Best Mortgage Rates

Based on In-Depth Reviews

- 200+Hours of research

- 100+Sources used

- 40Companies vetted

- 4Features reviewed

- 9Top

Picks

- July 2020's rate drop has lowered rates for 15-year fixed mortgages to 2.73%

- Mortgage lenders consider many factors for interest rates

- Government-backed options are available at lower rates

- Request a detailed breakdown of all fees and closing costs

How we analyzed the best Mortgage Rates

Mortgage Calculator

Always shop around!

Over the course of our research, the importance of comparison shopping quickly emerged. All the people we interviewed, from financial experts to homebuyers, agreed that one of the most crucial steps a consumer should take when looking into buying a home is doing their research. This can be especially confusing with mortgages and other complex financial products—and it can also take a lot of time. The cost of a mortgage involves a number of different factors, including more than just rates, fees, and points. Yet according to the 2018 National Housing Survey, around one-third of homebuyers don't shop around, preferring to rely on real estate agents and friends.

As part of efforts to mitigate the economic consequences of the Covid-19 pandemic, mortgage rates are seeing historic lows—as of April 2, 2020, primary mortgage rates now average 3.34%, thanks to the Federal Reserve's half a percentage point rate slash in March. This is the largest one-time cut since 2008's housing market crisis, bringing rates down to their lowest level in three years. This makes it a uniquely well-suited time for first-time buyers to consider purchasing a new house, since lower rates mean you can afford more home. Bear in mind, however, that the coronavirus pandemic will likely also increase the probability of unexpected complications arising, so make sure to have contingency plans built in for situations such as closing date delays or restrictions on movement.

Our Top Picks: Mortgage Rates Reviews

New American Funding review

Best for Non-Qualified Mortgages

A non-qualified mortgage refers to loans that don’t comply with the Consumer Finance Protection Bureau’s (CFPB) rules on what constitutes a high-risk loan. While this may seem indicative of dangerous practices, it can also be used the way New American Funding does--to offer mortgage loans that use alternate methods of income verification to qualify its borrowers, in the form of its Self-Employed mortgage and Non-QM loan.

Screenshot from newamericanfunding.com. Taken July 3, 2019.

New American Funding also offers Interest-Only mortgages--a loan usually offered to high-income borrowers, which only makes interest payments for a fixed term between five and ten years. This means the loan balance doesn’t decrease, and payments towards the principal must be met once the interest-only period is done.

Finally, the lender has the I Can mortgage, which allows borrowers to choose their own mortgage term, provided it’s between eight and 30 years, and they have a minimum credit score of 620.

Qualifying

To qualify for a non-qualified 1-year tax return mortgage program with New American Funding, borrowers must provide proof of employment for two years, personal tax returns for the past year (including schedules and attachments), and business tax returns for the same period.

Another option is the bank statement program, which requires personal or business statements going back 6-12 months, 100% of eligible deposits from both personal and business accounts, and finally, profit and loss statements for the last 12 months, or previous year, or year to date.

Additional Resources

One of the things we liked about New American Funding, besides its inclusive options, is its comprehensive educational resources. While this is always important, it’s especially so when it comes to non-standard debt products consumers may not be familiar with.

Screenshot from newamericanfunding.com. Taken July 3, 2019.

Not only does the company provide several calculators (mortgage, affordability, and refinance), but it also has a glossary of terms, and informative videos and articles. Lastly, we were particularly impressed by its large array of checklists available for download, including ones for budgeting, home loans, moving, and more.

Screenshot from newamericanfunding.com. Taken July 3, 2019.

AmeriSave review

AmeriSave Overview

AmeriSave has been in business for 17 years and is licensed in 49 states. The company is a direct lender and has funded more than $55 billion in loans to date. AmeriSave is highly rated by the Better Business Bureau and consumer reviewers on Trustpilot.

Fast Pre-Qualification and Detailed Quotes

The AmeriSave website makes it very easy to pre-qualify for a loan. You'll answer some basic questions to verify your identity and the property you're interested in, define your down payment intentions, and whether you might be eligible for government-backed loan programs. Interestingly, once you do, the site will provide you with its estimate of your current credit score. That's something you probably should know before you start shopping for a mortgage, but if you haven't downloaded your credit report, AmeriSave gives you an important bit of information that will help you investigate other loan options, too. You will need to provide your phone number to receive a quote and agree to receive marketing messages from the company, but you can opt out of marketing messages thereafter. The entire process takes about three minutes. When we tested the system—both for a first mortgage and refinancing—AmeriSave returned a rather astonishing range of mortgage offers based on the data we provided.

