Best Student Loan Refinance

Based on In-Depth Reviews

A comprehensive guide to choosing the best student loan refinance option for your needs and budget.

Last Updated:July 28, 2026

- 200+Hours of Research

- 20+Sources Used

- 13Companies Vetted

- 4Features Reviewed

- 10Top

Picks

Our Team of Researchers:

Our Site is Referenced By

Consumer Advocacy

What you need to know

Student Loan Refinance

- Refinancing can help lower your monthly payments

- A good credit score and a high salary are key for loan approval

- You can lose benefits by refinancing a federal student loan

- Avoid lenders that charge hidden fees or prepayment penalties

Our Approach

How we analyzed the best Student Loan Refinance Lenders

Loan Specifications

When choosing a student loan refinance lender, it’s important to compare the different loan options available and fully understand their terms. This includes the types of loans that can be refinanced as well as their loan limits, term lengths, fees, interest rates, and other variables.

Eligibility Requirements

The qualification requirements for refinancing, especially if you're looking for a lower interest rate, can be fairly strict. It’s best to understand the lender's eligibility requirements, such as their minimum credit score and annual income, before applying.

Customer Experience

Features that benefit consumers and contribute to a convenient customer experience should be a plus for any borrower. The customer experience can be enhanced with features such as a live chat, flexible customer support hours, online tools and resources, and a streamlined application and approval process.

Reputation

Transparency and verifiable information are key indicators of a company's reputation. We also take into account customer reviews and complaints from authoritative sources, such as the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB).

136 People found this helpful.

We receive compensation from these partners, which impacts the order they appear on the page. That said, the analyses and opinions on our site are our own and we believe in editorial integrity.

Our Top Picks: Student Loan Refinance Reviews

When we set out to compare the best student loan refinance lenders, we were taken aback the amount of misinformation and lack of transparency in the student loan industry. We quickly realized there are key questions student borrowers are asking, and many providers are now attempting to answer some of those questions and cater to a new generation of customers who are looking for clear guidance and unbiased information.

If you've ever considered refinancing your student loans, then this guide is for you. Here we break down the most important things to consider before opting to refinance and alert consumers to some industry trends to watch out for. We also review some of the top players in the student loan refinance industry, highlighting where they stand out and what they can do to improve. We also place a lot of emphasis on four key factors we think you should be very mindful of in your search for the right lender: loan specifications, eligibility requirements, customer experience, and company reputation.

This site does not include all companies or all available offers. Companies listed below are listed in alphabetical order.

CommonBond review

Best for Financial Hardship Assistance

It’s extremely rare for a private lender to offer hardship assistance, especially for an extended period. In this respect, Commonbond stands out from the crowd by allowing borrowers to pause payments for 3 months at a time and up to 24 months over the life of the loan.

This hardship assistance option can serve as a safety net for emergencies such as unemployment or illness, which can temporarily prevent an individual from making payments on time. We find this to be an excellent and rare feature, especially for a private lender.

Rate Flexibility

Student loan providers typically offer either variable or fixed rates. Commonbond, however, offers a hybrid option in addition to these two. Rates through this lender are customizable, allowing borrowers to choose the loan term and type of rate that best fits their needs.

Commonbond also allows prepayments, meaning borrowers are not penalized for paying their loan off ahead of time, for which many private lenders charge penalties.

Room for Improvement

Applicants should be aware that Commonbond doesn't offer loans in Mississippi, Nevada, or Vermont.

Their website is minimalistic and easy-to-navigate, but it doesn't provide enough information about the refinancing process, pre-approval process, or explanations about the hybrid rates. The disclaimers page does provide more detailed information, but it's not easy to locate. Also, eligibility requirements are not listed on the website.

We had to confirm the minimum credit score, which is 660, with a representative via live chat. They also confirmed only U.S. citizens or residents with a college degree may qualify for refinancing through Commonbond.

The company's additional educational resources are also very limited; both their FAQs and blog pages are short and only cover general questions.

This lack of easily-accessible information may be Commonbond’s way of encouraging consumers to call and speak with their customer service representatives. However, for a company offering a loan application process that's entirely online, clear guidelines and resources should be easy-to-find.

CU Student Choice review

CU Select Student Loan Refinancing Review:

CU Select connects borrowers with a network of credit unions offering student loan refinancing. This platform emphasizes community-focused lending, competitive rates, and personalized service, making it a solid choice for borrowers who value local financial institutions.

Rates and Terms:

CU Select’s partner credit unions offer fixed and variable interest rates starting at competitive levels, with loan terms ranging from 5 to 20 years. Borrowers may find lower rates than those offered by traditional banks.

