Best Credit Reporting

Based on In-Depth Reviews

- 200+Hours of research

- 64+Sources used

- 32Companies vetted

- 4Features reviewed

- 9Top

Picks

- You are entitled to a free, annual copy of your credit report from all three bureaus

- Reports obtained directly from the credit bureaus are often more accurate than those from credit reporting services

- Each credit bureau will have a different version of your report

- You will often have to pay extra to see your credit score

How we analyzed the best Credit Reporting Companies

AnnualCreditReport.com

Must-use credit reporting service

Before using any other credit reporting service, it’s highly recommended that you get your full report from the three major credit bureaus—Experian, Equifax, and TransUnion--each of which is required by law to provide one free annual copy. Annualcreditreport.com is the only government-authorized site for this purpose. The process is simple- to order your report, just visit the site and fill out the request form. You can also call (877) 322-8228.

The site advises you to be prepared to answer personal questions “meant to be hard.” They even recommend that anyone who has reports from previous years to have them at hand. Apparently, the questions are designed to be very detailed so they can verify your identity before sending out your report. We tested this out ourselves, and didn’t find the questions to be particularly obscure, but perhaps this has more to do with our test subject’s relatively short credit history.

You can order one credit report at a time or simply order all three at once. It’s advisable to ask for all three of them at the same time, so you can compare them side by side and make sure the information is accurate.

Credit reporting services offered directly by Experian, TransUnion, and Equifax

Thanks to the Fair and Accurate Credit Transactions Act (FACTA) passed by Congress in 2003, everyone is entitled to a free yearly credit report from all three credit bureaus. These free yearly credit reports can be obtained through AnnualCreditReport.com; however, in addition to providing these free reports, the three major bureaus also offer their own credit reporting services.

