Best Whole Life Insurance

Based on In-Depth Reviews

- 220+Hours of research

- 20+Sources used

- 23Companies vetted

- 4Features reviewed options

- 7Top

Picks

- Whole Life is permanent life insurance with tax advantages.

- Policyholders can receive dividends and build cash value to use at their discretion.

- Whole life is generally more expensive than other types of life insurance.

- Premiums are consistent throughout the life of the policyholder.

How We Found the Best Whole Life Insurance Providers

Our Top Picks: Whole Life Insurance Reviews

In our life insurance review, we explained general differences between term and permanent life insurance. If you’re considering life insurance, your main concern is probably your family’s financial security. But what if you could get more out of your life insurance policy while you live?

Whole Life insurance does just that: enables the policyholder to use the policy beyond the death benefit. With a whole life insurance policy, cash value from the premium accumulates over time that can be used for anything you choose, like pay off debt, make a down payment on a home, invest, and more. In this review, you'll discover how your family can benefit from this type of policy as well as the best whole life insurance companies that cater to your specific needs.

State Farm review

Best for Multi-Policy Discounts

This insurance company may have caught your attention with its comedic “Jake from State Farm” commercial back in 2011, but State Farm has earned its consumers’ trust. Ranking Highest in Customer Satisfaction in J.D. Power’s Life Insurance Study for the fifth year in a row, State Farm is one of our top choices for whole life.

As one of the largest life insurers in the country, State Farm offers a wide range of policies and coverages, including term and universal life, and the option to convert term life into a permanent policy.

Whole life insurance can be a bit costly for the average middle-class household, so State Farm’s multi-policy discount stood out to us as a valuable perk. For policyholders who already have homeowners, renters, or life insurance with the company, they can save up to 17% when adding vehicle insurance. State Farm also offers to combine life insurance policies with disability income insurance and homeowners insurance as a bundle called Triangle of Protection.

Premium Payment Customization

One general concern about purchasing a whole life policy is factoring in premium payments into a monthly budget. State Farm caters to this, offering whole life policies with a one-time payment option as well as alternatives to pay up to age 100 or another set number of years.

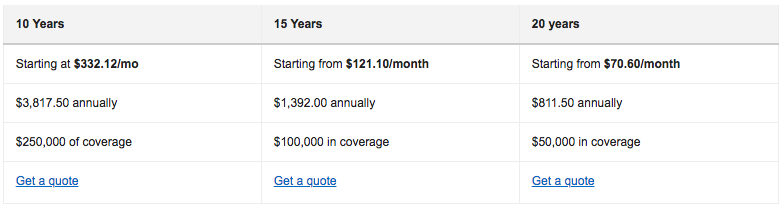

The option to pay for a set number of years, the Limited Pay Life option, enables policyholders to make premium payments for 10, 15, or 20 years for coverage amounts ranging from $50,000 to $250,000. State Farm also allows the flexibility of paying monthly, quarterly, semi-annually, or annually.

Screenshot of StateFarm.com's whole life policy options. September 18, 2019.

Those mainly interested in the death benefit coverage but who still want access to the whole life cash value component and the possibility of receiving dividends can opt for State Farm’s Final Expense Life Insurance. This policy guarantees a death benefit of $10,000 and still gives policyholders the option to pay their premiums monthly or annually.

Drawbacks

State Farm does not operate in Massachusetts, Washington, or New York. The company does, however, do a good job informing customers of this by stating it throughout its website in large print. State Farm may not offer their products nationwide, but its transparency, as well as the educational and helpful resources on its website—agent search, illustrated life insurance calculator, online quote, virtual assistant chat, educational blog—are what we believe helped them win their client's trust and earned them a J.D. Power customer satisfaction award.

Quotacy review

Best For Customer Resources

There are many insurance marketplaces out there, but Quotacy takes its customer service a step further. Launched in 2014, this insurance broker excels by offering a variety of educational resources including a comprehensive buyer’s guide, informative videos, terminology lists, FAQs, comparison diagrams, life insurance calculators, and articles.

Screenshot of Quotacy.com’s educational videos. September 18, 2019.

