Best Reverse Mortgages

Based on In-Depth Reviews

- 200+Hours of research

- 40+Sources used

- 15Companies vetted

- 3Features reviewed

- 6Top

Picks

- A reverse mortgage converts home equity into cash

- You must be 62+, own a home and live in it to qualify

- You will still be required to pay property taxes and insurance

- Make sure to compare lenders to get the best rates and fees

How we analyzed the best Reverse Mortgage Companies

Our Top Picks: Reverse Mortgages Reviews

Fees, interest rates, and originating and closing costs for reverse mortgages vary from company to company. We favored lenders with lower rates and fees across the board.

Finance of America review

Diverse Reverse Mortgage Products

The HomeSafe product suite gives older homeowners more choices and flexibility than typical reverse mortgages. Designed to meet the needs of homeowners 55 and older1, it offers loans up to $4M2 with no mortgage insurance premiums (MIPs).

- HomeSafe Standard provides a lump sum payout, ideal for those seeking immediate access to home equity.

- For those who prefer flexibility, HomeSafe Select functions as a line of credit, allowing homeowners to draw funds as needed.

- HomeSafe Second is a second lien that allows homeowners to access a portion of their home equity while preserving their current first mortgage rate and terms.

Finance of America3 also offers the FHA-backed Home Equity Conversion Mortgage (HECM) for homeowners aged 62 and older. The HECM for Purchase (H4P) allows seniors to use a reverse mortgage to purchase a new home, combining homeownership with financial flexibility.

Commitment to Customer Service

Finance of America holds an A+ rating with the Better Business Bureau (BBB)4, reflecting its commitment to professionalism and ethical practices. Customers consistently praise Finance of America for their support and guidance provided throughout the reverse mortgage process. With a 92% customer satisfaction rate5, the company’s loan officers work closely with clients to ensure they fully understand their options and make informed decisions tailored to their financial needs.

Educational Resources and Online Tools

FinanceofAmerica.com is a user-friendly online experience designed to educate homeowners and those considering tapping their home equity.

The website includes a reverse mortgage calculator and educational articles on reverse mortgages, retirement planning, and product offerings. Additionally, the site’s inspiring customer stories show how real customers used their home equity to make the most of their retirement. These resources ensure homeowners have the information they need to make informed decisions.

A Trusted Provider

With over 20 years of experience in the reverse mortgage industry, Finance of America is an established, trusted lender. The company’s reputation is built on their commitment to transparency, customer education, and ethical practices. Consistently receiving high ratings across various review platforms, Finance of America’s dedication to customer satisfaction is evident in the positive feedback from clients who appreciate the personalized service and expert guidance throughout the reverse mortgage process.

This article is for informational purposes only and should not be considered financial advice. It is recommended to consult with a financial advisor to discuss specific situations before making any financial decisions.

-

For certain HomeSafe products only, excluding Massachusetts, New York, and Washington, where the minimum age is 60, and North Carolina and Texas where the minimum age is 62.

-

Loans up to $4 million available for certain HomeSafe products. The HomeSafe reverse mortgage is a proprietary product of Finance of America and is not affiliated with the Home Equity Conversion Mortgage (HECM) program. Not all HomeSafe products are available in every state. Please contact us for a complete list of availability.

-

Finance of America is a division of Finance of America Reverse LLC. The company does not do business as Finance of America in CA, NM, NY and OK.

-

Source: Better Business Bureau - Finance of America Reverse LLC – A+ Rating, Accredited since 5/13/2004.

-

Source: Consumer Affairs - Finance of America Reverse 4.6 / 5 Stars Consumer Affairs Average 4.6 / 5 - 92% Customer Satisfaction Rating as of 6/25/2024.

Longbridge Financial review

Best for Online Functionality

Longbridge Financial has by far the best online experience and tools among all the reverse mortgage lenders we reviewed. The company’s website is intuitive—easy to scan and to navigate. Its combination of extensive learning material and well-designed reverse mortgage calculators means almost any user will find something to interact with on the site.

