Best Bad Credit Loans

Based on In-Depth Reviews

- 200+Hours of research

- 50+Sources used

- 17Companies vetted

- 4Features reviewed

- 6Top

Picks

- A bad credit loan can help you consolidate debt

- Look for lenders that only carry out soft credit inquiries

- Compare a minimum of 3 offers to ensure the best rate

- Always verify the accuracy of your credit report before applying

How we analyzed the best Bad Credit Loans

Our Top Picks: Bad Credit Loans Reviews

Getting a personal loan with bad credit can be stressful. Can I get approved with a low credit score? Will lenders even consider my application? Fret not, we too know what it’s like to be burdened with mounting debt (hello student loans!) Life happens and sometimes you find yourself in an unfavorable financial situation with your credit at stake. We also know that not having any credit history, having a thin credit file or bankruptcy can hinder your chances of getting the most favorable offers.

The good news is that this is not a final verdict and you're not alone. Statistics from Northwestern Mutual’s 2018 Planning and Progress study say that “Americans are twice as likely to have accumulated $5,000-$25,000 in debt (33%) rather than personal savings (17%).” And last year, more than 50% of Americans cited debt reduction at the top of the list of their financial concerns.

Having bad credit is not the end of the world, but something to strive to move away from. In the following reviews, we break down the most bad-credit-friendly companies in the fintech sector and later on, how to get out of the vicious cycle of bad debt.

Additionally, we also encourage you to visit your local bank or neighborhood credit union to see what rates they offer. The benefit of going with a banking institution that you’ve worked with before is that they can view your paycheck and lending history upfront. Working with an in-person loan officer can also give you further guidance on how to improve your application to get more favorable rates. Read on to get a better feel of which company suits your borrowing needs.

This site does not include all companies or all available offers. Companies listed below are listed in alphabetical order.

Avant review

Best For Fast Funding

Referenced in some of the biggest names in financial journalism (Wall Street Journal, Fast Company, and Bloomberg), Avant is an emerging fintech company offering unsecured personal loans. Loan amounts start at $2,000 and can go up to $35,000 with APRs between 9.95%-35.99%. The loan terms range from 24-60 months and application, approval, and funding can take as little as 24 hours. This company is a better option for borrowers with fair to average credit (600 or above) and at least $20,000 in gross annual income.

There are some limitations to applying for a loan with Avant: they don’t lend in Iowa, Colorado and Virginia, charge a 4.75% administrative fee, don’t offer a co-signing option, and you may not use the loan to fund your business. As with other companies reviewed here, Avant offers soft credit inquiries that will not impact your credit score.

Screenshot of Avant’s application guidelines. September 9, 2019.

Transparency Of Rates And Fees

Avant doesn't charge online application fees or early repayment penalties. Their website is easy to navigate and has a clear-cut section on loan rates and terms where you can check offers by state and qualifications. The company’s website also has a comprehensive FAQ section on the application and funding process, and offer a mobile application (Android and iOS) to manage your loan payments and account.

LendingPoint review

Best For Debt Consolidation

Based out of Georgia, Lending Point is an alternative online lender offering unsecured personal installment loans for people with bad to average credit scores. Their underwriting is designed to look past your credit score and consider your employment status and debt to income ratio, among other factors. The range of loan amounts offered is from $2,000 to $25,000 with APRs in the 10.99%-35.99% range. The loan terms vary between 2-5 years. We must add that having an annual income of $25,000 or above is necessary to qualify but, on the upside, their minimum credit score requirement is 585.

Screenshot of LendingPoint’s alternative application factors. September 10, 2019.

Payment Flexibility

LendingPoint is a prime lender for those looking for payment flexibility; you can change your payment due dates 5 days before it’s due, they offer a bimonthly repayment option, and don't charge prepayment penalties or late payment fees. It must be said they don’t lend in West Virginia, and if you have good to excellent credit, this is not your best bet.