After the consumer is well-informed about the type of life insurance they’re considering, Quotacy allows them to request an online quote without requiring personal information. It’s rare for a marketplace or broker to provide rate quotes without asking for your personal information, which makes Quotacy stand out from the rest.

Company Match and Compare Options

Another benefit of using this marketplace is the availability of company reviews. As an independent life insurance broker, Quotacy provides unbiased information about each life insurance company in its network. The marketplace explains that its agents aren't paid by commissions and therefore have no reason to pressure consumers into purchasing a policy.

Each company review contains an overview, its list of financial ratings, comparison quotes, benefits and features, available riders, Quotacy’s likes and considerations about the company, and any fine print in the guidelines, exclusions, or disclosures. The information is well organized, informative, and easy to read. The side-by-side quote comparisons consist of the average cost of premiums for a man and woman, of ages ranging from 30 to 70.

Screenshot of Quotacy.com's company comparison chart. September 18, 2019.

Drawbacks

As helpful and convenient as Quotacy’s quote comparison chart is, it's only available for term life insurance, not whole life. Also, the company reviews primarily focus on their term life policies, not whole life ones. Customers can still receive quotes for whole life policies but must use the "request quote" tool to receive them. Quotacy does, however, provide a chart of the average monthly rates for whole life insurance for male vs. female at ages 30, 40, and 50.

Guardian Life review

Best For Chronic Illnesses

Guardian Life stood out to us in the whole life insurance arena by catering to people with chronic illnesses who may experience difficulty finding coverage for their health condition, particularly individuals with HIV.

Since health status and risk are key factors that determine one’s eligibility for coverage, it’s common for people with ailments and conditions to face challenges when shopping for life insurance, especially for permanent coverage like whole life insurance. With the Chronic Illness Rider, as well as the other riders available that cover terminal illness or disability, Guardian Life makes it possible for more individuals to qualify for coverage and protect their families.

Guardian Life’s guidelines for HIV policyholders are reasonable, including a required medical test for HIV and the individual being under the care of an HIV-specialized doctor. The company only excludes those with a history of intravenous drug use, substance abuse, and other similar factors. Guardian Life is transparent about the possibility of a higher premium for those who qualify, as it explains in the FAQs section.

Steady Dividend Payout

In addition to health status inclusion, Guardian Life is another company with a track record for financial stability. According to the Guardian Life Fact Sheet and annual report, the company has successfully paid out dividends annually since 1868. The company is also listed by J.D. Power as a Certified Customer Service Organization, having demonstrated high levels of customer satisfaction.

Screenshot of GuardianLife.com’s Fact Sheet PDF. September 18, 2019.

Drawbacks

As mentioned earlier, individuals living with HIV may receive a higher premium if they qualify for coverage. Also, after speaking with a customer service representative, we can clarify that HIV is categorized under "chronic illness rider," not its own designated rider. Guardian Life does not mention on its website other qualifying chronic illnesses and exclusions, so we encourage consumers to contact an agent directly.

Nationwide review

Best For Payment Flexibility

The last on our list is Nationwide, a mutual company that offers multiple forms of insurance, including life, homeowners, and auto, as well as investment, retirement, and business insurance solutions. It’s slogan and jingle “Nationwide is on your side” may ring a bell for millennials, but this renowned company has been offering insurance and financial services for over 85 years.

Nationwide’s approach to whole life insurance policies is different from that of other life insurance companies. With Nationwide’s YourLife whole life insurance (WL), consumers have two payment length options they can choose to tailor to their budget. The first is the WL 100, where payment on the fixed premium continues until the policyholder is 100 years of age. The second option is the 20-pay WL, where the premium stays fixed, but the policyholder can pay off the policy in its entirety after 20 years.

Diverse Policy Riders

Nationwide also offers multiple riders that help customize policies to continue coverage through life-changing events. For example, the Spouse and Children’s Term Insurance riders enable policyholders to cover their entire family under one life insurance policy, with the option to later convert the coverage into separate policies per individual.

Another rider, the Accelerated Death Benefit, allows you to receive a cash advance on the death benefit should you be diagnosed with a terminal illness. These and other riders offered by Nationwide are also available through other life insurance policies, including term life and universal life insurance, adding convenience in case the individual chooses to transition from term to permanent insurance.

