap plans. Keep in mind that there is a time limit on these situations, usually around 60 calendar days, so you should begin the process to enroll in Medigap before your coverage ends or as soon as you’re aware of any arising circumstances. Medicare has more details on the remedies that could be available to you.

How to get Medicare supplement insurance

Medicare Supplement insurance, also known as Medigap, can help pay for the costs that Original Medicare (Parts A and B) doesn't cover, such as copayments, coinsurance and deductibles. Here are the general steps to get a Medigap policy:

-

Check your eligibility: First, you need to have Medicare Part A and Part B to qualify for a Medigap plan. If you're under 65, you might not be able to buy Medigap due to state laws. Check with your state's insurance department to see if you're eligible.

-

Understand the timing: The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This six-month period begins the month you're 65 or older and enrolled in Medicare Part B. During this period, you have a guaranteed right to buy any Medigap policy sold in your state, regardless of any health conditions. If you try to buy a Medigap policy outside this period, the insurance company might use medical underwriting and you might not be able to get a policy, or it may cost more.

-

Research plans: There are 10 standardized Medigap plans available in most states, labeled A through N. They offer different levels of coverage, but plans of the same letter offer the same benefits regardless of the company that sells them. Compare the different plans and consider your health needs and budget.

-

Choose an insurance company: Once you've decided on a plan, you'll need to choose an insurance company that sells that plan in your state. You can find a list of companies on your state's Department of Insurance website or the Medicare website. Compare prices because they can vary. Remember, each company may price policies differently, so it's a good idea to get quotes from several companies.

-

Apply for a policy: Once you've chosen a company and a plan, you can apply for a policy. The application process can vary by company. Some companies allow you to apply online, while others might require a phone call or a meeting with an agent.

Remember to always keep your current coverage until your new policy is in place to avoid any gaps in coverage.

Please note that these steps can vary depending on your specific situation and where you live. It's always a good idea to contact a trusted insurance agent or broker, or your local State Health Insurance Assistance Program (SHIP), for personalized advice.

Medicare Supplement Insurance Summary

-

Medicare Supplement Insurance, or Medigap, helps cover the out-of-pocket costs you’re responsible for after Medicare Parts A and B pay their share.

-

Plans are structured (standardized) the same in every state, except Massachusetts, Wisconsin, and Minnesota.

-

There are ten Medigap plans available as of 2019, but Medicare discontinues plans every so often.

-

Plan C and Plan F are being discontinued as of January 1, 2020 because of a federal law that says Medigap plans can’t cover the Medicare Part B deductible anymore.

-

If you enroll in a plan that is later discontinued, you don’t have to enroll in another one. You can still use your plan for as long as you want.

-

Medicare Supplement Insurance plans can cover things like the Medicare Part A and Part B deductible, copayments and coinsurances you have to pay for Medicare-covered services like inpatient hospital care, skilled nursing facility care, and outpatient medical services, among other costs.

-

Beneficiaries who foresee that they’ll need frequent inpatient care should look for a plan that covers the Part A deductible in total or in part.

-

Beneficiaries who will become eligible for Original Medicare after January 1, 2020 shouldn’t pick a Medigap plan based on whether it covers the Medicare Part B deductible, because no plans will cover this cost after 2019.

-

Beneficiaries who spend a lot of time outside of the United States should look into a plan that covers foreign travel emergency costs.

-

Your Open Enrollment period for enrolling in Medigap runs for six months starting on the month you are first covered by Medicare Part B.

-

Signing up for a Medicare Supplement plan during Open Enrollment ensures no insurance company can deny you coverage or charge you more for pre-existing conditions.

-

Companies can put you on a pre-existing condition waiting period, usually six months, but they can’t refuse to cover your condition after the period is up.

-

Enrolling in a Medigap plan after Open Enrollment, even if you already had a Medigap plan, gives the insurance company permission to evaluate you using medical underwriting.