Additionally, applying online is simple and speedy, with funding in as little as 24 hours. You can apply via their website or phone and their customer service reps can be reached via phone or email at (888) 969-0959 and customerservice@lendingpoint.com respectively. As for complaints filed against them with the CFPB, they have a comparably low number, south of 60, all closed in a timely manner with an explanation by the company.

OneMain Financial review

Best For Secured Loans

One Main Financial is an industry pioneer for personal installment loans. They offer loans ranging from $1,500 to $20,000 with a fixed rate and payment depending on your current income, expenses, collateral (if available), loan size, loan term, and credit history. They perform a soft credit pull to see if you qualify, so it won’t impact your credit if you’re just shopping around. Their secured loans are available with term options of 24, 36, 48 or 60 months with APRs ranging from 18%-35.99%. If you end up taking a loan with them, they offer free access to your credit scores as a perk.

Screenshot of One Main Financial’s branch locations by state. September 9, 2019.

In-Person Assistance Available

Applying with One Main is a simple, automated process. You can apply directly on their website, over the phone, or in one of their brick-and-mortar branches. One Main has over 1,600 branches in 44 states, so we recommend checking if they're available in your state.

Strong points in their favor are that they offer a co-signer option, they don’t charge early prepayment penalties, funds can be approved and disbursed within 24 hours, and there is no minimum credit score or annual income requirement. We should also add their customer base raves about the treatment clients receive throughout the application, borrowing, and funding process. On the flip side, their maximum loan amount caps at $20,000 ($30,000 if it’s a car loan).

One Main Financial is definitely a company to consider if you have fair to poor credit and are looking to borrow funds for debt consolidation, unforeseen life events, recreation, auto loans, or home projects through a transparent and simple application process with the option to apply in person.

Upgrade review

Best For Unsecured Loans

Founded in 2016 by two ex-LendingClub executives, Upgrade is a relatively young fintech company specializing in personal loans, credit monitoring, and educational resources for consumers. Applicants must have a minimum annual income of $30,000 and a minimum of $800 in free cash flow a month to qualify. When we refer to free cash flow, we’re talking about how much available cash you have at the end of the month once you’ve paid off all your bills. To see if you qualify, Upgrade performs a soft credit pull that won’t impact your credit report.

Screenshot of Upgrade.com’s free credit monitoring tool guidelines. September 10, 2019.

Credit Building Tools and Austerity Plan Refinancing

This lender is a great option for people who have a minimum credit score of 620 and are looking for credit maintenance tools. Upgrade offers a complimentary credit monitoring feature with a VantageScore® 3.0 simulator with weekly score improvement suggestions.

Furthermore, they have an entire section of their website dedicated to "Credit Health Insights," where they break down all things credit-related. Besides this, if you unexpectedly lose your job, you can reduce your payments or modify the term length. They also allow joint applications and don’t charge a fee for prepaying your loan.

Cons of taking out a loan with Upgrade include origination fees and limited loan availability in Colorado, Connecticut, Iowa, Maryland, Vermont, and West Virginia. This is a good fit for borrowers with fair credit looking to pay off credit card debt, consolidate accounts, finance home improvements, or repay student loans. You can reach their customer service line at (855) 997-3100 Monday-Friday, 6 am-6 pm, Saturday and Sunday 6 am-5 pm PST and via email at support@upgrade.com.