Screenshot of Nationwide.com’s riders as optional add-ons. September 18, 2019.

Drawbacks

Nationwide is widely recognized for its auto insurance, a product the company markets much more than any other type of insurance through its commercials and on its website. That being said, the company still offers a lot more information regarding whole life insurance and resources in comparison to other companies. Website visitors can find Nationwide’s 5-minute guide to whole life insurance PDF as well as utilize its life insurance needs calculator, financial specialist locator, and read about the different rider options available.

Honorable Mentions

AIG Direct

AIG is one of the largest insurance companies in the U.S. and offers cost-effective policies with the option for no medical exam. These advantages are available through AIG’s Guaranteed Issue Whole Life Insurance, which differs from a basic whole life insurance policy. While the guaranteed issue whole life policy is slightly more affordable, it's only available to individuals between ages 50 and 85. Also, the death benefit payout has a $25,000 coverage limit, since this policy is designed to only help with final expenses. Regular whole life insurance is designed for larger benefit coverage, such as paying off debts, family daily living expenses, and children’s college funds. Many whole life insurance payouts, including all of our top chosen companies, extend beyond $100,000. For this reason, we list AIG as a runner-up.

PolicyGenius

Another honorable mention is PolicyGenius, an independent life insurance broker that helps consumers find, compare, and get matched to life insurance companies. PolicyGenius provides many resources and educational information for consumers about different forms of life insurance, including unbiased company reviews, instant online quotes, and side-by-side rate comparisons. PolicyGenius is very transparent with its readers, recommending against whole life insurance for most shoppers and, instead, encouraging term life insurance, which is the more affordable of the two. For that reason, we also list PolicyGenius as a runner-up.

More insight into our methodology

Life insurance can be as difficult to navigate as will and estate planning, yet as equally important. When we first began our research on life insurance, we learned the diversity of options available, as well as the wide spectrum of coverage offered. As we dug deeper into policy utilization, we realized that whole life insurance offered far more benefits than anticipated.

For consumers to fully grasp the concept of policy flexibility, we realized whole life insurance needed a review separate from our general life insurance review. To find the best whole life insurance companies, we took into account their availability, financial solidity, choice of benefits, and customer service.

Nationwide Availability

Many states have different laws and regulations that govern their insurance policies. If you and your family were to move out of state, you’d have to check beforehand to make sure the company you're looking into is licensed to sell insurance in your state. On these grounds, we chose to only include companies that are licensed to operate in the majority of or all 50 states.

Financial Stability

Whole Life insurance policies are designed to do just that: insure your whole life. With that said, you want to make sure your company of choice is in good financial standing and a reputation of paying out death claims. For this reason, we turned to three independent, major credit rating agencies: Standard & Poor’s (S&P), Moody’s, and A. M. Best. These agencies assign letter grades as a rating scale based on research, risk analysis, and credit assessments of companies and corporations. We chose companies that received above-average financial ratings from these three agencies.

Policy Benefits

In comparison to other types of life insurance, Whole Life insurance is the most expensive. If you’re planning to enter a lifelong contract with an insurance company, you’d want to get the best bang for your buck. From payment flexibility to special rider add-ons, our list of the best whole life insurance companies offer policyholders multiple benefits and options to make sure their policies are tailor-made.

Customer Satisfaction

Before settling on a company, consumers should know how well it serves its customers. Our goal was to choose companies that have above-average customer satisfaction ratings and an overall good reputation for handling claims. While the Better Business Bureau and on-page customer reviews are helpful, J.D. Power ratings and the NAIC Complaint Index both cater specifically to the performance of insurance companies.

J.D. Power is a credible marketing research company that conducts industry-wide, unbiased studies on insurance customer satisfaction, claims experience, and website evaluations. J.D. Power is independently-funded with a team of statisticians, methodologists, and industry analysts. It’s Power Circle Ratings rank companies on a 5-star scale based on customer feedback and responses to several survey factors. Our top companies rank with at least 3 out of 5 stars

The National Association of Insurance Commissioners (NAIC) is created and managed by the chief insurance regulators from the 50 states, Washington D.C., and the five U.S. territories. The organization helps protect the public interest through supervision and regulation for equitable treatment of insurance consumers. We used the NAIC Complaint Index, which compares a company’s performance to others within the same market and focused on companies with a complaint index equal to or below the national average.