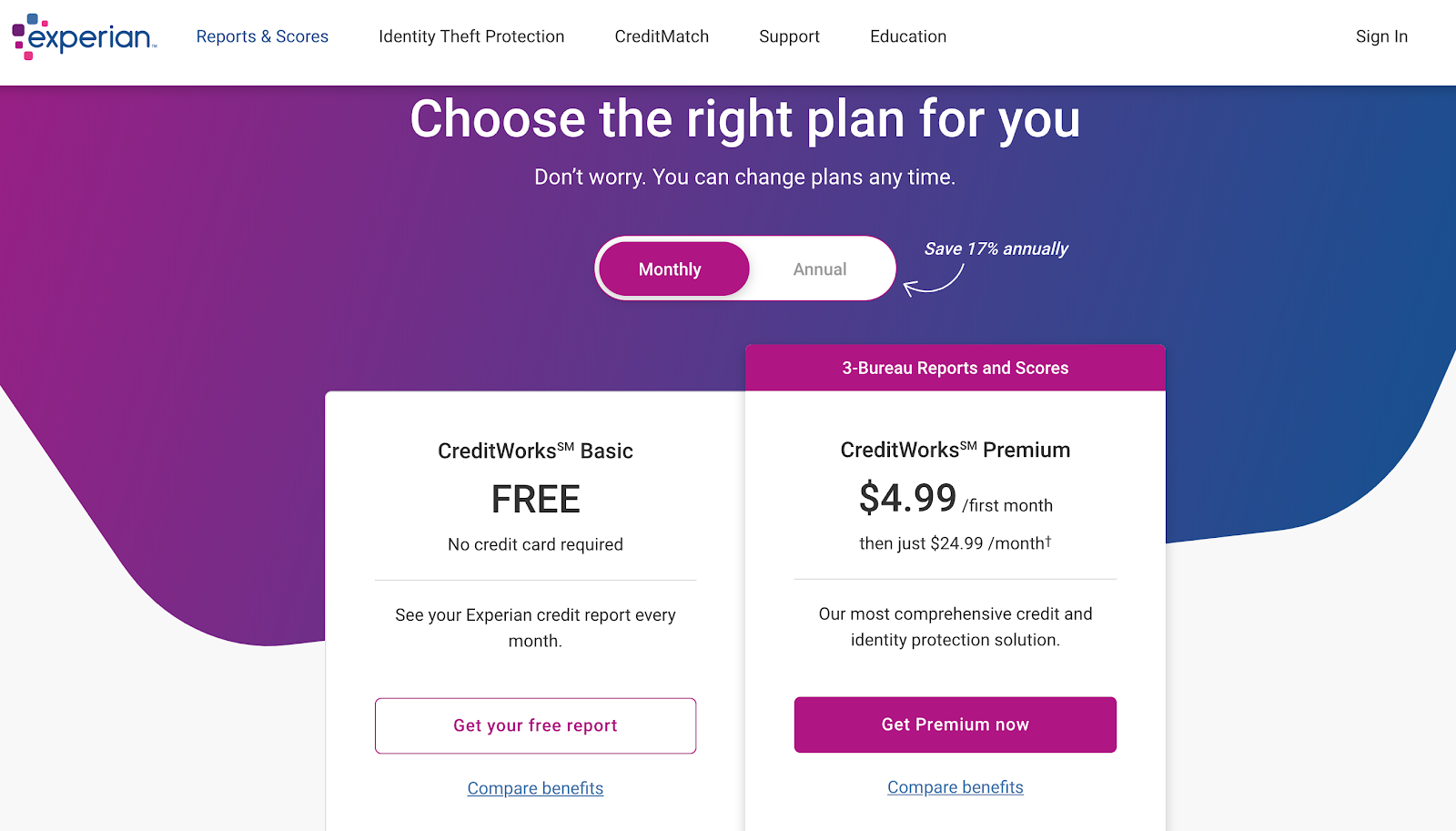

Experian

Screenshot experian.com, August 2019.

CreditWorks Basic

Experian offers a free credit reporting service called CreditWorks Basic, which includes:

· A summary of your accounts (open accounts, accounts that include late payments, closed accounts, and collections)

· Your overall credit usage (your total credit card debt against your total credit)

· Your total current debt (credit and retail cards, loans, collections)

· A list of public records (if you have any)

· A list of inquiries made into your report

Screenshot experian.com, August 2019.

This information updates every 30 days. However, this service will only provide a summary of your credit report, without the same level of detail included in the report you get through AnnualCreditReport.com (the website jointly operated by Experian, Equifax, and TransUnion which provides consumers with their annual free credit report).

Additionally, although the service says that they provide a FICO score, it’s important to note that what they show is the FICO Score range in which you fall—whether very poor, fair, good, very good, or exceptional.

Free Monitoring Alerts

Experian also includes free alerts, which will notify you of changes in your credit report, such as new inquiries, public record listings, if a new account is opened, or when you have a fraud alert placed on your record and a creditor is trying to verify your information.

Dark Web Triple Scan

The Dark Web Triple Scan, as they call it, checks if your social security number, phone number and email have been exposed in a data breach. It’s offered for free once you sign up. While that sounds like an excellent bonus, once we tried it, we realized it’s actually not that helpful.

In our test, our volunteer’s email was apparently found on seven “records on the Dark Web.” However, when we clicked on the entry to see more details about the issue, there was a distinct lack of information.

The final report simply shows a redacted version of the email and password that were allegedly exposed. It doesn’t mention the site where it was found or which breach exposed it. It only recommends that you change your passwords to make them stronger and that you upgrade to one of their paid services if you are interested in daily dark web scans.

Credit Marketplace

The service will also show you offers for credit cards based on your credit profile and spending habits. They feature a disclaimer saying that they do receive a compensation if you end up choosing one of the advertised offers, but state that the compensation doesn’t influence in what order or where the ads are placed.

Paid Services

There’s a paid version of CreditWorks Basic called CreditWorks Plus, which acts more like a credit monitoring service. Experian says on their site that the paid version provides daily monitoring of your credit report from the three major bureaus, a credit report locking feature, and identity theft monitoring as well as insurance. It costs $4.99 for the first month and then $24.99 for each following month your account remains open.

If you’re a free member, each time you sign in you’ll be asked if you want a trial of CreditWorks Plus. Be sure to press the “No, Keep My Current Membership” or cancel the trial period before it’s over if you don’t want to end up paying a monthly fee.

If you’re not interested in the free or the paid version of these services, there are two more ways you can see your Experian credit report for a one-time fee. If you have already used your free annual copy through AnnualCreditReport.com, you can order another one directly with them for $19.99, with your Experian FICO score as well. They also have a 3-bureau offer for $39.99 where you get your reports and FICO scores from all the bureaus.

If you ever want to cancel your account, there’s no way of doing it online. You have to call their customer service center.

FreeCreditReport.com: An alternative owned by Experian

Screenshot freecreditreport.com, August 2019.

FreeCreditReport.com shows up as a separate site from Experian when searching for credit reporting services, but they’re actually owned by the major credit bureau.

Their sign up process does have a difference. While Experian asks for only the last four digits of your social security number, FreeCreditReport.com asks for your full number. If you’re someone who’s skeptical about giving out their social security number, you’re better off simply creating your account with Experian.

We also noticed that if you’ve already created an account through Experian, you won’t be able to create one FreeCreditReport.com using the same login information. If you try, they’ll say your email address is already in use. Oddly, even though they say you’re already registered, they still won’t let you access your credit information because through Experian you only provide the last four digits of your social security number and they continue to ask for your full number.

Equifax

Screenshot equifax.com, August 2019.