-

Medical underwriting involves undergoing a physical exam, bloodwork, and other tests, as well as an examination of your medical records, to see if you are healthy or have pre-existing medical conditions.

-

Depending on the results of medical underwriting, you could be charged more for your Medigap policy or be denied coverage outright.

-

If you buy a Medigap policy during Open Enrollment, insurance companies can’t use medical underwriting.

-

There are other times when you can enroll in Medigap without having to undergo medical underwriting or a pre-existing condition waiting period. These are called Guaranteed Issue Rights.

Comparing Medicare Supplement Insurance to Medicare Advantage

Medicare Supplement Insurance isn’t the only alternative available for beneficiaries who are worried about covering those out-of-pocket costs remaining after Medicare pays its share. Medicare Advantage plans, also known as Medicare Part C, are health plans issued by a private insurer that cover your Medicare Part A and Part B benefits.

The Basics of Medicare Advantage

Medicare Advantage works pretty much like a regular private health plan:

-

The plan will issue you a card that you’ll present when you see a doctor or another provider; you won’t use your Medicare card while you have an MA plan.

-

You may have to pay a copay or coinsurance for certain services.

-

You may have to meet an annual deductible before the insurance company covers anything.

-

The plan will have an annual out-of-pocket maximum; once you reach this limit, you won’t pay anything for covered services and the insurer will pay for everything.

MA plans can’t cover less than Original Medicare, but they can cover more. Many MA plans include coverage for vision, dental, and hearing.

Depending on where you live and which insurance company you select, you may or may not have to pay a premium for your Medicare Advantage plan. This premium, however, is in addition to the Medicare Part B premium. Medicare Advantage does not cover your Part B premium.

The two main types of Medicare Advantage plans are Health Maintenance Organization (HMO) Plans and Preferred Provider Organization (PPO) Plans.

HMOs require that you use the insurance company’s network providers in order to be covered. You’ll have to select a primary care doctor and, whenever you need to see a specialist, you’ll have to visit your primary care doctor for a referral. Otherwise, the insurance company won’t cover the visit to the specialist.

PPOs, on the other hand, allow you to receive services from any physician in the plan’s network for the lowest copay and from any physician outside the network for a higher cost. You won’t need a primary care doctor to give you referrals to see a specialist. Most of the time, PPO premiums are higher than HMOs’.

PPOs and HMOs usually cover prescription drugs, so you don’t need to enroll in a separate Medicare prescription drug plan, like you would with Original Medicare and Medicare Supplement insurance.

You can enroll in a Medicare Advantage plan during your Initial Enrollment Period when you’re first eligible for Medicare. You can also enroll during the General Enrollment Period from January 1 to March 31, with your coverage starting on July 1. Finally, all Medicare beneficiaries can enroll in a Medicare Advantage plan, switch from one MA plan to another, or go back to Original Medicare during the Open Enrollment Period from October 15 to December 7, with your coverage starting on January 1.

Switching Between Medigap and Medicare Advantage

If you have a Medicare Advantage plan, you cannot sign up for a Medicare Supplement Insurance plan unless you’re planning to drop your MA plan and go back to Original Medicare. Medigap can’t help you pay for the copays and coinsurances you’re responsible for with Medicare Advantage.

If, on the other hand, you have a Medigap policy and you want to switch to a Medicare Advantage plan, you can do that during the Open Enrollment Period. However, you may not be able to go back to your Medigap plan if you change your mind. You only get a one-time pass to go back to your Medigap plan if you had Medicare Advantage for less than 12 months. Outside this time, you might not have guaranteed issue rights and may have to go through medical underwriting or even be denied coverage for a new Medigap plan.

Medigap vs. Medicare Advantage

Now that you know about both of your options, you might be wondering which is better.

Casey Schwarz, Senior Counsel for Education & Federal Policy at the Medicare Rights Center says there isn’t a single right answer for everyone.

“The choice between Medicare Advantage and Medigap depends not only on the policies that you’re looking at but also your individual priorities and values.”