Helpful information about Whole Life Insurance

If something were to happen to you tomorrow, what would be left behind for your family? As unfathomable as the thought may be, conversations like this can secure your loved ones’ future in your absence. With a life insurance policy, you can financially protect your family.

In the event the policyholder passes away, an insurance policy pays a tax-free, lump sum of money (also known as Death Benefit) to the designated beneficiaries. This Death Benefit, which can range from $20,000 to $100,000 or more, can be used however they wish.

If life insurance is an investment you’re considering for your family, it’s important to understand the different types of policies to choose one that best fits your needs.

If you’re young, without children, or only looking for coverage for a specific timeframe, then term life insurance might be the ideal choice. Term life insurance policies can cost a little as $20 per month, generally last no longer than 30 years, and payout the agreed death benefit to your beneficiaries if you pass away within that time frame. If you live longer than the term, and if you choose not to renew it beforehand, the policy will expire.

In contrast to term life, which is limited to a certain amount of years, there is a type of life insurance policy that is designed to last your entire life and will pay out the death benefit to your beneficiaries whenever you pass away. In addition to that, you may receive another form of benefits under this type of policy, even while you’re still living. If these advantages sound like a good investment for you and your family, Whole Life insurance may be an option for you.

What Is Whole Life Insurance?

Whole Life insurance is a type of permanent life insurance that includes an extra savings component known as the “cash value.” As long as you pay the premium, the policy has no expiration date and earns interest each year, accumulating cash value over time.

There are two other types of permanent life insurance, “variable” and “universal,” that also accrue cash, but their interest rates and cash value rely on market indexes and other investment components. The premium rate of whole life insurance remains fixed throughout your lifetime and the cash value operates like a savings account.

In comparison to term life insurance, which can be thought of as “renting” the death benefit, a whole life insurance policy is structured so that eventually, you own it. Once you finish paying the premiums, it’s still active. Also, since it’s guaranteed that your beneficiaries will make a claim someday, whole life insurance pays out the death benefit no matter what.

“If you have a temporary need, you’re better off with term. If you have someone depending on your income for support, a whole life policy would make a lot more sense. At the end of a term policy, you have no protection. But whole life doesn’t expire or decrease in value, and the premium will not increase.”

- Lynne McChristian Communications Consultant for the Insurance Information Institute

Finally, there is the option to include “riders” — features you can add on to customize the policy — that cover payment of your premium should life circumstances prevent you from doing so. A popular rider is the Waiver of Premium, which allows you to skip monthly premium payments if you become disabled and can no longer work. Other common riders include Chronic Illness and Long Term Care riders, both which supply additional income should you suffer from an illness or need care that would otherwise mean extra monthly bills. Be aware that riders will increase the cost of the premium, vary from company to company, and may require a medical exam to qualify.

Now that we’ve explained what whole life insurance is in a nutshell, let’s dive deeper into its benefits.

What Are the Benefits?

As previously mentioned, whole life insurance can provide additional income while you’re still living as well as a substantial lump sum for your beneficiaries. Remember, as long as you pay the premium, the policy is always active. Also, as opposed to other types of life insurance, the premium amount remains the same. Once the monthly payment is set, it does not fluctuate.

Cash Value

Another advantage of whole life insurance is how it builds cash value. Unlike other forms of permanent life insurance, which depend on the market and investments, a whole life insurance policy sets aside a “savings” portion that grows from a percentage of the premium. The cash value can also earn interest from the life insurance company, in which it grows significantly over time. Then, once mature, you can use the cash value however you like.

Dividends

Additionally, if your life insurance provider is a mutual company, there’s another perk to your policy. Depending on the financial stability of your life insurance company and how well it performs over the year, you may receive annual dividends that can be added to either the death benefit or cash value. Dividends are the amount of money returned to policyholders out of the insurance company’s profits. As a mutual company, the shares go back to the policyholder, instead of a stockholder. Keep in mind that dividends are not always guaranteed since the payout depends on the financial strength and stability of the company.