Eligibility:

Eligibility criteria vary by credit union but typically include a solid credit history, stable income, and U.S. citizenship or permanent residency. Some credit unions require membership, which may be based on location or other factors.

Key Features:

CU Select provides access to local credit unions with competitive rates, no origination or prepayment fees, and personalized service. However, borrowers refinancing federal loans lose access to federal repayment plans and protections.

Who It’s Best For:

CU Select is ideal for borrowers who prefer working with community-focused credit unions and seek competitive rates with personalized service. It’s a great fit for those eligible for credit union membership and looking to support local financial institutions.

LendingTree review

Best for User Experience

We believe informative content is the root of great user experience. Consumers should know what they’re getting themselves into, including the good and the not-so-great about the companies recommended to them.

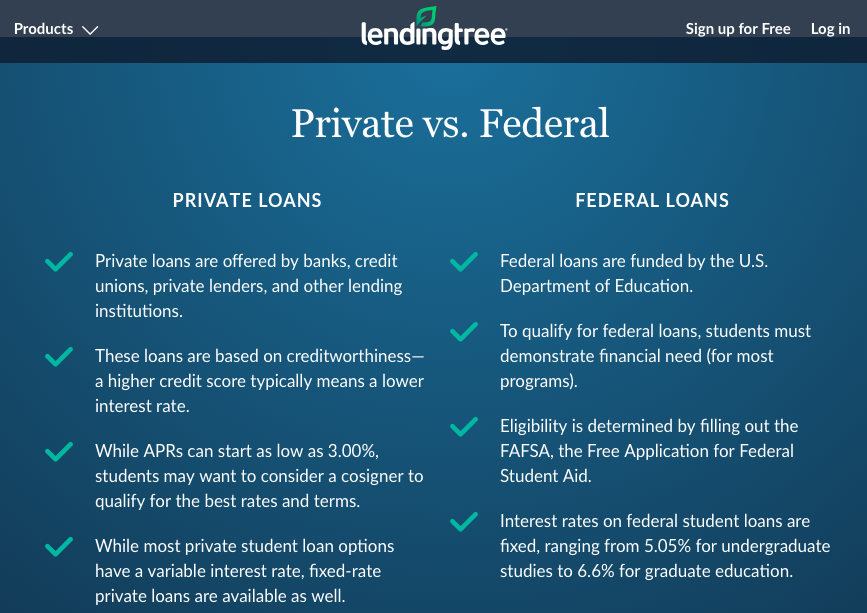

Lending Tree does an exceptional job in this area, carefully phrasing their content to inform and educate consumers without bias. Their website provides in-depth explanations about the differences between loan consolidation and refinancing, federal and private loans, the pros and cons of each option, and even some alternative solutions.

Explanation of private vs. federal loan types by LendingTree

Helpful Resources

Lending Tree offers a wealth of resources and several educational online tools. Accessible across multiple social media platforms, the company provides financial tips and advice by way of posts, articles, and even Pinterest photos.

Lending Tree also encourages customers to write and leave reviews on their website, sharing their experience with the lenders they've been matched with.

Room for Improvement

Having been in business for over 20 years, Lending Tree is a major networking platform affiliated with multiple websites, including SimpleTuition, ValuePenguin, and QuoteWizard.

While this can be a plus, a potential downside is that prospective borrowers can be swayed to do business with a lender due to its popularity as opposed to its reputation.

In the course of our research, we noticed that customer reviews across Lending Tree's social media platforms are nonexistent, most likely hidden, which isn't helpful to consumers searching for honest feedback from previous customers.

LendKey review

Best for Educational Resources

LendKey is a New York-based online student loan marketplace that helps consumers connect with over 300 lenders and compare refinancing options.

For those new to refinancing, LendKey has a plethora of educational resources on the subject. From a refinance guide to a walk-through informational video, prospective customers can easily navigate to a topic they're interested in and make a better-informed decision.

Guides, loan calculators, and more on LendKey’s Resource Center

We found the blog posts in their Resource Center to be helpful and informative. Their “Ultimate Guide to Student Loan Refinancing,” for example, contains vibrant visuals with statistics, frequently asked questions, and a flowchart quiz to help readers determine whether refinancing is right for them.

Payment Flexibility

In addition to its helpful resources, LendKey offers borrowers a unique repayment option for their loan term: interest-only payments.

Unlike most lenders who only offer term flexibility, LendKey allows borrowers to pay off loan interest for the first four years. This makes repayment over the remaining loan term easier, as interest no longer accumulates.

Room for Improvement

While looking through hundreds of consumer reviews, we noticed that the majority of customer complaints against the company involved billing issues and difficulty making payments.