Amerisave also offers a 90-day certified Lock & Shop interest rate that protects you from rate hikes while you’re shopping for a house. The locked rate does not require a signed purchase contract, which gives you more flexibility.

Screenshot from AmeriSave.com May 2021

Wide Range of Choices

When we requested a mortgage quote, we received over 30 loan options to consider. In our test case, all of the offers were for fixed mortgages with terms ranging from 10 to 30 years. However, AmeriSave states on its website that variable-rate loans are also available. Depending on your circumstances and credit profile you may be able to choose either a 5/1, 7/1, or 10/1 adjustable rate mortgage. "Short-timers"—homebuyers who intend to stay in their homes for just a few years—can often take advantage of the lower interest rates and payments variable-rate loans typically offer. You can contact the company by phone if the choices you are offered don't suit your needs, of course.

In addition to conventional mortgages, AmeriSave also offers qualified homebuyers VA, USDA, and FHA mortgages. These loans typically have less stringent down payment requirements—sometimes as low as 0%. Government-backed loan programs are often available to homebuyers with less-than-ideal credit histories, as well.

But it wasn't just the number of loan options AmeriSave served up that impressed us. The quotes provided were detailed and included points or credits in addition to specific rates. These details empower customers to compare actual loan costs more accurately and see how they can lower their monthly payments and overall loan costs by changing the loan term they opt for. Moreover, AmeriSave presents options in a well-organized, graphically inviting fashion. Comparing options was a simple, pleasant experience.

Certified Approval Letter

If you decide you want to take advantage of one of the loan options AmieriSave presents, you can go ahead and request a Certified Approval Letter. If you have all the necessary documents to complete your application, you may receive this letter in just a few hours. AmeriSave also stands behind its approvals. Once you are pre-approved, if you are unable to close on your loan, AmeriSave promises to pay you $1,500 if your loan doesn’t close. Restrictions apply but be sure to ask an AmeriSave representative if you qualify for its Certified Closing Promise.

Customer Experience

AmeriSave streamlines the loan shopping and application experience. You can complete the process entirely online. That's not unusual among online lenders. However, many customers are likely to appreciate the transparency AmeriSave provides along the way. The company also provides a variety of helpful resources for homebuyers, including payment and affordability calculators, simple-to-understand explanations of loan types, a well-organized FAQ section, and a large library of helpful articles on subjects ranging from how to improve your credit to how to find the perfect starter home.

Screenshot from AmeriSave.com May 2021

AmeriSave Summed Up

AmeriSave is a terrific first stop for homebuyers who want to compare a wide range of realistic mortgage offers quickly and easily. The company stands out for its transparency, detailed offers, and comprehensive educational and support materials, as well.

Quicken Loans review

Best Overall

Since Quicken Loans’ move to becoming an online platform in 2000, it’s quickly come to dominate the mortgage industry for tech-friendly borrowers. Quicken is the second-largest mortgage originator in America by volume. That size translates into expertise across a wide swath of the mortgage market.

Quicken is a non-depository lender, so their own capital isn’t built from deposits by consumers. In practice, this means that they sell their loans to investors, the largest of which are Fannie Mae and Freddie Mac, both government-sponsored enterprises.

Screenshot from Quickenloans.com, May 2021.

A Home Buyer’s Guide

One of the things we most liked about Quicken was its guide, which offers a step-by-step explanation of the mortgage process. We feel this is especially useful for first-time home buyers, since a common thread among the consumers we interviewed in that situation was that there were still things they hadn’t understood about the process. And no wonder! It’s complicated--which is why Quicken’s clear, concise explanations and tips sections are particularly helpful.

We also found their various calculators helpful for getting a better ballpark idea of home purchase budgeting. Quicken has a calculator for mortgages, affordability, refinance, and amortization--and these are all available via the company’s calculator app, downloadable for iOS and Android.

Screenshot from Quickenloans.com, May 2021.

Customer Experience

Despite being an online lender, Quicken Loans still makes sure to offer its customers the ability to speak to one of their 3,000+ mortgage bankers, should they so prefer. Though borrowers can apply online, they can also contact the company directly over the phone or via chat (after answering a few key questions regarding geographic location, loan purpose, and phone number).

It’s also worth noting here that since Quicken services 99% of its mortgages, the lender’s customer service continues throughout, rather than being parcelled off to another company.

As part of their continuous drive to ease the mortgage process, Quicken Loans has developed an eClosing network, a mortgage closing with a digital note. It can be done one of three ways: an in-person hybrid eClosing, an in-person electronic notarization (IPEN), or a remote online notarization (RON).