Upstart review

Best For Young Professionals

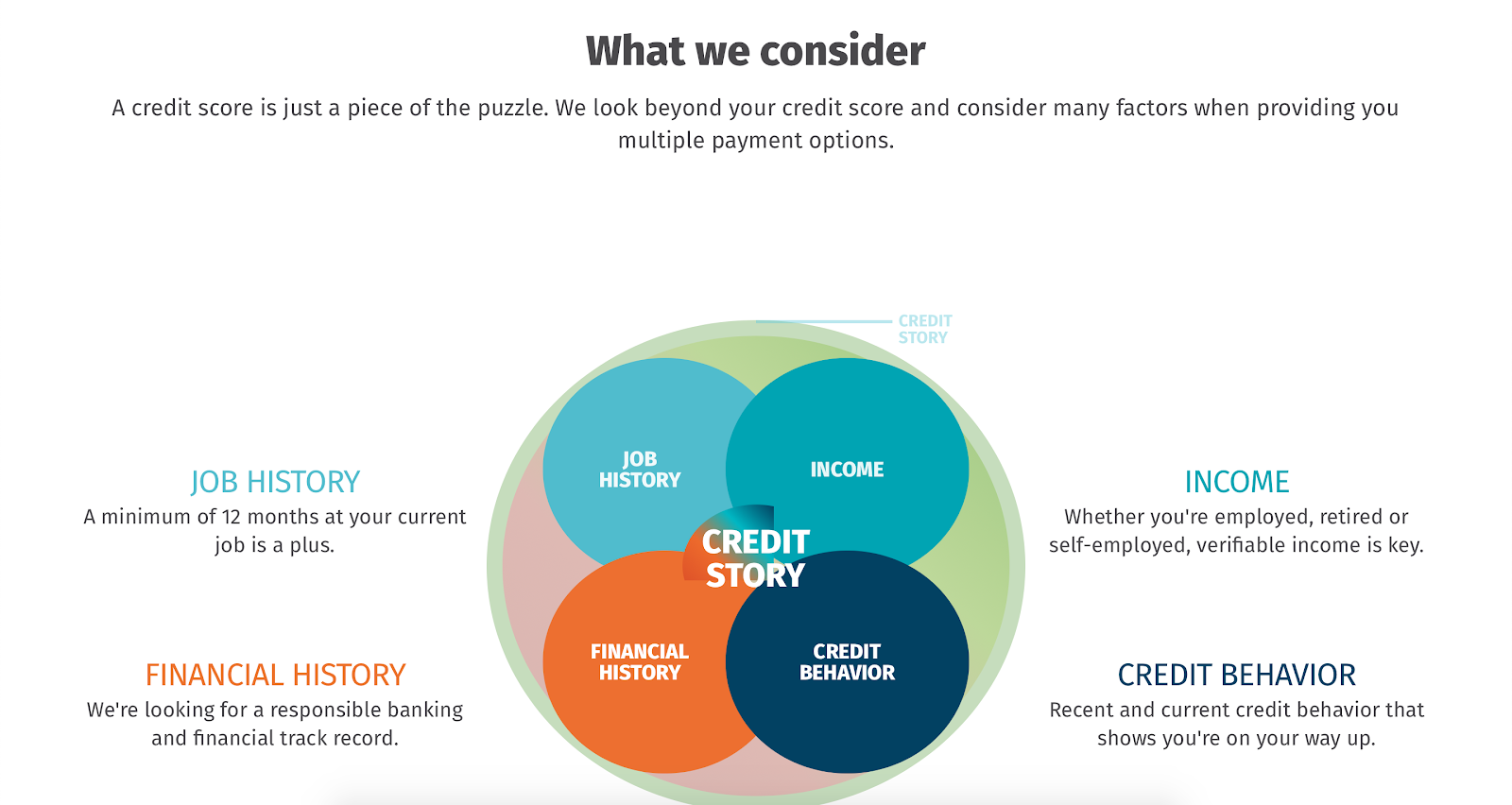

Upstart is an alternative online lender that uses your education, income, and professional experience as variables to help predict your creditworthiness. Founded by former Google employees, Upstart aims to use a mix of other factors besides traditional credit scoring criteria such as FICO score, credit reports, and income.

Beyond these, Upstart considers the college you attended, your GPA, standardized test scores, and work experience to create a statistical model of probable repayment. If you’re a young professional or a recent graduate, this is a reasonable alternative for an unsecured loan with a fixed rate.

Screenshot of Upstart’s alternative application form. September 9, 2019.