When counseling people, she asks “whether someone would prefer to have higher monthly [premium] costs and lower cost when they see doctors and more flexibility,” says Schwarz, referring to Medicare Supplement Insurance, “or if someone would prefer to have lower premium costs with potentially higher costs when they access care and potentially more hurdles or steps that they need to take to access care.”

The best way to decide is to look at the main features of each type of plan side by side.

In summary, Medicare Advantage costs less upfront, but you may pay more when you seek services. Medicare Supplement Insurance is more expensive every month, but you will pay little, if at all, when going to a provider because the policy, depending on the plan you pick, covers most services at 100%.

Another consideration is the network limitations. If you live in an area with a large insurance network, or if you already know your doctors are in the plan network, you may opt for a Medicare Advantage plan. If you want the freedom to see any doctor anywhere in the country, then Medigap may make more sense.

If you take many prescription drugs, you may go with a Medicare Advantage plan that already covers prescriptions. Medicare Supplement Insurance will never cover medication. However, a Medicare prescription drug plan can cost as little as $15 every month. If prescription drug coverage is important for you, make sure whatever option you choose includes all your prescriptions in the drug formulary to reduce your out-of-pocket costs.

Likewise, Medicare Supplement Insurance doesn’t include coverage for dental and vision care, so you would need to purchase an additional plan to cover these costs, while some Medicare Advantage plans include this coverage in their policies.

Maureen Baxter, a financial consultant at the Commonwealth Financial Network with ample experience in Medicare insurance and retirement planning, suggests basing your decision on your medical history, personal preferences, and potential out-of-pocket costs.

“Once you narrow the choice to one or two [Medicare Advantage plans], analyze your potential out-of-pocket costs for these plans in relation to Original Medicare plus Part D and a Medigap policy,” says Baxter.

Choosing the Best Medicare Supplement Insurance Plan

Now that we’ve discussed what is Medicare Supplement Insurance and the plans available for Medicare beneficiaries, it’s time to help you figure out which policy to choose. Your decision is two-pronged: first, you must choose which letter plan is right for you, and second, you need to find the right insurance company.

Choosing the Right Letter Plan

When choosing a Medigap plan, think not just about your health care needs right now, but also about what they might be in the future. Consider your medical history; for example, the type of care your parents or siblings required when they got older.

Someone with a strong history of progressive or degenerative illnesses that require skilled nursing care should make sure to pick a plan that includes coverage for this type of care (all plans except Plans A and B).

Think about your lifestyle choices. If you are looking forward to traveling outside of the U.S. in your retirement, pick a plan that covers foreign travel emergencies. This benefit covers 80% emergency care outside of the U.S. if you require it during the first 60 days of your trip and once you meet an annual $250 deductible. This benefit is available with Plans C, D, F, G, M, and N.

If you are healthy and realistically foresee staying that way for a long time, you could opt for one of the cost-sharing plans, Plans K and L, which only cover part of your out-of-pocket costs but charge much lower premiums every month.

However, keep in mind that your care needs may change unexpectedly in the future: you could have an accident or be diagnosed with a serious illness. In many cases, your Medicare decision is final.

“There are only certain times when someone has a right to buy a Medigap [policy] without medical underwriting,” says Schwarz. “The decision you make when you’re first eligible for Medicare and enrolled in Parts A and B, depending on the state that you live in, might be the decision that you have for a while.”

Finally, if you’re interested in the most comprehensive plans, regardless of the cost, make sure to snag Plans C or F before they’re discontinued on January 1, 2020.

Choosing the best Medicare supplement insurance company

Once you know which plan or plans you’re interested in, it’s time to look for an insurance company. Since Medicare Supplement Insurance plans cover the same benefits, no matter which company is offering them, your decision will most likely come down to price.

Says Ms. Schwarz, “Medigap does not make any independent medical necessity determinations. All coverage determinations are made by Medicare, and if Medicare pays, then the Medigap pays. Aside from paying your monthly premium, the interaction with your Medigap company is quite limited.”