Hybrid eClosing is currently available for mortgage refinancing in all 50 states, though IPEN and RON are still being phased in. However, as more states adopt the technology, the growing network will allow any Quicken Loans mortgage to can take advantage of the eClosing option.

On March 30, 2020, Quicken addressed how the coronavirus pandemic might affect the mortgage process in some areas. It stated:

"Even though shelter-in-place orders are in effect in many areas of the country, the mortgage process can still continue. Appraisers, closing agents and other people who need to enter your home can still do so under the shelter-in-place order. In some cases, we even have alternative ways to complete these parts of the process that don’t require entering the home.

We’ve made a slight adjustment to our rate lock process to accommodate shelter-in-place orders. Under normal circumstances, you’d lock your rate before underwriting begins. In areas where shelter-in-place orders are in effect, we can’t offer long rate locks because everything is changing so rapidly. If you’re in one of these areas, you’ll simply lock your rate closer to closing day."

Rates and Mortgages

Though we cannot emphasize enough that your specific mortgage rates will depend on your particular situation, Quicken Loans does have a page displaying its current mortgage rates, updated daily.

Screenshot from Quickenloans.com, May 2021.

The company offers a full range of non-bank mortgage products, including fixed- and adjustable-rate home loans, refinancing options, jumbo loans, and government-backed loans (FHA and VA). It also features YOURgage®, a conventional, fixed-rate loan in which borrowers can choose the length (also known as the term) of the loan, anywhere between eight and 30 years for loan amounts up to $484,350. This allows consumers to fully tailor their mortgage to their needs and budget.

Veterans United review

Best for VA Loans

As the name itself implies, Veteran’s United specializes in VA loans--indeed, it’s the largest originator of these types of loans in the United States. With VA loans as the sole focus of their business, Veterans United provides customer service and guidance tailored to this community, with 24/7 support and 23 physical branches in 18 states (often near military bases). With an advisory board made up of former military men and women, the company is ingrained with its borrowers’ military culture.

Customer Experience

Screenshot from Veteransunited.com, May 2021

The experience for Veteran United’s customers begins on the website, a helpful resource for easy-to-understand explanations of how the VA loan program works, mortgage terminology, and solid advice for homeowners. Because of their familiarity with all aspects of the VA loan program, Veterans United’s over 2,400 employees are experts in not only determining eligibility for the applicants, but in helping its customers secure a loan with the lowest expenses and fees.

In addition to articles and videos, Veterans United offers VA-specific calculators to help applicants prepare and budget for their home purchase. These online tools offer borrowers the ability to calculate monthly loan payments, how much home they can afford, and the loan limit specific to the county where the home is located.

Screenshot from Veteransunited.com, May 2021

Types of loans and how to qualify

Veterans United offers conventional loans, as well as FHA and USDA loans. Where the lender shines is in its requirements. The VA loan program typically strives to make it easier for servicemembers to qualify, understanding that this community faces particular challenges that may make it harder for them to qualify for typical credit and down payment minimums. This is why residual income is considered, aside from just the debt-to-income ratio--this means that underwriters also look at how much money is left at the end of the month once major debt is paid (but not things like food or your internet bill).

To be eligible for a loan with Veterans United, borrowers must meet some guidelines. They must have a minimum credit score of 620, for instance, and there are other, more specific conditions:

Screenshot from Veteransunited.com, May 2021

Commitment to its community

Applicants whose credit may still not be strong enough for a VA loan can take advantage of Veterans United’s Lighthouse Program--a free, no-obligation credit repair service to assist service members and veterans in reducing their debt and improving their credit profile. The Lighthouse Program is yet another example of a company culture that goes the extra mile to assist military families.

Better Mortgage review

Fast Closing Times

Better is a fast-growing digital-only mortgage company that, as of this writing (June 2020) is funding $700 million a month. Since the company's online experience effectively does away with loan officer commissions, lender origination fees, application fees, and underwriting fees, Better affirms that it saves each customer an average fo $3,500 in fees. Additionally, Better claims that it can close a mortgage in just 21 days, as opposed to the industry average of 42-50 days.

Screenshot better, May 2021.

How to Apply

Applying for a mortgage with Better is straightforward. You're first given the option of choosing between a new mortgage or a refinance. Once you've been directed into a pre-approval funnel, you're guided through a series of questions, such as how far along you are in your mortgage process, when you plan on purchasing, where you're looking, and the type of property you're interested in. Subsequent steps are fairly standard, such as a soft credit pull, registration on the site, and other relevant information. The interface is easy to follow, but if you run into any problem areas, each page has a convenient chat box for assistance. Otherwise, users can also call or email for help 7 days a week, from 9am to 9pm EST.