We advise consumers to speak with a Lendkey representative for more information about their repayment options and payment methods.

PenFed Student Loan Refinancing review

Best for Married Couples

Purefy is a fintech student loan lender in partnership with Pentagon Federal Credit Union (PenFed). They began offering student loan refinancing in 2017.

Unlike most lenders, Purefy offers a one-of-a-kind solution for married couples with student loan debt: the Couple Loan. This loan refinance option combines the student loans of both individuals and uses the higher credit score and college degree of the two to determine their rate. This helps couples save on interest costs and decrease overall household debt.

Transparency

Reviewing Purefy’s website was a breeze. Our team was impressed with the company’s in-depth explanations regarding the student loan refinance process, common industry terminology, and eligibility requirements. We encountered no misleading content or call-to-action phrases, which are common in the industry.

Purefy explains the logistics of student loan refinance

Purefy’s FAQs page also contains helpful, thorough answers covering everything from the basics of student loans and refinance to the application process and loan servicing after approval.

Room for Improvement

Since Purefy is in partnership with PenFed, only credit union members are eligible to apply. Fortunately, applicants can become members during the application process and the steps to membership are easy. No military affiliation is required.

We discovered, however, that applicants with a credit score of 670-699 still need a cosigner to apply, where most other private lenders allow borrowers with that score to apply on their own. Therefore, interest rates will be based on the cosigner’s eligibility for the life of the loan.

SoFi review

SoFi® is a leading online lender offering student loan refinancing with competitive rates and exclusive member benefits. Known for its streamlined process and financial perks, SoFi caters to borrowers seeking flexibility and support beyond refinancing.

Rates and Terms:

SoFi provides fixed and variable interest rates starting as low as 3.99% and 5.74% respectively, with autopay. Loan terms range from 5 to 20 years, allowing borrowers to tailor repayment plans to their needs.

Eligibility:

Applicants need a solid credit history, stable income, and an associate degree or higher. Co-signers can improve approval chances.

Who It’s Best For:

SoFi is ideal for borrowers with strong financial profiles looking for competitive rates and added perks. Its comprehensive benefits make it especially appealing for those seeking more than just lower interest rates. SoFi’s intuitive platform and top-notch customer support further enhance the refinancing experience, making it a great choice for borrowers prioritizing ease, value, and long-term support.

Our Research

More insight into our methodology

While researching the student loan refinance industry, we noticed a startling trend among student borrowers who left online feedback for their lenders across a number of consumer review platforms. It seems there is a lot of misinformation out there, and borrowers are confused about interest rates, repayment terms, and even financial hardship options. Many ignore the fact that, while refinancing can help borrowers obtain a lower interest rate and decrease their monthly payments, refinancing a federal student loan into a private one can cost them benefits like the option to apply for deferment, forbearance, or an income-based repayment plan.

We interviewed experts who confirmed that the problem of misinformation in the industry is twofold. While student borrowers are responsible for educating themselves about their options before making a decision, some lenders don't make it any easier for their customers to find the information they need to make an informed decision. With this in mind, we set out to find the most relevant information about student loan refinancing, including the reputation of some of the most popular online lenders, their loan specifications, eligibility requirements, and customer service standards.

In this guide, you'll also find essential information such as the pros and cons of refinancing, when it's best to consider this option, and how to identify companies who could be looking to take advantage of consumers, among other relevant details.

Loan Specifications

The ultimate goal of student loan refinance is to save money. Be sure to consider how much money you will save through refinancing. Also, pay close attention to the repayment terms and conditions of the new loan.

Our team identified the refinance options available, looking into loan amounts, types of loans, fees, and term length—especially if there is flexibility concerning repayment.

Loan Amount

Since many lenders have a minimum and maximum loan amount they’re willing to lend a borrower, we consider this factor. There is a wide range of loan amounts available depending on the borrower's education, degree, and years in school. During our research, we looked at companies that catered to a broader consumer segment by offering several loan amount options.

Types of Loans

Similar to loan amounts, there are several different types of student loans available. The type of loan will depend on the borrower’s level of education and degree, as well as the lender’s interest rates, which are the portion of a loan charged by a lender for the use of its funds. Interest rates vary by lender and loan type.

We pay special attention to borrowers willing to refinance a broader range of loan types. Listed below are the most common types of student loans eligible for refinancing:

- Undergraduate Loans: are designed to finance studies at degree-granting higher education institution, including Associate’s and Bachelor's degrees.

- Graduate Student Loans: are intended to cover tuition expenses for masters and doctorates degrees.

- Federal Loans: are available through the U.S. government’s Department of Education

- Parent PLUS Loans: are federal student loans given to parents of dependent, undergraduate students to help pay for their child’s educational expenses.