For Those with Short or Non-Existent Credit History

Upstart requires a minimum credit score of 620, but you don't need a minimum number of open credit lines or long-standing credit history in order to borrow. The online application is streamlined, so funds can be disbursed as fast as the next business day. This is a good option if you have little to no credit history, attended a reputable university, and have a well-paying job. Upstart APRs range from 9.57% to 29.99%, with a cap of $50,000 for loans with terms of 3 to 5 years.

Upstart's customer service can be reached by phone between 6 AM-5 PM PST and via email. As for reviews on the Consumer Financial Protection Bureau, they have a remarkably low number of resolved complaints. It's also worth mentioning that Upstart is available nationwide, except in Iowa and West Virginia.

More insight into our methodology

Prior to starting our search for the best bad credit lenders, we conducted 200+ hours of research, gathered information from approximately 50+ sources, and consulted experts in three different financial fields to get a deeper insight into what consumers with subpar credit need from a lender.

After a thorough investigation, we examined over 18 online lenders searching for the best in this category. We also did not discount local, traditional banks and credit unions, as these can be great for lower rates and personalized service, especially for people with lower credit scores.

We began this process with a list of 18 online lenders specializing in loans for borrowers with "bad credit." Our list included peer to peer lenders, balance sheet lenders, aggregators, marketplaces, and brick-and-mortars. We evaluated them based on the types of loans they offered, loan term lengths and amounts, APRs, minimum credit score requirements, overall company transparency, and customer service and reputation.

Finally, we narrowed the list down to 10 lenders, out of which 6 surpassed the industry standard and our criteria. Here are the factors that became the framework through which we evaluated the lenders on our list.

Loan Details

Bad credit loans are available for people who, for various life circumstances, have seen their credit scores plummet, have no credit, or have a thin credit history. There are several kinds of these loans available, but the ones we focus on in this review are secured and unsecured personal installment loans. There are other types of loans for people struggling with their credit scores: payday and car title loans, but we will discuss those further in the "What to Watch Out For" section.

In this review, we look at online lenders who consider alternative underwriting data such as educational background, current income, and professional trajectory, financial history, and credit behavior. We favored lenders who consider the whole financial history of individual applicants, accept co-signers as an option, and have accessible online applications.

On average, these companies have loan terms of 24-60 months and offer loan amounts in the range of $1,500- $50,000 with APRs between 9.95% and 35.99%. We made sure the lenders we reviewed didn't exceed the 36% APR marker, given that it’s capped at that almost nationwide.

Minimum Credit Score

When we set out on this bad credit loan research endeavor, we wanted to find out all we could on the industry standards. We started by looking at the minimum credit score requirements. Some lenders on this list have no minimum credit score requirements, but the lowest score starts at 580 and upwards. Further on in the "Helpful Information" section, we'll talk about familiarizing yourself with your credit report and so you can take measures to correct any errors in it and raise your credit score to get more competitive rates.

Additionally, the lenders we reviewed perform initial soft credit pulls to verify if you’re eligible for their loan products. These we favored because they don’t impact your credit report while you’re shopping around.

Transparency

The bad credit loans that these lenders offer can be used for a number of things: debt consolidation, medical emergencies, car expenses, credit card repayment, and other unforeseen life situations. These are not situations where you want to be overcharged for borrowing much-needed funds, therefore, we reviewed lenders based on the transparency of the rates and fees listed on their websites. Trustworthy lenders discuss their rates and fees upfront.

Customer Service

As part of our evaluation process, we took into account things like customer support availability, online customer reviews, and the reputation of each lender according to the Consumer Financial Protection Bureau. The CFPB assures lenders and financial institutions are treating consumers fairly by “regulating the offering and provision of consumer financial products,'' as stated on their webpage.

Helpful information about Bad Credit Loans

Credit Scores Today

According to the FTC's Bureau of Consumer Protection, a credit score is a system that creditors use to determine the risk they will be taking on by lending to you. The credit scoring system is used to determine what products will be available to you and on what terms, meaning a higher credit score will get you lower rates, while a lower score will get you higher rates. But shouldn’t you know this by now? You would think it’s common knowledge, but we don’t take classes on “How To Manage Your Credit Responsibly” in school (at least we didn’t). That's where this guide comes in handy. Here we’ll be breaking down all things credit score and credit report-related.