Tax-Deferred Growth

Imagine receiving an additional check each month in which taxes aren’t taken out before you receive it. This is exactly how the cash value grows — tax-deferred. Depending on how your policy is structured and how much you’ve paid toward it, you can withdraw the cash value tax-free and use it however you decide. The dividends you receive are typically tax-free as well if the amount is less than your total premium. Finally, like financial security, the death benefit paid to your beneficiaries is tax-free.

With a whole life insurance policy, you can have an additional stream of income that is tax-free and lasts a lifetime. We do recommend, however, that you receive expert advice from a tax advisor for insight on tax laws and making use of money from your policy.

Utilizing the Cash Benefits

An essential question to think about when deciding on whole life insurance is how you and your family plan to use the cash value and death benefit. What exactly can you use it for?

Simply put, you can use it for anything. Under a whole life insurance policy, the cash value is essentially your money, which you’re free to use however you see fit. Since this advantage is accessible while the policyholder is still living, there are plenty of ways one can use it:

The death benefit can then be used for remaining bills and expenses after your passing, such as funeral and burial costs, the beneficiaries’ daily living expenses, retirement for the surviving spouse, and college savings for the children.

While additional cash and several advantages come with the policy, there is one factor that plays a major role: the cost of premiums. Whole life insurance policies cost much more than term life policies. Let’s take a further look to learn the reason behind it.

The Breakdown of Policy Expenses

Since individuals are given a much longer timeframe to pay off their premiums when compared to term life insurance, the average person might be curious as to why whole life insurance policies are generally more expensive. The reality is, a lot more work is done on the insurance company’s part to ensure the policy lasts a lifetime, remains customizable, and is available in case of an untimely death. This involves several fees that don't apply to term life policies.

Below is a simple breakdown of some of the extra fees:

-

Administration Fees - the record-keeping and maintenance of the policy

-

Sales Charges - the compensation for sales expenses and local and state taxes, which is deducted from the premium payment before it's applied to the policy

-

Mortality Risk Charges - the insurance company’s safety net in case the policyholder doesn’t live to the assumed age

-

Cost of Insurance - the actual cost of having the insurance policy

Also, dividend payout relies on three main factors: financial strength, claims, and expenses. After the insurance company evaluates its financial health through investments (the managed finances), the annual claims (the number of death benefits paid out), and its total expenses of the year (management of its day-to-day operations), the company analyzes how much dividends it can payout. Extra policy fees also help ensure dividend analysis is performed properly and that the company strategically has all of its ducks in a row.

Is Whole Life Insurance Right for You?

So, now that we’ve covered the what, why, and how, it’s time to determine if this type of life insurance is the best option for you and your beneficiaries.

The first thing to consider is whether or not you can afford it. Where a whole life policy for a $100,000 death benefit can have a $5,000 per year, a term life policy for the same death benefit can cost about $250 per year. Expect to pay a lot more for whole life insurance than for term life insurance. If the benefits far outweigh the cost of the premium in your case, and if paying a few hundred dollars each month for the premium fits into your budget, whole life insurance might be more favorable.

Next, think about the beneficiaries for whom you’d want to leave money behind. If you don’t have a spouse or significant other, children, a family member who depends on you financially, or a business, consider what you plan to use the extra cash benefits on should you invest in a whole life insurance policy.

Dave Jelinek, a former insurance salesman in Wisconsin, shared with us why whole life insurance was one of his best investments:

“When buying life insurance, don’t think of it as a bill. It’s like putting money into a 401K. The difference is, the policy has a lot of flexibility.”

Jelinek explained that eventually, he no longer had to pay the premiums out of pocket. The dividends he received were enough to cover the payments for him. Having originally bought whole life policies for his two children as a savings plan, Jelinek realized it was super flexible. After 25 years, the cash value of those whole life policies accumulated to about $25,000, which his adult children could cash out or transfer to their policy.

As always, it’s beneficial to discuss your income, investment, and retirement plans with a financial advisor to receive expert insight on how whole life insurance can work in your favor.

What to Watch Out For

Compare the Cost and Coverage

As we stated before, whole life insurance premiums can be quite expensive in comparison to other forms of life insurance. If you choose whole life insurance, make sure you’re exhausting its benefits. If you’re only interested in whole life for the death benefit, you’re likely to find a term life insurance policy that offers the same coverage for a much cheaper premium.