- Private Loans: are funded by private lenders like banks and credit unions to cover tuition expenses.

Term Length

The term of the loan is the length of time in which a borrower agrees to pay back their loan in full. This is another factor we take into account when reviewing student loan refinance providers.

Most lenders offer between 5 and 20-year terms. Shorter terms typically translate into higher monthly payments and lower interest charges, while longer terms translate into lower monthly payments and higher interest charges.

We searched for flexibility in this area, prioritizing lenders that allow their customers to choose the term length that works best for their budget.

Fees

Another critical factor is the fees. Lenders charge fees for several reasons, from originating a loan and processing paperwork to servicing a loan after origination and processing late payments:

- Application Fee (aka Origination Fee): an upfront fee charged to a potential borrower intended to pay for the costs of the application and loan approval process. This fee is added to the total loan amount.

- Interest Rate: an upfront fee charged by a lender for processing a new loan application.

- Late Payment Fee: a fee charged when the borrower does not pay on time or within the grace period. Some late fees can be up to 5% of the payment due.

- Collection Fee: fees charged and added to the loan balance if the borrower fails to make multiple payments after a prolonged period. The lender will notify collection agencies, which charge up to 40% of the loan balance. This will also negatively impacts the borrower’s credit score.

- Prepayment Penalty: a fee charged when a borrower makes early payments or pays off their loan earlier than the agreed term. Fortunately, the Higher Education Opportunity Act of 2008 made it illegal for lenders to charge prepayment penalties on all education loans.

While some fees are bound to happen, others—such as loan application and processing fees—are unnecessary. General loan fees include loan application fees, processing fees, late payment fees, and collection fees, which only accrue when the borrower fails to make several loan repayments.

When looking for the most reputable companies in the student loan refinance industry, we suggest going for a lender that clearly states and explains any applicable fees or shows greater flexibility in this area by doing away with unnecessary costs such as application fees.

Eligibility Requirements

Refinancing a student loan means converting the loan from a federal one to a private one.

There are several differences between federal and private loans, the main ones being that federal student loans come with terms set by the government and will have fixed interest rates and income-driven repayment plans.

Under a new refinanced loan with a private lender, most borrowers will no longer have access to benefits usually offered under federal student loans, including deferment, forbearance, and the income-based plans mentioned above, which are available for those under financial hardship.

To ensure they’re lending money to a borrower who won't default on their loan, lenders expect applicants to meet certain qualifications. These requirements are aimed at determining whether an applicant can repay a loan on time. These typically include:

- U.S. Citizenship and/or Permanent Residency status

- College Degree and/or current enrollment status

- Credit score above 650

- Proof of sufficient income or job offer

- Low debt-to-income ratio

For individuals who have a credit score lower than 650, many lenders accept co-signers added onto the loan for approval. A cosigner, who has an established credit history and source of income, can help the borrower receive a lower interest rate. Also, they can help the borrower get approved for a higher loan amount.

Nevertheless, there are still risks involved. Some private lenders do not offer cosigner release, meaning the cosigner must be tied to the loan for the remainder of the term. If the borrower is unable to make payments on time or any at all, the cosigner is required to pay. This can negatively impact the co-signer’s credit and become a financial strain if the borrower falls behind on payments.

Customer Experience

We believe high customer service standards are essential for a great user experience. Borrowers want to know they’re doing business with a company that has their best interest in mind, and that’s what we look for in a lender.

Competitive lenders seek to provide special features and benefits that make their products more attractive to prospective borrowers and encourages customer loyalty. This is especially true in the student loan market.

Online Quotes

Private lenders often provide online quotes before prospective borrowers start the application process. These quotes detail the terms of the loan and the interest rate a borrower would qualify for based on their personal details and the loan amount they want to refinance.

Benefits

Some lenders offer discounts for borrowers who sign up for online automatic payments, which can be a win-win for both parties. Other companies also have referral programs in which borrowers can receive a bonus for anyone they refer to do business with the company.

To remain competitive in a saturated market, certain lenders may also waive application and processing fees or offer discounts, which vary from one provider to the next and may not be available to all borrowers.

Resources

Online tools and resources, such as glossaries with common industry terminology, rate comparison tools, and educational material in the form of articles or blog posts, are a plus for consumers, especially for those new to refinancing.

Loan refinancing calculators, for example, are a popular tool that allows prospective borrowers to get a better idea of their monthly repayment amount. This can be extremely helpful for borrowers who are still unsure of whether refinancing is their best option.

Ways to Reach Out

It's a red flag when companies don't give their customers a way to reach out for assistance. Lenders that offer 24/7 customer support and multiple channels of communication—a live chat and the option to call or email—demonstrate their commitment to helping customers by providing ongoing support.