Equifax doesn’t offer a free credit reporting service. Instead, it offers the report for $15.95 and, once purchased, you’ll have access to the report for 30 days.

Your credit report won’t be updated during this 30-day period. It will only show the information compiled on your report up until the day you purchased the offer. Equifax recommends you print out the report if you want to keep it past the offer’s end date.

This offer also includes your Equifax credit score and a summary of positive and negative factors that could be affecting your score. It is important to understand that the credit score that they will provide is the Equifax Risk Score. This is a scoring model developed by Equifax and it’s not the one creditors use.

The infamous data breach

In September 2017, Equifax announced that personal information from around 147 million people had been accessed by hackers. The bureau has faced intense criticism in their handling of the breach, particularly as it later surfaced that they had undergone another significant hack in March of the same year--and not disclosed it. Indeed, that same month the Federal Trade Commission (FTC) had alerted Equifax about a “critical security vulnerability affecting its ACIS database.”

The information exposed in the September breach included social security and driver’s license numbers, names, dates of birth, addresses, phone numbers, taxpayer identification numbers, and even credit card numbers.

Equifax agreed on a settlement of up to $700 million in penalties, and to provide help for the people affected by the situation. The FTC put up a page where you can check your possible benefits. They also include a link to the official site for submitting claims.

People were given the option of free credit monitoring by Equifax themselves for at least 10 years, or awards of up to $125 for monitoring by another bureau of their choice. The FTC recommends choosing the monitoring service by Equifax, since it includes monitoring for all three credit bureaus and $1 million in identity theft insurance, as well as identity restoration services.

TransUnion

TransUnion doesn’t provide a free credit reporting service. It only offers a credit monitoring service for a monthly fee of $24.95.