Whole life insurance calculates premiums based on your actuarial risk at the time you purchase the policy. This includes an overage that will be invested to build cash value and provide compensation for the insurance agent who sold you the policy. In our interview with Lynne McChristian, the Communications Consultant of the Insurance Information Institute, we learned that medical exams are a rising trend among life insurance companies.

“Typically, the younger you are, the less costly insurance is going to be. We always recommend people to get insurance early. It’s based on your age, health habits, and characteristics. Life insurance policies do require a simplified medical exam if it’s an individual policy for a higher [death benefit] limit. The underwriting guidelines may be different from one company to another.”

When comparing how much you’re putting in, with how much you’re getting out of a whole life insurance policy, here’s how you can estimate the amount you need:

- Calculate at least 5x your annual gross income (general rule of thumb)

- Factor in funeral and burial expenses

- Include an emergency fund

- Account for any debts, including mortgage or rent payments

- Assess income replacement (should the surviving spouse be out of work)

- Consider education/college expenses per child

Remember, should making payments on the policy become a financial strain, you can elect to cancel or “surrender” the policy. Be aware, however, of surrender charges — the money deducted from the cash value should the policyholder terminate the policy. If you cancel your whole life insurance policy too early, you may walk away with nothing.

Dividends Aren’t Guaranteed

Dividends can be viewed as valuable assets to whole life policies, but they aren’t guaranteed. Their payout depends on the financial stability and performance of the company that year. Also, even if the company is consistent in paying them out, be aware that the dividend amount is also subject to change each year. When purchasing a whole life insurance policy, be mindful of the probability of receiving dividends.

Be Smart With Your Money

Since there are no restrictions on how to use the cash value of whole life insurance, someone without financial restraint can easily exhaust the money. If you plan to use the cash value as a loan, meaning borrowing against the policy, understand that your insurance company will charge interest on it once borrowed. If you choose not to pay it back, that value can be deducted from the death benefit.

Another factor to keep in mind is the time it takes cash value to build. Depending on the policy, most policyholders will not see a significant difference in the cash value until after several years, sometimes over twenty years. Borrowing early before the value matures may result in some tax fees. Policyholders should be careful not to borrow more than they’ve accumulated. Consulting a financial advisor before using your cash value can save you from making detrimental decisions that can affect your finances and insurance policy.

Research the Insurance Company Beforehand

While shopping around for different quotes, be mindful that a captive insurance agent will most likely be biased. Their job is to get your business for their company. Also, the company’s financial strength has a strong correlation with annual dividends and death benefit payout. By simply choosing the first company that offers the lowest premium, you may not get the option or coverage you need.

We spoke with Jason Dana, licensed life insurance agent and vice president of JRC Insurance Group, who provided us with tips on how to look for a reputable life insurance company.

“You’re going to want to look at the [company’s financial] ratings. A.M. Best does a good job at rating life insurance companies only. A+ superior is ideal, and higher. Also, work with an independent agent who quotes more than one carrier, so you can make sure you’re getting the best deal.”

Dana also highly suggested that anyone looking for whole life insurance should go with a mutual company. With mutual companies, the policyholders benefit from the shares of the company, resulting in dividend payout and other financial benefits.

FAQs about Whole Life Insurance

How early should I get whole life insurance?

I already have term life insurance. Can I convert it into a whole life policy?

Is whole life insurance necessary if I’m single with no children?

What factors can affect my insurance policy rate?

Do I need to take a medical exam for the policy?

Are there tax benefits with whole life insurance?

Our Whole Life Insurance Review Summed Up

| Company Name | Best for |

|---|---|

| State Farm Whole Life Insurance | Multi-Policy Discounts |

| MassMutual Whole Life Insurance | Dividend Payout |

| Quotacy Whole Life Insurance | Consumer Resources |

| Northwestern Mutual Whole Life Insurance | Retirement |

| New York Life Whole Life Insurance 2 | Policy Customization |

| Guardian Life Whole Life Insurance | Chronic Illness |

| Nationwide Whole Life Insurance | Payment Flexibility |