Fees

As we mentioned above, Better's entire premise is predicated on being able to obtain a quicker mortgage process for consumers, with fewer fees. Therefore, the company consistently offers competitive rates and substantially lower fees, helped in part by completely eliminating a brick and mortar infrastructure. They also offer a "Better Price Guarantee," which states:

"If we can’t beat a competitor’s price, we’ll give you $100. If you think another lender has a more competitive price, send us their loan estimate within one business day from the date on the loan."

Of course, this offer does come with some caveats, as seen in the accompanying fine print, but they're essentially what you'd expect. For instance, if you prove that Better and another company offered the same rate and loan terms, but the other company offered lower closing costs, you'd get that $100 check—but only if you present evidence that you took the other company's mortgage. And of course, Better will not honor the guarantee in any state where they don't originate loans.

Customer Experience

We especially liked that Better has up-to-date articles on the mortgage market, home buying, and refinance on its site, as well as several tools to help consumers navigate the complicated, and sometimes intimidating, mortgage process. They also have some explanatory videos which can be useful for more visual learners. And, you can even subscribe to rate tracking.

Screenshot better, May 2021.

On the other hand, Better is somewhat limited, still, in the number of states where it originates loans. Homebuyers from Nevada, Massachusetts, New Hampshire, Vermont, Virginia, Hawaii, and Minnesota aren't eligible. The lender also limits its offers to just new mortgages and refinancing, without including USDA or VA loans, or any home equity products. Finally, the very things that lower your costs (namely, the lack of physical locations) means that people who prefer to apply in person should consider other options.

Rocket Mortgage review

Best Online Experience

Screenshot Rocketmortgage.com, May 2021.

How to apply

The application process is simple, with questions leading consumers through each step. While a completely online experience may seem scary to some people, as though it may not offer enough support, Rocket does a good job of providing assistance, giving users the ability to chat in real time with a loan specialist.

The application process as we tested it is straightforward. It asks bite-sized questions about your loan needs and goals, personal assets, credit score, and other pertinent loan information in nine short sections. If you have all the answers at hand, the process takes less than five minutes. Keep in mind that the more accurate you are with the information you input, the more precisely the final loan package will be tailored to your needs.

Fees

Rocket Mortgage’s average origination fees are about 0.50% of the loan amount. Government-backed FHA and VA loans fees are slightly higher, but don’t go over 1% of the loan. These fees exclude any discount points you may want to purchase to lower your interest rate. Speaking of rates, it’s impossible to see prevailing rates on the Rocket website, as consumers can only access these after creating an account and entering some information.

Screenshot Rocketmortgage.com, May 2021.

Customer Experience

As is typical in the mortgage industry, customer sentiment about Rocket is mixed. Positive feedback emphasized the efficient process and good customer support, while negative comments cited an impersonal touch, which is not surprising due to the company’s large size and the very nature of its online experience. Rocket Mortgage does offer an online Learning Center that has very comprehensive resources consumers can use to learn about the mortgage process. Purchasing a home is difficult, and we think it’s a plus when companies address this need.

LendingTree review

Best Online Marketplace

When people want to purchase a home, they can either choose a direct lender (like a bank or a credit union), or they can submit an application to a broker that then places the loan with one of the lenders in its network. LendingTree offers a third option, as a third-party service that’s neither a broker nor a seller, but rather a marketplace. This means that after consumers fill out an application on LendingTree, it submits that data to its network of brokers and direct lenders. This leads to competition between them, potentially resulting in lower rates.

Application process

Screenshot from Lendingtree.com, May 2021.

Consumers can submit an application via LendingTree’s website or over their 800 number. After submitting your standard data--income, assets, education, debts, occupation and length of time at your job, and SSN--the company then performs a credit pull. Since LendingTree is not a lender, it doesn’t process the application any further, or have anything to do with approval or denial. Instead, it uses the borrower’s FICO score to select the lenders it will recommend from its network. These (up to 5) lenders then put together a preliminary quote, and contact prospective borrowers (usually over the phone).

Pros and Cons of Using a Marketplace

Shopping around for mortgage offers through a marketplace such as LendingTree can offer several unique advantages. Not only will you receive multiple competing offers from lenders looking for your business, you may also be able to parlay this competition into a lower rate by saying you got a lower quote from somebody else. The convenience of being able to play one lender against another, from just one application, is hard to overstate, as the company itself shows below.

Screenshot from Lendingtree.com, May 2021.