Other Credit Reporting Services

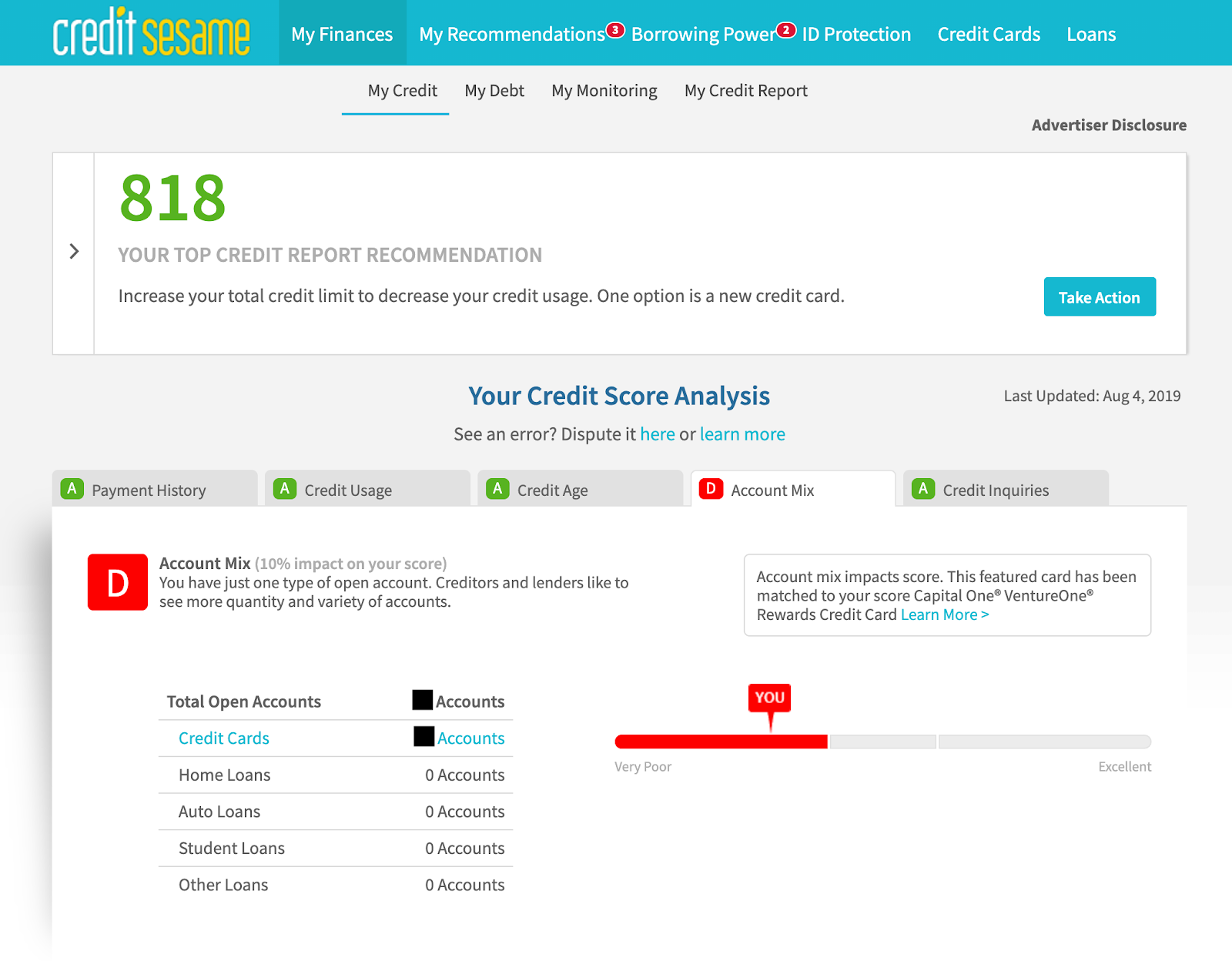

Credit Sesame review

Best for Its Free Extras

Screenshot creditsesame.com, October 2019.

Credit Sesame doesn’t offer a free credit reporting service per se. Instead, their free membership gives you what they call a credit report card based on your TransUnion report.

The report shows you a summary of your:

· Payment history: negative marks, if you have any (late payments, collections, foreclosures, bankruptcies)

· Credit usage: your total credit limit compared against your credit card debt

· Credit age: average account age, oldest open account, newest open account

· Account mix: how many different types of credit accounts you have open

· Recent inquiries: hard inquiries in the last 12 months

Screenshot creditsesame.com, August 2019.

It even assigns you a letter grade to each factor so you can get an overall idea of what you’re doing well and where you could improve.

The report card also shows your VantageScore 3.0, an overview of your open credit accounts—both credit cards and loans—and what percentage of your monthly income is going toward debt payments. Both your credit report card and VantageScore 3.0 should update monthly.

Free Monitoring Alerts and Identity Theft Protection

As a bonus, Credit Sesame includes credit monitoring alerts of new activity on your TransUnion report, which you can get via email or push notifications. You can also receive notifications when your credit score goes higher or lower than a number of your choosing.

They also provide a $50,000 identity theft insurance and access to identity restoration specialists at no additional cost. The insurance is meant to reimburse you for expenses and legal costs in the case you suffer from identity theft while you are a member.

This insurance may cover:

· Fraud or embezzlement

· Theft due to personal information being stolen by a person from whom you purchased goods or services

· Theft due to forgery or alteration of checks, drafts, promissory notes, or similar written orders meant to pay money. It also applies to written orders made by someone who, for any reason, was acting as your agent at the time.

· Information exposed due to a data breach

· Stolen identity over the Internet such as the unauthorized or illegal use of your name or social security number

The company includes a link to a summary of benefits in your account where they describe your insurance coverage in detail.

Essentially, you are not covered if your losses happened because you willingly gave out the information that was later used against you, gave out incorrect information, or if it was due to an investment venture or games of chance. It also doesn’t cover losses due to clerical mistakes by a financial institution or legal costs that exceed a $125 hourly rate.

The service also provides you with an Identity Theft and Fraud Customer Guide which includes letter templates and phone numbers to contact the major credit bureaus, your financial institution, government agencies or law enforcement, and inform them of the situation.

Paid services

If you’re interested in a full credit report, we recommend opting for one of the company’s paid memberships. They include everything the free membership does plus full credit reports and other perks:

· Advanced Credit ($9.95/month) provides daily credit score updates (from TransUnion), monthly credit score updates from all the bureaus, and full credit reports each month.

· Pro Credit ($15.95) offers the same benefits as Advanced Credit in addition to credit score monitoring for all the bureaus, and 24/7 access to experts that can help you correct report inaccuracies.

· Platinum Protection ($19.95) has the benefits included in all other memberships, plus 24/7 access to experts that help with stolen or lost wallet situations, black market website monitoring, public record monitoring, and social security number monitoring. This plan also offers insurance coverage of up to $1 million, a big upgrade from the $50,000 coverage offered by the free membership.

They also offer a one-time purchase of your TransUnion credit report for $9.95 or all three credit reports for $24.95.

Credit Marketplace

Like many other credit reporting companies, Credit Sesame has a marketplace where they show personalized credit card and loan offers, with a disclaimer saying that the compensation they receive for showing these offers may impact how they’re prioritized. For instance, if they show you a personalized list of credit cards, the first option on the list won’t necessarily be the best match for you.

It’s also important to note that the approval odds they may show are only an estimate which compares your credit profile with other users who chose the same offer. The same applies to the average and lowest amount of credit shown. These could also change depending on the creditor’s decision.