Reputation

Last, but not least, we take into account the lender’s reputation within the industry. Reputable companies are transparent regarding their products, services, prices, and background. One should be able to find general information online about the company their products without difficulty.

We spoke to Delaney Lynch, Head of Partnerships at Earnest, who told us about the value of consumer insights. According to her, consumer reviews can reveal a lot about a company's practices and their efforts to educate customers. Reading online customer reviews can also be a great way to learn about the industry as a whole and make better-informed decisions.

"A fantastic resource is going online and reading consumer reviews. Do so with an objective eye, discerning customer circumstances from larger business practices. This can be extremely insightful and give you a better idea about which lenders have resources to help you educate yourself."

- Delaney Lynch, Head of Partnerships at Earnest

Other sources we typically verify are from the three major consumer review platforms: the Federal Trade Commission (FTC), the Consumer Financial Protection Bureau (CFPB), and the Office of the Comptroller of the Currency (OCC).

These sources offer unbiased information about consumer protection and loan regulations. Unlike other online review platforms, these agencies do not sell ratings or accreditations. Consumers can also share their experiences with and concerns about companies on the FTC and CFPB websites.

Helpful information about Student Loan Refinance

As a nation, the U.S. is facing a massive, student loan debt crisis. As of 2019, student loan debt totals to over $1.3 trillion. Furthermore, according to Pew Research Center, an estimated 4 in 10 adults under the age of 30 have student loan debt.

While postgraduate education—master’s and doctorate degrees—is believed to be the gateway to a better life, financially speaking, postgraduate students make up the larger percentage of the country's student loan debt.

Those who hold undergraduate degrees have a median of $25,000 in student loan debt. In comparison, borrowers with postgraduate degrees have an average of $45,000 to over $100,000 in student loans.

Millions of people across the U.S. are struggling to pay back their student loans and seeking a solution to regain control over their finances and improve their standard of living. Refinancing may be a smart solution for some of them. Let's go over this option in detail to determine whether it's the right one for you.

Student Loan Refinancing 101

Student loan refinancing involves replacing a borrower’s existing loan (or loans) with a new loan featuring a different interest rate and term length.

Typically, the goal of refinancing is to obtain a lower interest rate, thereby decreasing monthly payments and saving money over the life of the loan. Refinance lenders make a profit from interest payments, which is the cost you pay for borrowing.

To help you better understand student loan refinance, we’ve broken the topic down into six essential questions:

Who Can Refinance Their Student Loans?

Fundamentally, refinancing a loan is the same as applying for one. Since you’re replacing your old loan with a new one, you still have to prove to the lender that you are financially responsible and able to pay back what you borrow.

Just as with any other type of loan, borrowers must meet certain qualifications requirements before they're approved for refinancing.

Generally, lenders require their borrowers to be citizens or permanent residents who’ve already graduated and hold a college degree. Some lenders are more lenient, however, permitting students who are currently enrolled in their last year of school to apply.

Lenders also generally require borrowers to have sufficient income and a credit score of 670 or higher. You may find that some lenders accept loan applications from individuals transitioning into a new job or who have recently started one at the time of application. Still, borrowers will be required to show proof of employment by way of a job offer letter.

Lastly, most lenders will check your debt-to-income ratio, which is your current total debt against your total income, as well as any bankruptcies you've had in recent years. Together, all of these requirements help lenders determine your financial stability and creditworthiness.

"I think they [consumers] should compare lenders, and also their eligibility criteria, in order to get pre-approved. Most student loan refinance lenders have pretty strict criteria, so it makes sense to check out the eligibility criteria of each lender before applying so you’re not enduring a hard credit pull. Also, look at the pricing, interest rates, and terms offered. Some lenders have standard rates, but others are more flexible."

-Brian Attridge, Senior Vice President of Business Operations at Purefy

If you currently have a lot of debt, such as car loans, credit cards or medical bills, it may not be a good idea for you to refinance your student loans. Neither is it a viable option for individuals who are unemployed, going through financial hardship or have a spotty payment history or low credit score.

Remember, lenders want to make sure you're a responsible borrower who won't default on their loan. To improve your odds of approval and get the best possible rate through refinancing, it’s best to wait until you’ve secured a stable job, paid off some of your debt, and improved your credit score.

What's the Difference Between Refinancing and Consolidation?

Although used interchangeably by some, refinance and consolidation are not the same thing. When you consolidate your student loans you're rolling all of your existing loans into a single one. This consolidated loan will have an interest rate that's based on the weighted average of the interest rates of the other loans before consolidation.