We also liked the amount of educational resources the company offers consumers, with helpful explanatory articles on different home purchase-related topics, tips, and reviews on their mortgage lenders.

However, LendingTree’s business model does mean you’ll have to go through the hassle of being contacted and (likely rather aggressively) marketed to by each of the five different lenders. This scenario happens enough that we found it to be a recurring theme across several different consumer review websites.

Consumers who are worried about hard credit pulls, due to having few accounts or a short credit history, may also want to tread with caution. Though LendingTree itself performs a credit pull, it’s possible that each of the lenders you’re matched with may also want to get one of their own. If these pulls all occur within a month, credit bureaus usually assume you’re shopping around and don’t count them individually. If not, they may cause a drop in your score. Of course, this depends on whether they’re hard or soft pulls. A hard credit inquiry takes place when a financial institution “pulls” your report from one of the three credit bureaus to check when you’re applying for a debt product (like a loan or credit card), and result in an automatic point deduction from your credit score. Soft pulls, on the other hand, have no effect on your score--they occur in situations such as when you check your own report, during background checks, and when you open a new bank account.

loanDepot review

Despite its early roots in the online lending industry (stretching back to the late 90s), loanDepot has a tangible commitment to face-to-face service, with over 150 affiliated loan stores around the United States. The lender has a good amount of loan types available: FHA, VA, conventional fixed and adjustable-rate mortgages, jumbo, and refinance.

FHA Loans

loanDepot is one of the largest originators of FHA (and VA) loans in the industry. J.D. Power’s 2018 Customer Satisfaction Survey found that loanDepot had a Power Circle rating of 4 out of 5, among primary mortgage originators, a score that translates to “better than most.” Since so much of the lender’s business is conducted in person, this leads us to conclude that customer service is a high priority for the company, and makes them a good choice for consumers looking for a personal touch.

Screenshot from loanDepot.com. Taken June 30, 2019.

They also offer the 203k fixer-upper loan we mentioned above, ideal for consumers who need to remodel or update their new home.

Applying with loanDepot

As we mentioned above, the lender has over 150 loan locations in the U.S. and is licensed in all 50 states and the District of Columbia. The focus on service extends to the innovative, as a fairly recent investment of $80 million in proprietary technology now allows the company to verify employment, income, assets, and even conduct credit checks, all digitally. This powers the mello smartloan™, in which loanDepot’s loan engines determine the options that are best for you, cost- or time-wise--in just seven minutes on average.

Screenshot from loanDepot.com. Taken June 30, 2019.

The idea is that the savings from the lower overhead costs can then be passed on directly to the consumer, allowing for better rates and deals. According to the company, it also reduces the time from application to closing by as much as 75 percent.

SoFi review

SoFi is another standout choice for best overall, though it’s particularly good for consumers with good incomes but not much money saved for down payments--they advertise great rates with as little as 10% down, for loans of up to $3 million.

Prospective borrowers can take advantage of the company’s soft credit pull to check what their rates might be, without it affecting their credit score. SoFi also looks at non-traditional income, making it a good choice for the self-employed or with restricted stock units (common in the tech industry).

Screenshot from sofi.com, May 2021

SoFi has 15- and 30-year fixed-rate loans, as well as a 7/1 ARM. The application process is straightforward, giving consumers a fully underwritten, quoted rate they can use as leverage when making offers on a property, showing they have the financial ability to purchase.

However, consumers should be aware that the lender doesn’t offer government-backed loans, like FHA, USDA, and VA, or home equity loans and lines of credit.

JPMorgan Chase Bank NA review

Best Bank Lender

JP Morgan Chase Bank NA's mortgage division is one of the top originators in the industry. Not surprisingly, they offer a wide variety of fixed-rate mortgages with terms between 10 and 30 years, adjustable-rate mortgages with 5-, 7-, or 10-year terms, as well as jumbo loans.

For borrowers who can’t make large down payments, Chase has two options aside from FHA and VA loans, called the Standard Agency loan and the DreaMaker mortgage, which allow down payments as low as 3%. Consumers who choose any of these mortgages, and purchase a home in a low- to middle-income area can also obtain grants from Chase of up to $2,500. And the lender also participates in several programs that offer assistance with down payments and closing costs.

Associated Costs

Chase does have rate lock, origination, and underwriting fees, which can significantly raise the total cost of your mortgage. However, the company is upfront about this and presents estimates for closing costs and lender or third-party fees when showing potential borrowers their rate and fee quotes. Existing Chase customers may also be eligible for certain discounts.

In addition, Chase promises customers an on-time closing in as few as three weeks or the company will provide $2,500 cashback.