MyCredit Guide by American Express review

Most Detailed Free Credit Report

Screenshot mycreditguide.americanexpress.com, August 2019.

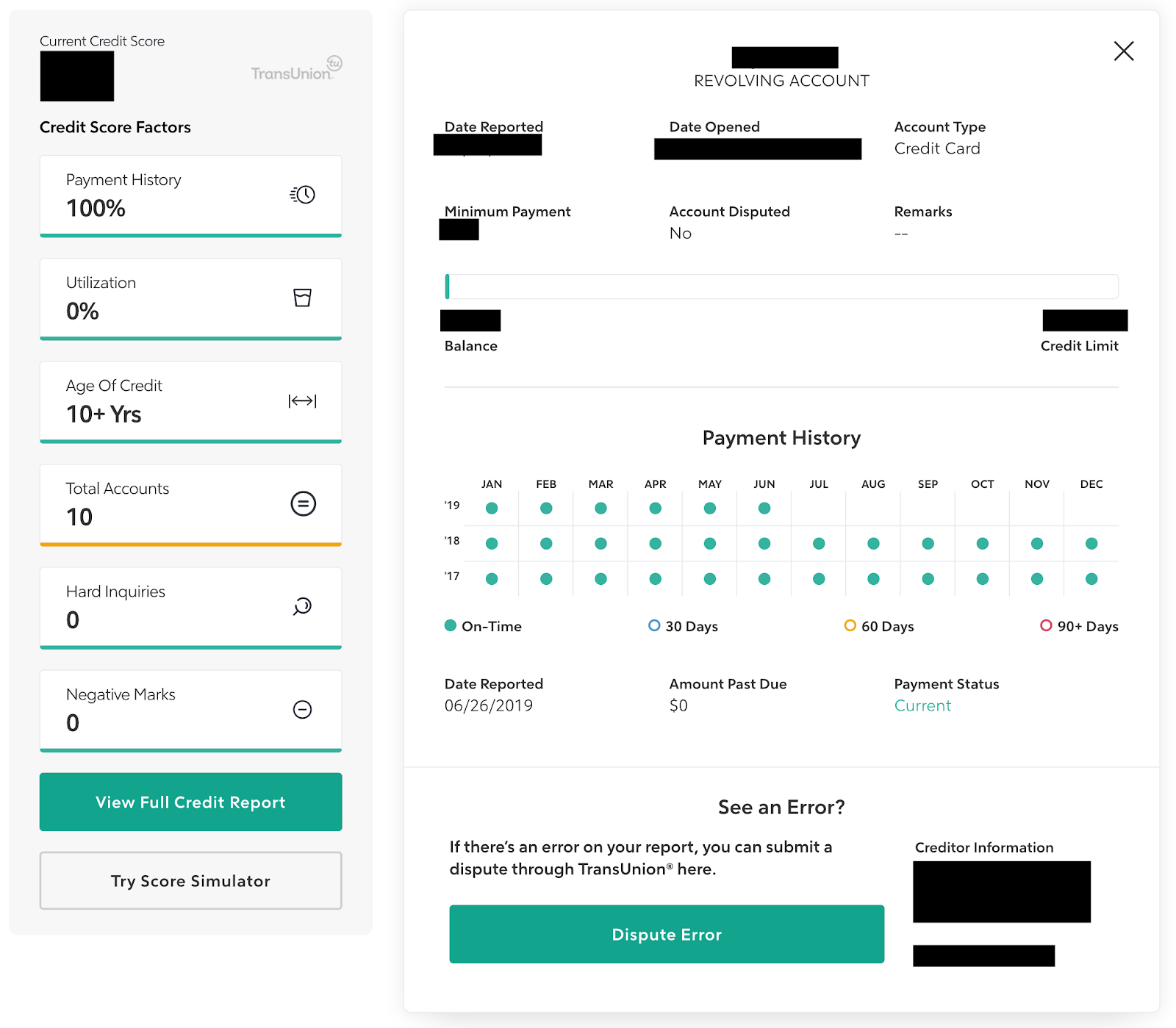

Although provided by American Express, MyCredit Guide is available to everyone, even if you’re not a cardmember. They offer the TransUnion credit report and VantageScore 3.0.

This service provided the most detailed free credit report out of the ones we tested. It includes an account summary of balances, payments, accounts (open and closed), delinquencies and derogatory items, public records, and inquiries in the past two years.

Each account, open or closed, has its own individual entry you can click on to have a more detailed look. Each entry includes:

· When the account was last reported to TransUnion

· Account number

· Account status (open, paid, or closed)

· Current balance

· Original balance

· Credit limit

· Monthly payment

· Date of last payment made

· Account type (credit card, mortgage, auto)

· If it’s a loan, its agreed paying terms

· If a loan was secured or not

· When an account was opened

· When it was closed

· Name of creditor

Screenshot mycreditguide.americanexpress.com, August 2019.