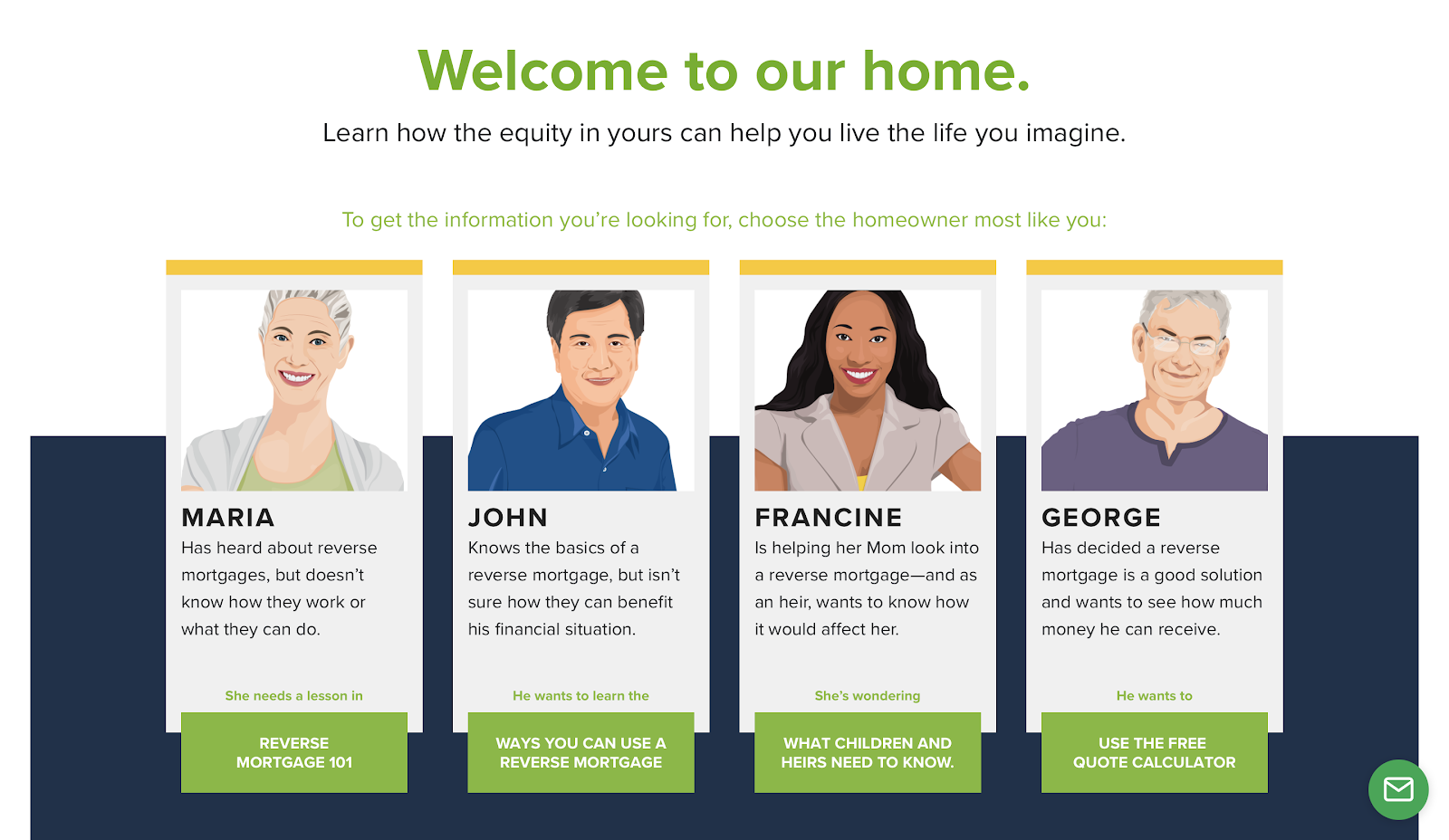

The website’s landing page makes it easy to immediately pinpoint the information that matters. There are four “profiles” to choose from; each one targets specific concerns and levels of knowledge about reverse mortgages, from none to extensive. Clicking on a profile redirects the user to information which can help that specific type of homeowner through the decision-making process. Consumers who have carefully researched reverse mortgages are just as likely to learn something new as those who barely know anything about the product.

The learning material on Longbridge’s website is segmented into three major categories: Reverse Mortgage 101, What to Expect, and Reverse Mortgage Products. This makes it easy for anybody who wants to fully explore the website by themselves to find what they are looking for. The information itself is quite thorough; it covers all the basics of reverse mortgages, but also some of the more intricate topics regarding these products. Additionally, the layout, typeface, and occasional use of video content make for an interactive and streamlined reading experience.