We interviewed Bruce McClary of the National Foundation for Credit Counseling to get insight into the industry from a credit expert. He states: “A credit score, according to the FICO scale, is based on a number of different elements, and the most significant element determining a person's credit score is how they’re paying their creditors and the history of those accounts. So if the person is making their payments on time, that reflects in the credit score that they have been making timely payments.

Those make the most significant difference. 35% of a FICO score is determined by this one factor. So if a person has damaged credit or if they have a low credit score it could be either because of a lack of history or because they have accounts that haven’t been maintained properly."

The other key factors that make up your credit score are: how much debt you owe (30%), the length of your credit history (15%), the number of new credit lines you open (10%), and the diversity of your credit lines (10%). Added together, these percentages make up the totality of your score. Poor credit is in the range of <580, fair credit scores are considered to be between 580 and 669, good scores range from 670-739, very good scores are between 740 and799, and excellent credit scores are upwards of 799.

McClary goes on to explain that " when someone wants to rehabilitate their credit score to get it to a healthier level, it depends on where they’re starting from. If they have a thin credit file and they don’t have much credit history, it’s all about building a healthy credit history, making sure that you’re opening accounts that are manageable and that can be maintained with timely payments so that you can start to raise your credit score.”

And according to our research, the average American has racked up a significant amount of debt, with the national average being $38,000 per person. Northwestern Mutual’s 2018 Study and Progress Report states that, on average, Americans spend 36% of their monthly income on debt repayment and 37% on discretionary expenses such as eating out, nightlife, clothing, and personal care.

Credit Reports

It is important to note that, contrary to popular belief, your credit report is not the same thing as your credit score. When you request your updated credit reports, they will not include your credit score, but instead, show you a snapshot of your credit history.

According to TransUnion, your report will show your account summary, your personal info including your SSN (make sure another person’s information is not linked to your account), credit inquiries (too many can impact your score negatively, and if you don’t recognize a lender it can be a sign of fraudulent activity), credit cards and revolving accounts, mortgage/ installment loans, and public records (which can include bankruptcies for up to 10 years).

Checking the accuracy of your credit report is important. Federal law states that consumers can get an annual credit report from each of the 3 major credit reporting agencies. You can use the FTC website to order your free credit report online or under the Fair Credit Reporting Act, request your credit scores from the three credit reporting agencies for a fee. Once you’ve purchased your score, you'll get instructions on how to improve it.

How Can I Rebuild My Credit?

As we mentioned previously, there are many reasons and life situations that lead to a bad credit standing. When we asked Dr. Kurt Schindler, Certified Financial Planner ® and tenured professor at the University of Puerto Rico, Río Piedras Campus about the healthiest alternatives for improving credit scores, he had some enlightening insight.

Dr. Schindler comments that “working on the credit is the easy part, but changing the habit is the much harder part. It’s like dieting, you really don’t want to, so when people ask me about credit building products I think the one I’m most comfortable with is a credit builder loan where you’re making payments to yourself. Or alternatively, where you have a cash collateral against a credit card, where if you don’t pay, the bank already has the funds. So essentially, you’re taking out a loan against your own money.”

We believe it’s important to highlight that changing your financial habits is key in the process of rebuilding your credit. Before you start this process, it’s important to request your three annual credit reports to rule out any mistakes or fraudulent activity. If your credit report does have mistakes, contact the credit agency. Thanks to the Fair Credit Reporting Act, credit agencies and information providers are responsible for correcting any mistakes on your report.

You can use this sample letter for credit agencies and this sample for information providers. These sample letters are from the FTC Consumer Information Resource. Afterward, you need to review all your loans with late payments or in delinquent status. If you have any loans with delinquent status, contact the collectors to arrange repayment. A bad credit loan won't do much help if you’re not taking care of the accounts that are weighing down your score.