The personal information section of the report includes variations of your name that could’ve been used by your creditors. For example, a creditor may have reported an account under your current married name and others using your maiden name or a previous married name. If you see a name in there that you’re not familiar with, it could point to a possible case of identity theft.

The service includes a summary of the factors that may impact your credit score, email alerts about changes in your credit report, and a credit score simulator. The simulator estimates how your score may change by certain financial choices like getting a new credit card or canceling one, getting a loan, late payments, and inquiries.

If you continue using your membership over a period of time, MyCredit Guide stores your credit scores for up to twelve months and creates a trend line so you get an idea of your credit health’s stability.

While American Express may send pre-qualified credit card offers sometimes, the offers come directly from them, not from outside partners like other credit reporting services.

Rocket HQ review

Most Secure Free Service

Screenshot rockethq.com, August 2019.

This service is very similar to Amex’s MyCredit Guide. It also shows you your TransUnion credit report and VantageScore 3.0 for free.

They also update weekly, offer score simulators, and notify you of changes in your credit through email alerts—Rocket HQ sends push notifications too if you have their mobile app.

An interesting detail about Rocket HQ services is the security measure they use. It was the only service that sent us a verification email before letting us access the service. They’re also the only one that uses 256-bit encryption to protect stored information. Other services usually use 128-bit encryption.

Another difference between Rocket HQ and their competitors is the level of detail included in their credit reports. Each account entry in Rocket HQ details whether an account is a revolving or installment account, its type (credit card, mortgage, auto, student, or other loan), when it was opened, when it was reported to the bureau, the date it was closed, and the name of the creditor.

The way they show you your payment history for each account is convenient as well. They organize a calendar for each account and mark by color which month you paid on time or when you were late 30, 60, or 90 days. Finally, Rocket HQ also provides a score simulator.

Unlike other free services, they don’t show a single credit card or loan offer through their service. Other free credit reporting services show a ton of offers to their members—and sometimes even send them out through daily emails—so they can provide their free service in the first place. Rocket HQ shows you your credit report without relying on compensation from other companies.

Their site is also filled with resources like blog posts and guides on how to improve your financial health.

Screenshot rockethq.com, August 2019.

MyFICO review

Best for Paid Credit Reports

Screenshot myfico.com, August 2019.

This service is operated by the Fair Isaac Corporation, the company that created the most widely used credit-scoring system, the FICO score. Many people don’t know that there’s more than one FICO score--there are industry-specific ones (auto, bankcard, mortgage, to name a few), as well as the XD, NextGen, collection, and classic or generic score we’re more familiar with.

While FICO doesn’t offer any free credit report services, they do offer one-time purchases of credit reports that include nine or ten FICO scores that may be used by your creditor. All purchases will include the FICO Score 8, their most widely used version.

Their cheapest offer is called the 1-Bureau Credit Report and FICO Scores, which offers access to your credit report from the credit bureau of your choice, along with nine or ten different versions of FICO scores for $19.95. Their other offer is the 3-Bureau Credit Report and FICO Scores for $59.85. This one lets you compare your credit reports from all three bureaus and shows you 28 different FICO Score versions. Both offer access to your purchased report, or reports, for 30 days.

Both also offer an interest rate simulator that estimates how your FICO Score impacts interest rates and monthly payments; a score analysis to see the factors that are affecting your FICO Score 8; and a score simulator that explores up to 24 different scenarios to let you see, for example, how taking out a loan or getting a new credit card can lower or raise your credit score.

Still more possibilities

Credit Journey by Chase and CreditWise by Capital One

Both Credit Journey and CreditWise show you your VantageScore 3.0 and a summary of your TransUnion credit report for free.

The perks they offer are also very similar to the other services we tested, but be aware that they will ask for your full social security number upon sign-up. Most other credit reporting services only ask for the last four digits.

CreditWise by Capital One offers 256-bit security encryption, which is supposed to be safer than other services. But, on July 19, 2019 Capital One announced that around 100 million US customers’ information had been exposed in a data breach. The information included personal information from credit card accounts and social security numbers.

More insight into our methodology

As we started our research into credit reporting services, we realized that, although they all offered what seemed to be the same thing — namely, a credit report — what each one ended up providing might vary widely in both quality and usefulness. Credit bureaus (of which the three main ones are Experian, Equifax, and Transunion) are the entities actually in charge of collecting your credit information from lenders and creditors. Their reports contain the most complete information available. However, each bureau will likely have slightly different data, because every lender can choose which information it shares with which bureau, and which agencies they report to in the first place.