How to Get a Mortgage with Chase

As one would expect with a large lender, Chase offers several different options for its customers’ mortgage process and application: online, at a local branch, or over the phone.

Screenshot from Chase.com, May 2021.

For online consumers, Chase offers two options--a shorter version with just basic information, or a longer form with personal data that gets them closer to a prequalification. Neither completely eliminates the need for real-person interaction, and borrowers will need to either get on the phone or go to their nearest branch to answer additional qualification questions. Documentation can be submitted and tracked electronically.

Learning Center

Chase provides robust mortgage education on its website. One of the reasons that the mortgage process can be stressful for customers (apart from the large financial commitment) is the sheer complexity of choosing the best loan for your needs. Much of Chase’s home purchase business is with first-timers, which may be why they’ve taken the time to flesh out their Mortgage Learning Center with articles, calculators, how-tos, and videos with customer testimonials.

Screenshot from Chase.com, May 2021.

PenFed Credit Union review

Best Credit Union Lender

Pentagon Federal Credit Union, or PenFed, has one of the largest selections of mortgage products on the market. The company also offers low- and no-down payment options and special programs for first-time homebuyers. Both homebuyers and homeowners seeking to refinance their mortgages can select from fixed- and adjustable-rate loans, conventional and jumbo loans, and government-backed VA and FHA loans. PenFed offers these many choices at lower-than-average interest rates. That's because credit unions are pledged to serve their customers first and aren't driven by corporate earnings goals. In addition, since credit unions aren't taxed the way private banks are, they are able to pass certain savings on to their members.

Applying for A Mortgage

The first step in applying for a mortgage through PenFed is to join the credit union. Membership is open to anyone. You don't need to be a member of the military or another organization to join. You'll fill out a series of short forms to apply for membership. It's worth noting that PenFed will perform a hard credit check on you if you apply for membership. That may result in a temporary dip in your credit score.

Screenshot from Penfed.org, May 2021.

While borrowers can apply for a mortgage on PenFed’s website, and upload documents, the credit union still isn’t completely online--and it’s likely consumers will have to pick up the phone at some point during the process. Despite having a limited number of physical branches, this reliance on customer service and real-person conversations makes PenFed great for people who want the human touch. This doesn’t mean that it doesn’t have good resources on its website--on the contrary, PenFed’s mortgage education section is one of the most robust we’ve seen. They make several calculators available to borrowers and offer clear explanations of the various types of home loans. These resources help customers narrow down their choices and make more informed decisions.

Screenshot from Penfed.org, May 2021.

Large Selection of Mortgage Products

PenFed has a wide array of mortgage products available, including fixed-rate loans with terms between 10 and 30 years, ARMs in a variety of lengths (including a unique 15/15 ARM) conventional and jumbo loans, and FHA and VA loans. Depending on the type of loan you apply for, credit requirements vary but you can get a mortgage through the company with a credit score as low as 620. In this way, PenFed opens the door to homeownership for a wide range of customers.

Freedom Mortgage review

Best FHA Lender

Freedom stands out due to its large menu of loan types. Mortgage products include conventional, ARM, and jumbo loans, as well as USDA, VA, and FDA ones as well.

Screenshot freedom.com, May 2021.

For this last option, the company offers not just the standard first mortgages, but also the FHA 203k loans, which factors in the cost of certain repairs and renovations into the total amount. Finally, Freedom also has loans for purchasing condos, financing investment properties, or building a house from scratch.

Online Application

Applying really is easy: the application is fully online, documents can all be uploaded and e-signed, and borrowers can even opt in to text message status updates. Consumers could, technically, complete their whole mortgage without ever talking to a person, should they so prefer (though there are loan officers available to help, as well). And if a loan doesn’t close on time, the company covers the first month’s mortgage payment up to $2,500, thanks to its “Close-on-Time Guarantee.”

Screenshot freedom.com, May 2021.

Transparent Rates

While many lenders that advertise low rates feature numbers that include discount point assumptions, Freedomclaims to be fully transparent about the rates it shows consumers. To get to these, potential borrowers need only click on the “Get My Rate” button and fill out some basic, non-personal information, and they are redirected to a live rate quote they can use for comparison purposes. Rates can be locked for up to sixty days free of charge, and if they go down, you may be able to take advantage of it via the lender’s “lock and lower” program. We also liked that they were clear about their flat-rate origination fee of $795 for most loans (Costco members may be able to lower that to $275).

CrossCountry Mortgage review

CrossCountry Mortgage is a full-service lender licensed in all fifty states, with 1,600 employees as of June 2019. Interestingly, the company operates under a franchise model with mortgage brokers, allowing it to expand its reach nationally, though it has a limited number of physical branches.