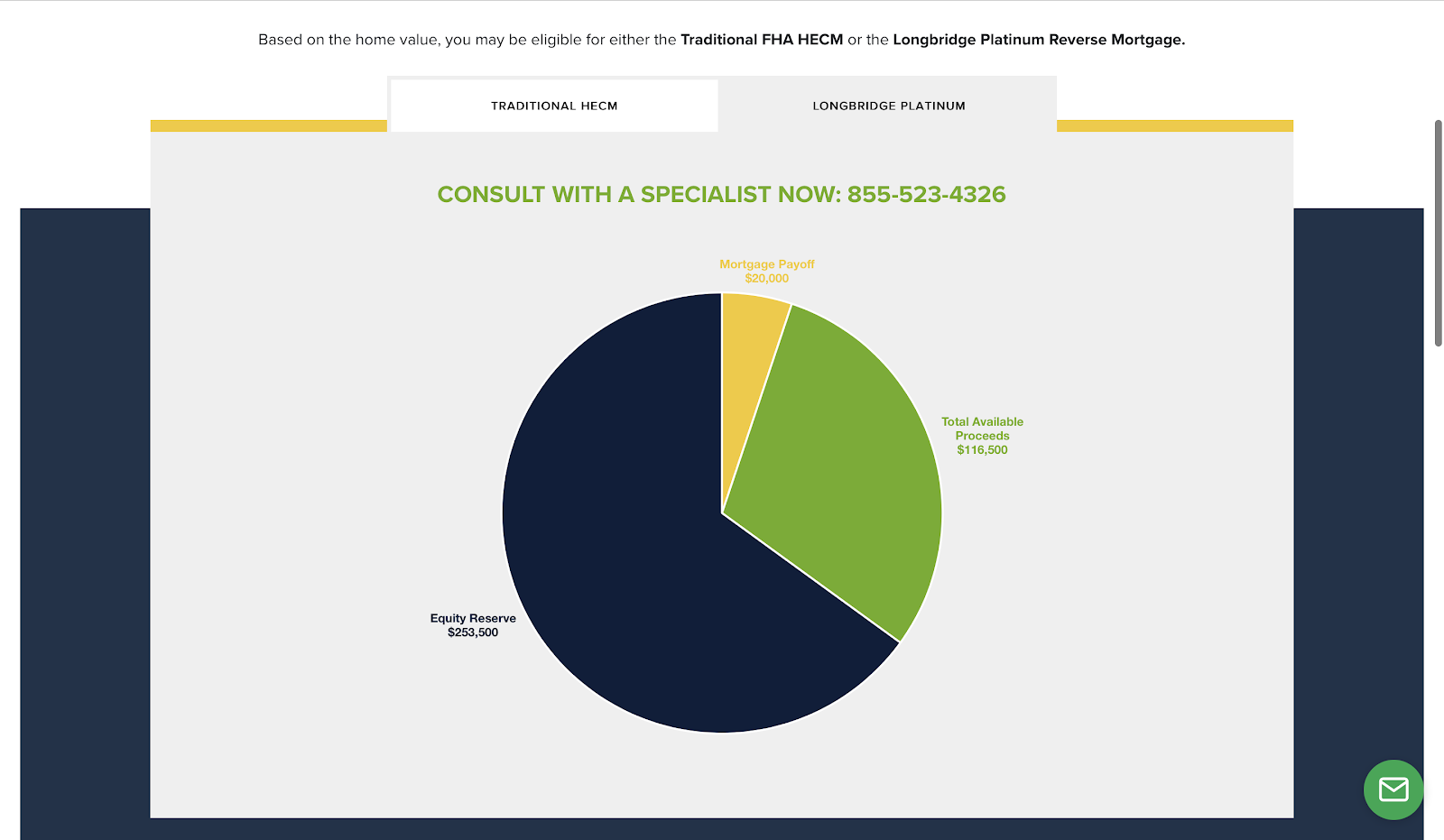

Longbridge features the most robust reverse mortgage calculator in the industry, with highly specific results thanks to the number of fields that must be filled out. Users must first input their estimated home value, but if they’re not sure, they can also use Zillow to get an estimate based on their address. After filling out the rest of the form, they are shown pie charts for both a traditional HECM and the Longbridge Platinum proprietary loan. They can also see what the projected growth would be if they chose to receive their reverse mortgage as a line of credit.