While insurance companies aren’t allowed to change the structure of standardized plans, they are allowed to charge different amounts, depending on the policyholder’s age and location. The way Medigap plans are priced is one of the most important factors when it comes to deciding from which company to buy a policy.

Pricing Types for Medigap plans

There are three methods insurance companies can use to set the premium for a Medigap policy. You should always know how an insurance company “rates” your policy so you are prepared for rate increases in the future. The three rating methods are:

-

Attained-age-rated: The cost depends on your age when you sign up for a policy and will increase as you age. Medicare notes that an attained-age-rated policy can have the lowest cost when you first enroll, but it can increase as the years go by until it’s very expensive. Other ways an attained-age-rated policy can increase its premiums is because of inflation.

-

Issue-age-rated (or entry-age-rated): The cost depends on your age when you sign up for a policy, but it will not increase as you age. It can increase because of inflation and other factors, but your age will never be a factor when calculating your premium.

-

Community-rated (or no-age-rated): The cost is the same for everyone with the same policy, no matter the age or gender. It can increase because of inflation, but everyone in the policy “community” will have the same premium.

Other Factors

Apart from how an insurance company prices its Medigap policies and how much they actually charge for their plans, there are a few things you might like to look at before making a final decision:

-

Discounts: Some insurance companies offer discounts to non-smokers, married couples who sign up for Medigap policies together, and women. Many also offer a premium reduction if you pay your premium annually or if you pay through direct debit.

-

Medicare SELECT Policies: Some insurance companies offer SELECT plans, which are identical to the standardized Medigap plans, but they require that you only see doctors within the insurance company’s network. They may also require you to get a referral from your primary care doctor before seeing a specialist. In this way, SELECT plans work like HMOs. These restrictions also mean they’re less expensive than regular Medigap plans.

-

Silver Sneakers Membership: The Silver Sneakers program encourages older adults to be physically active and healthier by providing access to thousands of fitness centers and classes across the country, as well as wellness discounts for select wellness products. Membership is available to Medicare Advantage and Medigap beneficiaries with certain insurance companies. The Silver Sneakers website lets you search for companies in your state that offer this benefit.

What To Watch Out For When Buying Medicare Supplement Insurance

The best thing you can do when it comes to signing up for Medicare Supplement Insurance is to get informed. Explore all the alternatives available to you, whether it’s Medigap or Medicare Advantage or anything in between. There are plenty of places you can go to get answers to your questions.

Medicare

Medicare.gov has a huge and comprehensive website that can answer most of your questions regarding Medicare benefits. You can read up on all your options, ask for assistance, request a new Medicare card, and initiate claims online. They also have a directory of Medicare-approved providers across the nation, from hospitals and physicians to skilled nursing facilities and hospices.

State Health Insurance Assistance Programs (SHIPs)

State Health Insurance Assistance Programs (SHIPs) are free counseling services dedicated to helping people like you learn more about Medicare. Their specialists can clear up questions regarding when you can enroll, change, or drop your coverage, whether you qualify for Medicare, and whether any specific services are covered by your insurance. Each state has its own SHIP, and you can find a complete directory on the program’s website.

Medicare Advocacy Groups

There are also advocacy groups for Medicare beneficiaries, such as the Medicare Rights Center, which are valuable resources that can help you find out more about your options and help you assess your situation if something goes wrong.

The Medicare Right Center has a National Helpline for beneficiaries, family members, and others who have questions about Medicare. They can help you get information on financial assistance programs to help you pay your Medicare premiums and deductibles, such as the State Medicare Savings Programs.

There may be other organizations in your state that could help you in a legal situation, like the Medicare Advocacy Center, which provides legal assistance to Medicare beneficiaries in Connecticut or your state’s legal aid society.

Financial Advisors

This isn’t the first thing people think about when they’re looking for help on Medicare topics, but the fact is that Medicare can be part of a larger retirement plan. Deciding on a type of Medicare insurance can have financial consequences ten or twenty years down the line.