While it doesn’t specialize in VA loans per se, it does have good options within that program, particularly its Interest Rate Reduction Refinance loan (IRRL), also known as a VA Streamline Refinance. An IRRL allows consumers to refinance an existing VA ARM into a fixed-rate VA loan, or reduce your loan term to pay off your home sooner. While you’re not required to provide a certificate of eligibility, it should be presented to ensure you’ve used your VA entitlement.

Screenshot from Crosscountrymortgage.com, May 2021.

For its standard VA loans, CrossCountry offers competitive rates, and zero down payment, if the sales price doesn’t exceed the appraisal value. There’s also 100% financing without any mortgage insurance, and closing costs may be paid by the seller.

Ally Bank review

Ally offers conventional and jumbo loans for purchasing and refinancing. The company doesn’t currently provide any government-backed options such as VA, USDA, or FHA loans.

Screenshot from ally.com, May 2021.

Its conventional fixed- and adjustable-rate loans are fairly standard for the industry, but it does offer Fannie Mae’s HomeReady low down-payment program. Borrowers with low to moderate incomes may be eligible to purchase a home with just 3% down under this program. Ally's jumbo loans require a minimum down payment of 20%. Though Ally’s conventional loans require a minimum credit score of just 620, borrowers looking for a jumbo loan must have a credit score of at least 700.

Applying with Ally

After the 2008 financial crisis, Ally Bank became a fully online operation. Its mortgage branch, Ally Home, was founded in 2016 and also does business entirely online.

Interested borrowers can start the mortgage process either over the phone or by using Ally’s website. Online applicants are required to fill out a form that asks for a phone number, in addition to other standard information. Once this is submitted, candidates will receive a call from a loan officer, to discuss which combination of mortgage terms, interest rates, and discount points are best for their situation. This first approach leads to a prequalification, but consumers must still provide more information in a formal loan application. Once customers are prequalifited, they can proceed with their applications online or via email.

Screenshot from ally.com, May 2021.

Ally does charge some rates and fees —conforming conventional loans have a $995 loan origination fee. Customers who have an existing account with Ally may be eligible for a $500 discount on closing costs. The bank offers free rate locks for up to 75 days, though a longer period can be negotiated for an additional fee.

Alliant Mortgage review

Alliant Credit Union is another good choice for first-time homebuyers, with a 0% down payment program for some qualified borrowers, and just 3% down for others. There are no application or escrow waiver fees, which also helps keep costs lower. And Alliant’s origination fee can be as little as $995. However, just like PenFed, Alliant has a limited number of physical locations, so borrowers should be aware that their mortgage process will likely be online or over the phone.

Screenshot from Alliantcreditunion.org, May 2021.

Alliant Mortgages

Alliant offers a wide selection of fixed (10- to 30-year terms) and adjustable mortgage (3- to 10-year) loans, as well as its Alliant Advantage Mortgage (first-time home buyers can get 0% down for loan amounts up to $500,000; and 5% with no PMI for existing homeowners). The credit union also offers jumbo ARMs with low rates, and loans for non-conforming condos, a rarity since these cannot be sold to Freddie Mac or Fannie Mae and are therefore considered risky.

We liked that Alliant has a Ratewatch system that allows borrowers to input their preferred rate and get notified when it’s available. Overall, the union does a good job educating its members and showing its rates clearly and transparently, even offering a step-by-step PDF of the mortgage purchase process.

Screenshot from Alliantcreditunion.org, May 2021.

Movement Bank review

Best for Low Credit Scores

Movement Mortgage is a relative newcomer to the mortgage industry, having been founded in 2008 in the middle of the subprime mortgage crisis. It’s grown quickly, though, and currently has over 4,000 employees in more than 650 locations across the United States.

It offers a wide selection of loans, from the standard fixed- and adjustable-rate mortgages to jumbo and condo loans, as well as FHA, USDA, and VA programs. Interestingly, the lender also includes high-balance mortgages in high-cost areas, as designated by Fannie Mae.

We would like to see more easy to access information on rates, and more educational tools, as the current website is pretty bare bones and doesn’t really offer much by way of informing consumers.

Screenshot from Movement.com, May 2021.

Applying with Movement Mortgage

Almost all of your mortgage application with Movement is submitted electronically, either on the website or via their app, though there is a live customer service hotline available. Consumers looking for a preliminary rate quote will have to use that phone line, since the website won’t offer any rates unless potential borrowers complete the full application.

Screenshot from Movement.com, May 2021.