In that sense, consolidation is a way to simplify monthly payments for borrowers who have multiple loans and are having a hard time keeping up with separate payments, while refinancing is replacing an existing loan with a new one featuring a different rate and terms.

Borrowers can consolidate all of their federal student loans through a Direct Consolidation loan or consolidate all of their private student loans through a private lender. Consolidation becomes refinance only when you’re requesting a completely new interest rate and term length. Many borrowers choose to consolidate both their federal and private loans under a new private loan before refinancing.

When Should I Refinance?

Referring back to eligibility requirements, it’s best to refinance your student loans when you have a sufficient income, a good credit score, have paid down other forms of debt, and can make timely payments without compromising your finances.

If you’re financially stable immediately after graduating college, have considered the pros and cons of refinancing, and decide that refinancing your student loans right away is your best option, don't hesitate to do so.

The decision to refinance is at the discretion of the borrower. Just be aware that you have the potential to save a lot of money by refinancing early on as opposed to waiting for a few years.

Where Do I Apply?

You can apply to refinance your student loans directly with the lender of your choice. Most student loan refinance providers offer borrowers a complete online application process with no-obligation quotes and the ability to submit all the required documentation via their secure platform.

Borrowers can also call customer service or visit banks and other types of lenders in person at their nearest branch to start the application process. Make sure you’ve read all of the lender’s eligibility requirements and asked any questions you may have had about the application process beforehand.

Why Should I Refinance My Student Loans?

As we've mentioned above, when borrowers choose to refinance their student loans, they have the opportunity of paying a lower interest rate under a new loan with new terms.

A lower interest rate will translate into lower monthly payments, which can save borrowers a lot of money over the life of the loan. On the other hand, a borrower can refinance to obtain a shorter loan term if they want to pay off their debt sooner or want to remove a cosigner.

How Do I Know I Made the Right Decision?

Determining if you’ve made the right call by choosing to refinance will come down to your comfort level with the new lender and payment plan. As Delaney from Earnest put it, "you know better than anyone what you can pay each month. Having a solid understanding of your full financial picture is extremely important when it comes to refinancing."

When searching for a good lender, look for companies that offer flexible rates and adjustable term lengths. Also, consider lenders that don't require application or processing fees, as this will save you money in the long run.

Also, keep in mind that there are risks to refinancing your student loans. Private lenders offering hardship and forbearance options are rare in the industry.

If you decide to refinance your federal student loans under a new private loan and are later unable to make timely payments, you won't be able to apply for an income-based repayment plan, forbearance, deferment, loan relief, forgiveness, or other hardship benefits.

All the benefits mentioned above are offered under federal student loans only. Also, if you choose to refinance, there are no guarantees that your new interest rate will be lower than your current one. Lastly, you may not be able to claim your new private loan under the student loan interest tax deduction.

Additional Facts Consumers Should be Aware of

Before opting to refinance, borrowers should carefully assess their financial situation and the terms of their current loan(s).

Consolidation is another option, which also has the possibility of lowering your interest rate once averaged. If you’re still interested in refinancing through a private lender, bear in mind that, just as with any other type of loan, the lender will look at your credit and employment history, debt-to-income ratio, and even your educational background.

While some lenders only require the applicant to have completed a college degree, others may only accept high salary earners, which proves to lenders you’re more likely to repay your loans in full and on time. Not all lenders have strict eligibility requirements, but most will look at payment and credit history to ascertain the risk involved in lending to a potential borrower.

Student loan refinancing is an industry-wide practice founded on the fact that student loans are unsecured debt instruments. That means they require no collateral (such as a house or other assets) that the lender can use as compensation in the event the borrower defaults.

We always strongly recommend that borrowers read the terms of their new loan carefully, especially the annual percentage rate (APR). If you're looking to get acquainted with common student loan terminology you can read our article on the subject or look for online sources that can help you better understand the terms of you loan.

What To Watch Out For When Refinancing a Student Loan

Student loan debt is a rising figure in the list of U.S. consumer debt, surpassing credit card debt and falling just below auto loan debt. As the crisis aggravates, the popularity of student loan refinancing increases.

Despite its popularity, student loan refinance is a risky industry. There is no guarantee that you’ll receive a lower interest rate or better repayment terms. If you're not careful, you may find yourself in a worse financial situation down the road.

While most homeowners generally understand the concept and benefits of mortgage refinance, student loan refinance is not a topic most student borrowers are well versed in. For example, many aren't aware of the fact that federal student loans have flexible repayment options.

Those who have taken out a federal student loan and are financially unstable or have experienced life-changing events that have hindered their ability to make timely loan payments have the option to apply for loan deferment or an income-based payment plan.