A retirement planner can help you frame your Medicare choice in the right context.

“Healthcare needs can change in retirement. Each year, as part of your annual retirement plan review, you should analyze your Medicare decision,” says Baxter, who frequently discusses Medicare and other retirement topics on the Commonwealth blog.

On an annual basis, you should take a look at your medical expenses and calculate how much you paid out of your own pocket and how much Medicare covered (or failed to cover). Study your plan’s benefits and assess whether your needs are changing.

Baxter warns about changing your Medicare decision without asking the right questions: Depending on what your initial decision was, the insurance company may decide to medically underwrite your policy. “This means they can consider your current health condition and possibly charge a higher premium or deny Medicare Supplement coverage entirely.”

Shop around and request Medicare supplement insurance quotes

In the end, one of the best things you can do is to shop around. Request quotes from multiple insurance companies in your area and get all the relevant information (their policy rating method, available discounts, additional services, etc.) Base your decision on the largest pool of information possible.

FAQs about Medicare Supplement Insurance

How much is Medicare supplemental insurance?

The average cost of a Medicare supplement insurance plan can range from $150 to $200 per month.

However, the actual cost can vary widely based on several factors, including:

- The plan: Different Medigap policies have varying coverages, so premiums can vary from one plan to another.

- The location: Costs can also vary by geographic location. Some states have higher healthcare costs, which can result in higher premiums.

- The insurance company: Even for the same coverage, prices can vary between insurance companies. Some companies might also offer discounts.

- Your age: Some policies are age-rated, meaning the cost could go up as you get older. There are three ways insurance companies can price their policies: community-rated (same price regardless of age), issue-age-rated (price based on your age when you buy), and attained-age-rated (price goes up as you get older).

- Underwriting: If you apply for a Medigap policy after your initial enrollment period, the insurance company might base the price on your medical history.

Who regulates Medicare supplement insurance plans?

The Centers for Medicare & Medicaid Services (CMS) sets the basic standards for Medigap policies, which ensures that it's easy for you to compare coverage and price. For instance, CMS defines the benefits that must be included in any Medigap policy, and requires that these policies be clearly identified as "Medicare Supplement Insurance." Federal regulations also mandate that the basic benefit structure for each type of Medigap policy is the same, regardless of the insurance company that sells it.

While the federal government sets minimum standards, state insurance departments play a primary role in regulating Medigap policies. Insurance companies must be licensed by the state to sell Medigap policies, and the state insurance department monitors these companies for compliance with state laws and regulations. These can include rules about pricing, marketing, and consumer protections. The specific rules and level of oversight can vary from state to state.

Always remember to verify the legitimacy of any Medigap policy or insurance company with your state's insurance department before purchasing a policy.

When can I change my Medicare supplemental insurance plan?

You can apply to change your Medicare supplemental insurance whenever you want. However, there are some periods during which you have more protections:

-

Medigap Open Enrollment Period: This is the six-month period that starts the month you're 65 or older and enrolled in Medicare Part B. During this period, you can buy any Medigap policy sold in your state, even if you have health problems, for the same price as people with good health.

-

Medigap Free Look Period: If you decide to change your Medigap policy, you have a 30-day "free look period" to decide if you want to keep the new Medigap policy. This period starts when you get your new Medigap policy. You'll need to pay both premiums for one month.

If you want to change Medigap plans at any other time, insurance companies can use medical underwriting to decide whether to accept your application and how much to charge you for the Medigap policy. During the medical underwriting process, the insurance company reviews your medical history to decide if they accept your application, deny it, or will charge you a higher premium.

Your state may have additional protections or times of guaranteed issue rights — the rights you have in certain situations when insurance companies are required by law to sell you a Medigap policy. In these situations, an insurance company can't deny you a policy, or place conditions on a policy, such as exclusions for pre-existing conditions. They also can't charge you more for a policy because of past or present health problems.

I’m a veteran, can I get Medigap?