Movement has set some lofty goals for themselves as regards to the speed of their processes: six hours to underwrite, seven days to process, and one day to close. Considering that federal loan programs average one month to close, and some first-time homebuyer programs can take as much as 45 days.

Options for Low Down Payments

Movement’s mortgages cater to lower to middle-income borrowers by offering a large variety of loans with low down payments. These include its VA and USDA programs, which are sometimes no money down, Fannie Mae’s HomeReady Mortgage, and Freddie Mac’s Home Possible Advantage loan. Most government-backed loans have a minimum credit score of 620, but Movement also has options for consumers with lower scores--a conforming VA loan only requires a score of 580, for instance, and so does an FHA one.

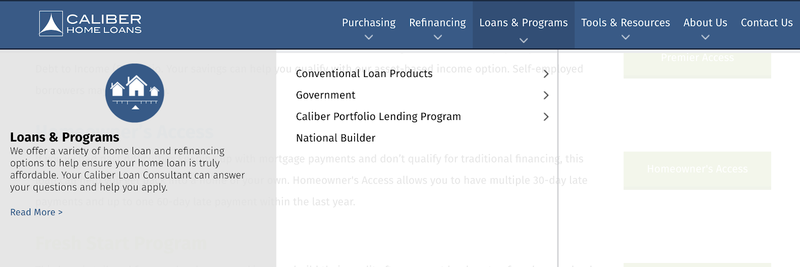

Caliber Home Loans review

A non-qualified mortgage alternative

Though a lesser-known player in the mortgage industry, Caliber Home Loans is a national lender that has been growing fast since its founding in 2013, as it emerged out of the merger between Caliber Funding and Vericrest Financial. It currently has one of the largest rosters of home purchase loans we’ve seen, with a wide array of conventional mortgages, government-backed programs, and the company’s own Caliber Portfolio Lending Program.

Screenshot from caliberhomeloans.com. Taken July 3, 2019.

This last category includes non-qualified mortgage options, such as the Professional Elite for the self-employed, Investor Access for real estate investing using property cash flow, Fresh Start for consumers who need to rebuild their credit after foreclosure or bankruptcy, Homeowner’s Access which allows late payments, and more.

Caliber aims to get to closing in as little as ten days after completing an application, thanks to a system authorizing the lender to verify borrowers’ income, bank statements, employment, and property details. They do explain that while this ten-day goal is their ideal closing time, some loans may not be suited for digital delivery of certain documents.

Pennymac Mortgage review

PennyMac also focuses on online and over-the-phone service, with few physical locations around the United States, though it’s one of the country’s largest non-bank mortgage originators, PennyMac has over 1.5 million home loan customers. While you can submit your documents electronically, and there’s online customer support, the company mainly services borrowers via several call centers staffed with loan officers who help guide consumers through the process. Each loan officer holds an average of 14 or 15 state licences, each of which requires continuing education for recertification-- keeping PennyMac’s representatives up to date with the industry.

Screenshot from Pennymac.com, May 2021.

The lender doesn’t have a minimum income requirement, making it a good choice for lower-income borrowers. However, consumers should be aware that PennyMac may charge an application fee and an appraisal deposit. Finally, we liked that the company offers resources and tools for homebuyers, such as calculators, a mortgage learning center, and a home value estimator.

Vylla review

Another good option for poor credit scores

Vylla is the forward-facing mortgage arm of the Carrington Holding Company, formed by the consolidation of Carrington’s real estate brokerage, retail mortgage section, and title business.

Screenshot from Vylla.com, May 2021.

Mortgage Menu

Similarly to Movement Mortgage, Vylla also offers a wide selection of loans for consumers with poor credit, or who have trouble getting together a substantial downpayment. Borrowers can choose between conventional purchase loans, jumbo loans, and programs from the FHA, USDA, and VA.

The company also has options for consumers who have bad credit or are self-employed, in the form of its only adjustable-rate mortgages: Flexible Advantage and Flexible Advantage Plus, with 5/1, 7/1, or 10/1 terms.

Minimum credit score requirements are really low at just 500, though this may vary according to the type of mortgage.

Application Process

Rather than have a comprehensive list of its mortgage offers, Vylla prefers to match consumers with the loan that best suits them. To that end, the company’s fully digital application process can start from three different points: “Affordability,” “Monthly Payment,” and “Purchase Price,” depending on where the borrower is in their purchase decision. This prompts a window to open asking for your zip code, and from there, you’re required to answer some pre-qualification questions regarding financial info (such as credit score, down payment, debts, and income). A few clicks later, Vylla matches you with its suggested loans.