Outstanding Reputation

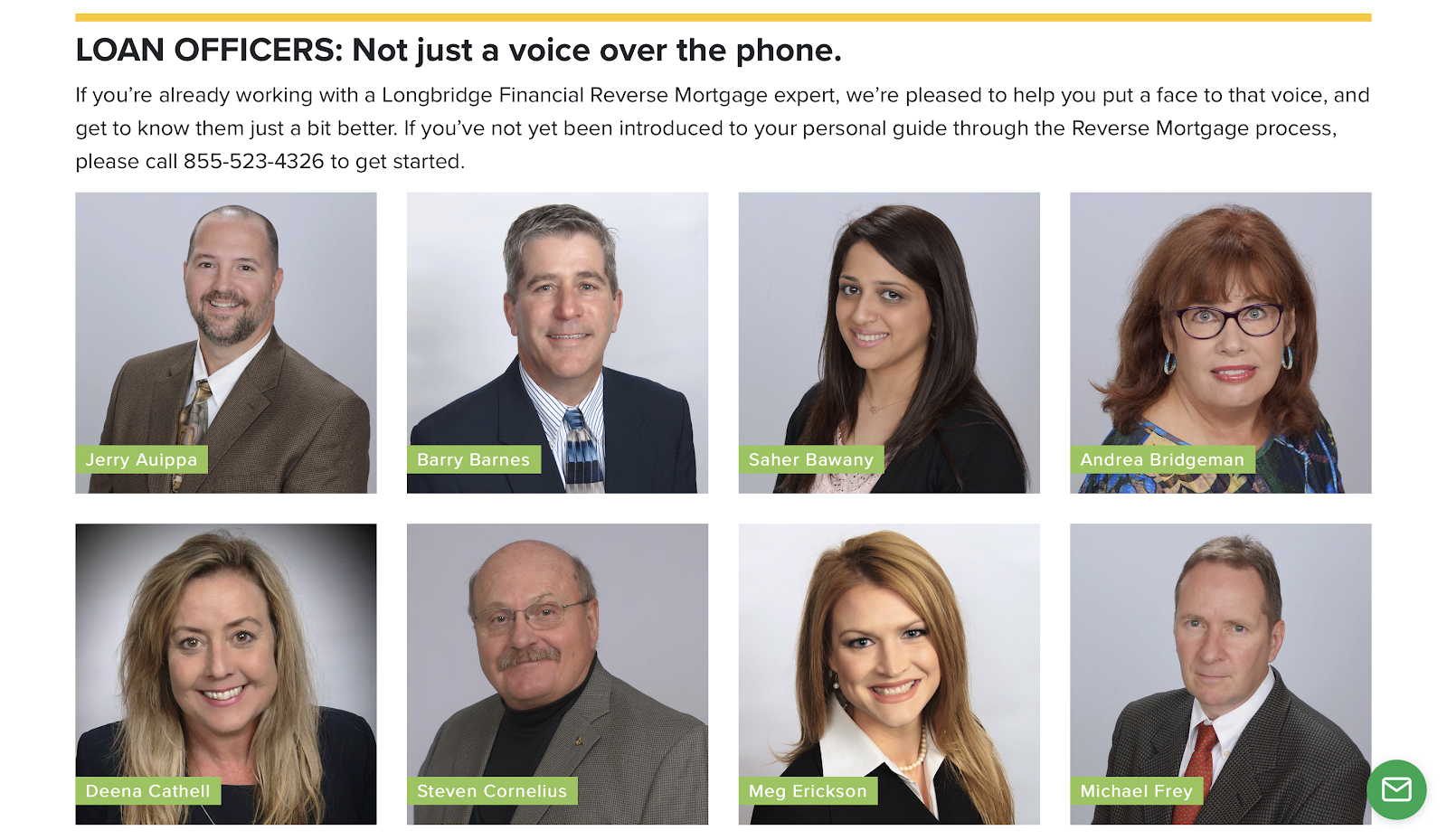

Longbridge has one of the strongest reputations in the entire reverse mortgage industry. The company is led by Christopher Mayer, an MIT PhD who also serves as a Paul Milstein Professor of Real Estate at Columbia Business School. Mayer was also Senior Vice Dean and Director of the Milstein Center and has held positions at the Wharton School and the Federal Reserve. All of the company’s loan officers, most of whom have worked for years or decades in the mortgage industry, are shown on the team page along with a short introduction and their NMLS agent code, which can be used to look up any regulatory actions that have been taken against them.

Longbridge is a member of the NRMLA and was approved as a Ginnie Mae issuer of HECM-mortgage backed securities (HMBS) in 2017. Alicia M. Munnell, one-time Assistant Secretary of the Treasury for Economic Policy, and who has been at the forefront of advocating for the reverse mortgage industry for decades, also gave the company its approval and even invested in it.

On the consumer side, Longbridge boasts excellent reviews on each third-party review aggregator it appears in. It’s accredited by the BBB and currently holds an A+ rating with the bureau. Additionally, it only has three complaints in the CFPB—two of which received a timely response—and a single regulatory action against it listed in the NMLS.

Unique Programs

In addition to the HECM and HECM for Purchase programs, Longbridge also offers its own proprietary loan called the Longbridge Platinum. As with other proprietary reverse mortgages, the loan is not backed by the FHA and features a loan amount maximum of $4,000,000. Under certain restrictions, the loan allows homes with a current solar panel lease, may qualify condos that haven’t been approved by the FHA, and is currently available in 17 states.

Finally, Longbridge also provides the “Gold Program,” a reverse mortgage program with lower fees and rates exclusive to those who meet certain additional requirements. In order to qualify, applicants must have a credit score of at least 660, using the MidFICO. Manufactured homes will not qualify for this program.