After you’ve done this, your next steps should be paying your bills on time, keeping your balances low, not maxing out on your credit cards, not requesting too many loans or lines of credit that require hard credit pulls and avoiding unnecessary big purchases. If you’re considering a credit repair company, take a look at our most recent review on the subject.

Finally, set out to create a budget that takes into account your monthly income and expenses. Here’s a basic template from the FTC to get you started. As personal finance guru, Dave Ramsey says: “A budget is telling your money where to go instead of wondering where it went.”

National Foundation for Credit Counseling

As we searched the web for resources to guide consumers on their credit journeys, we discovered the NFCC. The National Foundation for Credit Counseling is the longest-running nonprofit helping people get on track to rebuild their credit histories. NFCC partners with different agencies that guide consumers with debt management plans, credit report reviews, homeownership counseling, reverse mortgage counseling, foreclosure prevention counseling, and bankruptcy counseling. You can schedule an appointment with one of their partners by calling (800) 388-2227 or directly on their webpage.

Types of Lenders

As we’ve previously explored in our Best Personal Loans review, there are pros and cons to working with different types of lenders. For the purpose of this bad credit loan review, we’ll focus on online lenders, banks, and credit unions. As we mentioned before, working with your local bank or credit union could work in your favor, as they're familiar with your income and payment history. They are also a great option for a low-rate credit-building loan, where you’re making payments to the total amount until you pay it off and get the funds. This is a great option for making positive marks on your credit score. The major con about working with a credit union is that you must be a member and have payment history to apply.

The benefits of working with your local bank are that they are also familiar with your credit history and account details. Banks are also more strictly regulated than online lenders, which can result in lower interest rates and fees. Conversely, working with an online lender can prove to be much easier and has become an increasingly popular option for borrowers. The cons of working with an online lender are that, although they have faster funding times, you might not get the personalized treatment you'd receive at a brick-and-mortar branch and you might get higher rates.

What To Watch Out For When Applying For A Bad Credit Loan

Predatory Lending and Scams

In the lending world, the two boogie-men of predatory loans are payday loans and car title loans. Demographics with bad credit or no credit can be easy targets, as it's incredibly easy to qualify for one of these loans.

“How can I avoid the pitfalls of predatory lending?” you may ask yourself. Let’s start with this: before working with a lender, make sure they are registered with the Federal Trade Commission (ftc.gov) and with the Consumer Financial Protection Bureau (consumerfinance.gov). The FTC and the Consumer Finance Bureau are great resources to check if the lending company is operating up to par with industry standards and regulations.

You want to make sure the lender you're working with is legitimate, trusted by consumers, and has a good industry reputation for having responsible lending practices. As always, shop around for offers with lenders who perform soft credit pulls, compare offers to get the most favorable rates, and make sure you read the fine print before signing any contract. Read on to save yourself the headache of a vicious cycle of debt.

Payday Loans

Also known as guaranteed loans, meaning you are guaranteed to receive the loan, payday loans are the most popular type of predatory loan for people with bad credit history, little to no credit history, or a bankruptcy. They range from $50- $1,000, depending on the state. A basic rule of thumb is that no legitimate lender will say you'll be guaranteed a loan without first verifying your credit history and credentials.

Payday loans are one of the most expensive loans on the market due to their sky-high rates and fees, which can go up to 400% or higher in some states. Yikes. According to the Federal Trade Commission, obvious tell-tale signs that a lender is making you a “too good to be true” offer are lenders that:

-

Are not interested in your credit history

-

Charge fees that are difficult to find on their websites

-

Demand a fee upfront before you see any money in your bank account

-

Make you an offer over the phone and ask for payments upfront

-

Are not licensed to operate in your state

-

Have a copy-cat name of a legitimate company (more on this later)

-

Ask you to wire money or to pay an individual

Scam artists and predatory lenders will work slyly to appear like legitimate lenders in the eyes of consumers. That's why it is of utmost importance to always do your research prior to taking out a guaranteed loan. And if you do, make sure you have the funds to pay it back immediately. We honestly advise exhausting all other options like borrowing money from friends and family. It will save you a significant amount of money in the long run.