Federal student loan cancellation, discharge, or forgiveness might be an option under particular circumstances outlined by the U.S. Department of Education. Eligibility requirements for these benefits can be strict, but so can the requirements for student loan refinancing for average student borrowers.

While our team researched and dove deep to summarize the most important things to keep in mind regarding student loan refinancing, we still encourage consumers to carry out their own research and look closely at the terms and rates offered by each company they consider.

Student Loan Refinance Scams

Consumers should know there are businesses and programs that take advantage of the student loan debt problem, targeting individuals who are desperate to get rid of debt and solve their financial problems.

Some companies are complete scams, taking money from individuals seeking assistance in student loan debt relief and disappearing afterwards.

Others are legitimate, legally performing businesses, that still take advantage of consumers by charging them for services that are generally free. With that said, here are several red flags and warning signs to look out for:

- You have to pay upfront to get help

- The company promises immediate loan forgiveness

- There's pressure to sign up

- They ask for sensitive personal information without stating why they need it

- They contacted you without you seeking out their services in any way

- There is little or no information about the company online

While there isn’t a one-size-fits-all situation, there are warning to keep an eye out for. Educate yourself as much as possible about student loans and student loan refinancing beforehand, checking reputable consumer protection sources such as the CFPB.

Most importantly, trust your instincts. If you get a bad feeling about a company, it might be best to walk away and consider other options.

Misleading Information

Some legitimate lenders and student loan refinance providers use misleading wording in their advertisements and website content to attract consumers.

Phrases such as “save thousands of dollars” and “get a lower rate” can be deceptive, as there is no guarantee that every customer will in fact get a lower rate.

SoFi, for example, was charged by the FTC in 2016 for false and misleading advertisements about student loans. The charge was settled in 2018 and the company has since updated their website content and eliminated misleading language.

Even online tools, such as student loan refinance calculators, can be deceptive to the uninformed. Some calculators show prospective borrowers how much they’d save by comparing their current student loan rate with an example low interest rate.

According to Attridge, when you see the lowest rate that lenders offers, that is usually the variable rate and the shortest term for that lender. A lot of lenders use that lowest rate to tease the borrower, but you usually need an 800+ FICO score and meet other strict eligibility criteria to qualify for that.

These things shouldn't be a problem so long as consumers understand that while low rates are possible, they’re not always probable.

Another thing to keep in mind is that a lower interest rate doesn't necessarily guarantee a shorter loan term. If you extended your loan term from 15 to 30 years, for example, you'd have a lower monthly payment but would be paying more toward interests over the life of your loan.

Online Reviews

Online customer reviews can shed light into company practices and help borrowers make better informed decisions. However, consumers should be aware that not all review sites are as transparent as they appear to be.

For example, some sites grant accreditations or give higher ratings to companies that are willing and able to pay for them, while others post only positive reviews and leave out any negative feedback. This last example can be especially true on social media pages.

You may come across businesses that have good letter or number ratings, but an alarming number of customer complaints and negative reviews. In such cases, read the reviews and complaints and notice whether or not the company has taken the time to reply to them.

While not all companies with negative online reviews are bad. Some experts suggest about 10% of satisfied customers leave good reviews, while customers who've had negative experiences are highly likely to share said experiences through unfavorable reviews.

The best way to navigate through online customer reviews is to take both positive and negative feedback with a grain of salt and to ask people you know about their experience with the providers you might be considering.

FAQs About Student Loan Refinance

Can I still apply for an income-based payment plan if I refinance?

Income-based payment plans are generally only available through federal student loans. When an individual decides to refinance their loans, they’re receiving a new loan and interest rate from a private lender.

Some private lenders do, however, offer some type of assistance for those experiencing economic hardship.

Commonbond, for example, offers loan forbearance, which is postponement or reduction of payments, up to two years if the borrower qualifies. Keep in mind, their offer does not exceed two years.

If you believe an income-based plan is better for your current financial situation, or that at some point you may not be able to afford your monthly payments, it may not be a good idea to refinance.

Can I refinance if I filed for bankruptcy?

Refinancing a student loan after filing for bankruptcy can be difficult, but not impossible.

Bankruptcies remain on your credit history for seven years (Chapter 13 filing) or ten years (Chapters 7 and 11), so every time you apply for credit, the financial institution will see the record and take it into account when considering your application.

A bankruptcy also lowers your credit score, sometimes by as much as 200 points.

However, as the years pass and you consistently make timely payments on your existing accounts, the bankruptcy’s impact is lessened and applying for credit becomes easier.

Many lenders place a time limit before you can refinance, often three or five years.