Credit reporting services unrelated to Experian, Equifax, or Transunion, on the other hand, simply partner with a bureau to show you a summary of their information on you. Further, we discovered that these services often team up with a single one of the three major bureaus, essentially just acting as a go-between, but allowing consumers to access their report more than once a year.

Credit reporting services are often confused with credit monitoring services, and indeed, many of the former also offer the latter. Both check your credit history, but credit monitoring is better suited to people who have been—or fear being—victims of identity theft. The tools these companies offer are specially designed to spot fraudulent activity and potentially prevent damage to your credit. They do this by monitoring social security numbers, public records, and the dark web.

To better choose between credit reporting services, we researched how each one operates, and which credit details they provide. We also tested them ourselves, by submitting information from one of our staff writers’ relatives to each service and comparing the results. We gave preference to those services that provided us with as much detail as possible, while still presenting the data in a format that was both understandable and user-friendly.

In order to determine what consumers were looking for when signing up for these kinds of services, we went through online forums and review sites where people discussed their main concerns and misunderstandings about credit reports. We noticed that many consumers weren't aware that most credit reporting services don't offer the same level of detail as the official credit reports from the three major bureaus. Many also didn’t know that these services usually only show information from a single bureau.

Based on these concerns, we picked services that are straightforward and transparent about what their membership includes, and that provide useful tools that can serve as stepping stones to better credit health.

Lastly, we talked to experts on credit building and consumer protection to help us better understand how the whole process works.

Plans & Pricing

We first looked into services that offered free memberships, as supplemental aids to the three free annual credit reports you’re entitled to from Experian, Equifax, and Transunion. The credit summaries included in these free memberships are helpful for keeping track of how well—or not— they manage their debt and how they can improve.

Most of the free services also offer premium plans with monthly subscription fees. However, we considered most of these premium packages were credit monitoring services, since they offer daily updates, reports of any inquiries or changes, dark web monitoring, and often, also check whether any account information is involved in data breaches.

Some services also let you purchase a copy of your credit report from one or all of the three major credit bureaus for a one-time fee, which may include a credit score. These offers could be helpful for people who are about to make a big purchase such as a house and want to be sure they get the best deal possible.

Report Details & Frequency

Free credit services are never as detailed as the report you get directly from the credit bureaus. Since we favored free memberships, we compared the reports they offered and selected the ones that provided the most comprehensive information.

We preferred free memberships that included personal information, open and closed accounts, account numbers, balances and status of accounts, payments, credit age and usage, derogatory items (late or missed payments, for example), public records, and inquiries.

Your credit report is constantly changing as creditors send new information about your credit accounts and payments to the major credit bureaus. However, not all creditors send information to the bureaus with the same frequency; and credit bureaus don’t update your credit report with the same frequency either.

We preferred credit reporting services that updated your information weekly over those that did so on a monthly basis. This should show you a more accurate view of your credit data, and how it can fluctuate over time.

Credit Bureau & Credit Scores

The three major credit bureaus are legally required to provide a free yearly credit report. A major advantage of credit reporting companies is their ability to allow for increased and more detailed supervision of financial health, by providing reports in a monthly or quarterly fashion. However, credit reporting services are not just meant for sending out credit reports and scores. In fact, the broad other half of what they do revolves around credit monitoring and support tools. Some of these functions are purely informative, such as credit score calculators and interest rate messengers, whereas others delve into security concerns, and send out alerts anytime a change is detected in one's credit.

If a customer determines that an alerted change is incorrect, then the credit reporting service's identity theft protection comes into play. Typical services include not only identity theft monitoring, but also insurance and restoration, as well as credit report error assistance, in order to catch potential identity theft incidents before they take place.

Monitoring & Extra Features

Credit reporting services sometimes include extra features such as monitoring alerts, or credit score and interest rate simulators. These can be great educational tools and a way to get an idea of how well your debt management strategies are working. They may also pinpoint what you can change to increase your credit health and get better offers on credit cards or loans.

Some services also include credit monitoring alerts, security scans, and identity theft insurance. Alerts are a great way of getting a heads up on any changes in your credit report and may even offer some identity theft protection. Each time there’s a change in your credit report, the service sends out an email or push notification alerting you of the change. If these don’t relate to your usual credit activity or are otherwise unfamiliar, it could mean someone else is using your personal information.

We also took a look into services that included identity theft insurance or security scans. These features are usually available only for premium members but they could interest people who fear their personal information might have been exposed to hackers.

Helpful information about Credit Reporting

Why check your credit report in the first place?

A study by the Federal Trade Commission found that one in five consumers had an error on at least one of their three credit reports. If they hadn’t reviewed or checked their credit reports, they would've never spotted the errors in the first place.