Car Title Loans

These can be another type of "get cash quick, no proof of income required" predatory loan. The FTC advises against taking out a car title loan because you stand to lose one of your most valuable possessions and means of transportation. These short term loans are available for anything between $100 and $5,500, but some lenders may offer up to $10,000.

Car title loans can be accessed online or in person, have a repayment period of 2-4 weeks, and can have interest rates in the 3 digit range. It works like this: once you get the money in your bank account, the lender gets your car title. Once you pay off the loan, you get your title back. Be aware that these loans can get ridiculously expensive, with APRs in the hundreds and added charges such as processing fees, document fees, loan origination fees, title charges, and lien fees.

We got to talking with seasoned financial expert Dr. Kurt Schindler on his experience with predatory lending practices. “In my personal finance class I have my students go in and get the information for a title loan, a pawn shop, and a furniture rental store so they can get the experience of working with what I call the 'shadow banking system,' I need them to see the consequences of not managing credit carefully.”

He goes on to talk about what the FTC Consumer Bureau calls the “rollover.” This happens when a consumer who has taken out a title loan can’t pay it back in full, the lender offers to “rollover” the amount owed, creating added fees and interest to the original amount that was owed. This initiates a seemingly never-ending cycle of spiraling debt. He goes on to reiterate that “no one is teaching the consumer to be careful about the ease of it or that will be directly related to the problems that getting into too much debt entails.”

As stated by our extensive research, it’s prudent to say these loans should be avoided at all costs. Their interest rates can go up to exorbitant amounts and the chances of getting stuck in a toxic debt cycle are just too high.

According to Bruce MacCleary of the National Foundation For Credit Counseling, the latter are the most toxic forms of predatory lending. He adds that “the interest rates in some cases are outrageous, the terms and other fees associated with them can be very high, and there’s a lot of risk to the borrower in those situations. I would say it pays to take a few extra minutes to shop around and look for an alternative to a payday loan or a title loan and to find those in that space that are lending responsibly.

If you’re considering peer to peer lenders or some of the fintechs I would tell people to exercise caution. There are a lot of new lenders that are emerging in that space and it pays to take the extra time to investigate, check them out, and make sure that you’re comfortable doing business with them.”

As we discussed before in the payday loans section, another precautionary measure to take when going online for a bad credit loan, or any online loan for that matter, is being diligent in making sure the company name is spelled correctly in the URL bar.

Former FBI agent Lee Walters warns us of a predatory lending practice where predators will tweak an actual online lender’s web domain so that you basically can’t tell the difference between the legitimate one and the forged domain.

Walters’ goes on to say that “with the online lenders, you have to make sure you’re at the right site because some of these scammers will buy a domain that’s very close to what the actual domain is, and if you accidentally type in one letter wrong it can take you to a site that looks very much like what you’re trying to get to. You have to make sure you’re going to the right domain.”

This is important to keep in mind while shopping around for a loan in general. Scam artists will go through the trouble of forging websites, references, and paperwork to pass off as reputable banks and organizations, according to the FTC.

FAQs about Bad Credit Loans

Why does bad credit affect my loan options?

A collection agency has contacted me about an old account. What are my rights?

Does checking my credit hurt my credit score?

Our Bad Credit Loans Review Summed Up

| Company Name | Best for |

|---|---|

| OneMain Financial Bad Credit Loans | Secured Loans |

| LendingTree Bad Credit Loans | Poor Credit |

| Avant Bad Credit Loans | Fast Funding |

| Upstart Bad Credit Loans | Young Professionals |

| LendingPoint Bad Credit Loans | Debt Consolidation |

| Upgrade Bad Credit Loans | Unsecured Loans |