Applying with a cosigner can increase your chances of approval and get you a lower interest rate because the person’s credit history and FICO score are considered alongside yours.

What’s the difference between consolidation and refinancing?

Refinancing refers to replacing a current loan with a new loan for the purpose of reducing the interest rate, extending the loan repayment term, changing the lender, or removing a cosigner, among other reasons.

The process consists of taking out a new loan for the total amount due in the current loan and using the money to pay off the debt, essentially replacing it.

One may refinance personal loans, car loans, mortgages, or student loans.

Consolidation, though similar in method, is primarily a way of reducing the number of debt obligations by replacing several loans with a single loan.

Many people use consolidation loans to manage their debt when, for example, having to make multiple monthly payments with different due dates becomes confusing.

In the process of consolidating, however, one can obtain many of the benefits of refinancing (lower interest rate, longer term, etc.)

Will refinancing hurt my credit score?

Refinancing affects your credit, but not necessarily in a bad way. When you apply to refinance (just as you would when applying for any kind of loan), the lender will make a hard inquiry into your credit report, which will decrease your credit score by a few points.

These points, however, are usually restored within a few weeks, so your score doesn’t take a permanent hit.

If you apply for refinancing with several different lenders, you may lose more points in the same way, which should return to normal after a short period.

On a positive note, refinancing can help boost your credit score as well. If you receive a lower interest rate or a lower monthly payment with the new refinanced loan, it may be easier for you to stay on top of your monthly payments.

Paying on time every month will make a good impact on both your credit history and score.

Can I refinance my student loan without a college degree?

Unfortunately, most lenders require that you have a degree from a qualifying institution before you can refinance your student loan.

There are some lenders out there, such as Laurel Road and Earnest, that allow individuals who are currently enrolled in school and pursuing their degree to apply for refinancing.

Typically, borrowers without a college degree must meet additional requirements, such as having made a minimum of 12 timely payments before refinancing, while individuals with a degree from an accredited university are usually only required to make three payments.

How can I qualify for student loan refinancing?

To qualify for student loan refinancing, you must meet your lender's requirements, which vary from one provider to the next. Most lenders require borrowers to be 18 years of age and a U.S. citizen or permanent legal resident.

Lenders will also look at a borrower’s credit history to analyze consistency in making on-time payments. Lenders also request proof of employment and income, which is used to calculate their debt-to-income ratio. Additionally, most lenders require borrowers to have a degree from a qualifying institution or currently pursuing a degree.

There may be additional requirements, such as a minimum credit score, a minimum and maximum refinance limit, and state of residence, as some lenders may not be licensed to operate in all 50 states.

Can I refinance a federal student loan?

The Department of Education doesn't have a loan refinancing program in place because every student borrower receives the lowest possible interest rate the first time around.

That means that if you want to refinance your student federal loans you'd have to convert them into a private loan funded by a private lender.

Those interested in refinancing their student loan(s) should keep in mind that private interest rates tend to be higher than federal interest rates.

Federal rates are lower because your credit score isn't the deciding factor, and most students don't have excellent credit scores.

Also, turning your federal loan into a private loan means you will lose many of the benefits of federal loans, such as loan forgiveness programs, deferment, and special repayment plans.

Nevertheless, the Department of Education has a Direct Consolidation Loan, which borrowers can use to combine several federal student loans into a single loan.

The interest rate of a Consolidation Loan is be calculated by averaging the interest rates of all the borrower's loans, which won't necessarily mean a lower monthly payment unless the repayment term is extended.

Can I Save Money by Refinancing My Student Loans?

The two main reasons people refinance student loans—or any loan in general—are to lower the interest rate or change the loan term.

A lower interest rate means you could pay less over the life of the loan. With a longer loan term you might end up paying more for what you borrow through interest payments, but your monthly payments will likely be lower.

Many people wait until their credit score has increased and they have secured a higher salary before refinancing, which can improve their odds of getting a lower interest rate.

Our Student Loan Refinance Review Summed Up

| Company Name | Best for |

|---|---|

| ELFI Student Loan Refinance | Customer Service |

| Laurel Road Student Loan Refinance | Flexible Eligibility Requirements |

| CommonBond Student Loan Refinance | Financial Hardship Assistance |

| PenFed Student Loan Refinancing (powered by Purefy) | Married Couples |

| LendKey Student Loan Refinance | Educational Resources |

| Earnest Student Loan Refinance | Additional Benefits |

| SoFi Student Loan Refinance | Medical Students |

| Credible Student Loan Refinance | Loan & Lender Comparisons |

| LendingTree Student Loan Refinance | User Experience |

| Splash Financial Student Loan Refinance (Direct) | Alternative Credit Data |

We receive compensation from these partners