Wondering How To Find The Best Annuity For You?

Take our quiz to explore options tailored to your needs, including fixed, variable, or immediate annuities!

An annuity is a popular choice for retirement planning and long-term financial stability. Explore top annuities with fixed or variable rates, guided by experts to help you plan confidently.

Take our quiz to explore options tailored to your needs, including fixed, variable, or immediate annuities!

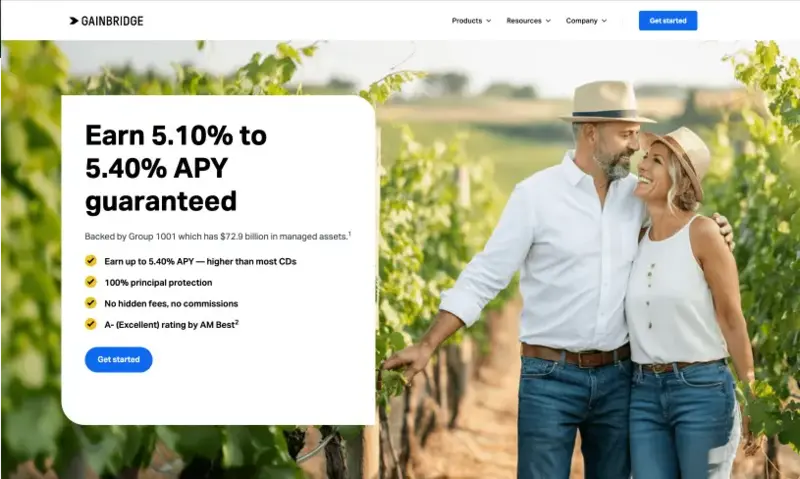

The FastBreak™ annuity, offered by Gainbridge, is a non-tax-deferred savings product with a guaranteed annual percentage yield (APY) up to 5.40%.¹ It is available in terms ranging from three to ten years and requires a minimum investment of $1,000.

Unlike tax-deferred annuities, FastBreak™ requires you to pay income tax on the gains credited to your account each year. While this means you don't receive the tax-deferred growth common with other annuities, it offers the advantage of flexibility. You can access your funds before age 59 ½ without incurring early withdrawal penalties, which is typically not an option with tax-deferred products.

According to Gainbridge, the FastBreak™ annuity is ideal for individuals focused on medium to long-term savings goals who want the flexibility to access their money if needed, before reaching retirement age. With its competitive APY and penalty-free early withdrawal feature, it’s a good fit for those seeking steady growth with financial flexibility.

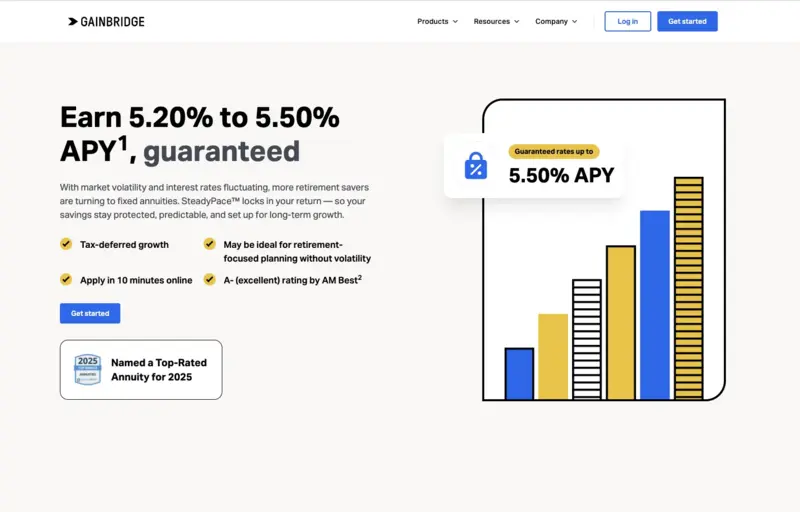

The Gainbridge® SteadyPace™ annuity is a tax-deferred savings option offering a competitive 5.50% APY and flexible term lengths ranging from three to ten years. With a minimum deposit requirement of $1,000, this annuity is accessible to a wide range of investors. Earnings grow tax-deferred, allowing potential tax savings, and you can withdraw up to 10% of your account value annually without penalty, starting in the first contract year.

Upon maturity, you have the flexibility to receive your funds as a lump sum, opt for regular payments over five to ten years, or renew your contract for continued growth under the prevailing terms. However, withdrawals before age 59½ may incur a 10% federal tax penalty on earnings in addition to ordinary income taxes.

The Gainbridge® SteadyPace™ annuity is ideal for individuals seeking secure, tax-deferred growth with guaranteed returns. It suits those with medium- to long-term savings goals, including pre-retirees and retirees who value flexibility, predictable income, and low-risk investment options.

Partner Disclaimers & Disclosures:

Gainbridge® FastBreak™ and SteadyPace™ Annuities:

¹ Annuity rates are subject to change at any time, and the rate mentioned may no longer be current. Current rate as of 09/15/2025 for a 5-10 year investment term. Rates subject to change.

² Withdrawals made prior to age 59 ½ are subject to an IRS early withdrawal tax penalty.

Please visit Gainbridge.io for current rates, full product disclosures, and other important information. Products and/or features may not be available in all states. All guarantees based on the financial strength and claims paying ability of the issuing insurance company.

Withdrawals above the 10 percent free withdrawal amount are subject to a withdrawal charge and market value adjustment and if under age 59 ½ may be subject to an IRS early withdrawal tax penalty (FastBreak™ is not subject to this penalty). FastBreak™ and SteadyPace™ annuities are issued by Gainbridge Life Insurance Company in Zionsville, Indiana.

FastBreak™ is not a tax-deferred annuity; instead you are taxed annually on earned interest.