The inaccurate information on these reports could have lowered their credit score. Lower credit scores could have meant paying thousands more in interest rates. In fact, someone with a fair credit score could end up paying more than $40,000 in interest over their lifetime compared to someone with a very good credit score. Consumers with excellent credit scores could pay even less--in a nutshell, your credit is your financial calling card, it can both open and close doors.

Credit reports have also become essential tools beyond the financial world. Nowadays, your housing or employment status could be decided by your credit history; and maybe even your love life. A study by the Federal Reserve found that comparing your credit score with your partners’ can even help predict how stable your relationship will be.

So, it’s a well-known fact that excellent credit can benefit almost every area of your life. While reaching that milestone is not always easy, checking your credit report is a necessary step, and credit service companies can be a helping hand.

In the first place, using credit reporting services can help you become more credit-conscious. Since they update frequently, they can help you stay on top of your credit history, identify inaccurate information and get a better understanding of how you could improve your debt management strategies.

“Good credit is actually essential to access a lot of different opportunities in our day-to-day lives. We tend to think about the importance of credit as access to a mortgage loan … [but] credit impacts a lot of other aspects beyond just the ability to get a mortgage or other high dollar loans,” said Carmina Lass, Chief Program Officer at Credit Builder Alliance—a national nonprofit network that serves as a bridge between smaller nonprofit organizations and the major credit bureaus to help people with poor or no credit build financial health.

“They [credit reporting services] can serve a great purpose in terms of helping people stay connected to their credit history,” believes Lass.

Credit reports: What are they and who makes them?

A credit report is a detailed history of your credit usage and debt. They reflect your payment habits, how much you owe, and how long your credit accounts have been open.

Credit reporting agencies, or credit bureaus, are the companies in charge of collecting people’s credit information and creating their reports. These are then used by financial institutions, such as banks or credit card issuers, to determine if, how much, and on what terms they should extend credit to you.

The three big dogs of the credit reporting industry

Equifax, Experian, and Transunion are the most prominent credit reporting agencies. Their status results from the immense amount of data they store from consumers. According to the Consumer Financial Protection Bureau, they have credit information on more than 200 million adults, and receive data from approximately 10,000 different entities. It is also estimated that the major bureaus receive information on over 1.3 billion credit accounts monthly.

The major credit bureaus are not the only ones keeping tabs

In addition to the three major credit bureaus, there are also some lesser-known, specialized credit reporting agencies that focus on collecting information to meet the needs of specific industries. Last January, the Consumer Financial Protection Bureau published an updated list of more than 40 reporting agencies in the United States. These are some of them and what they may have on you according to the CFPB:

Innovis: their reports are very similar to ones created by the three major bureaus. The difference will mainly be the amount of information they have about your credit history. Not all financial institutions will report to Innovis like they do with Equifax, Experian, and Transunion.

ChexSystems: checking and savings account activity.

Certegy: check writing histories.

LexisNexis Risk Solutions: real estate transactions, ownership data, liens, judgments, bankruptcy records, professional license information, and historical addresses on file.

Microbilt/PRBC: credit, bill payments, employment, bank account information, property records, court judgments, address, and phone numbers.

CoreLogic Teletrack: payday lenders, rent-to-own businesses, furniture stores that offer financing, auto finance, and leasing companies.

Clarity Services: a part of Experian. They state on their site that their “data source is derived from a variety of financial service providers, including auto financers, check cashers, prepaid card issuers, short-term installment lenders, peer-to-peer microlenders, small-dollar credit lenders, online small-dollar credit lenders, telecommunications, and many more.”

National Consumer Telecommunications and Utilities Exchange (NCTUE): is operated by Equifax. They state that they collect “data such as payment and account history, reported by telecommunication companies, pay TV, and utility service providers that are members” of the agency.

The Fair Credit Reporting Act

The Fair Credit Reporting Act (FCRA) is a federal law that regulates how credit information is managed and collected by consumer reporting agencies. It also establishes who can have access to your credit report and under what circumstances. Basically, it aims to make sure the information included in credit reports will always be accurate and used fairly.

The law was passed in 1970 to stop credit reporting agencies like Retail Credit Company—Equifax’s original name—from including information regarding social, political and even sexual preferences in people’s credit reports.

Since then, three acts have helped strengthen the FCRA: the Fair and Accurate Credit Transactions Act of 2003, the Dodd-Frank Act of 2010, and The Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018. Together they have given people more control over the security and accuracy of their credit reports.

The Consumer Financial Protection Bureau (CFPB) The Federal Trade Commission (FTC) are in charge of enforcing the act.

Your rights under the FCRA

Sure, the FCRA--along with the three supplementary laws of 2003, 2010, 2018--dictate how consumer reporting agencies collect and share information, but sometimes mistakes are made and rules are broken. If you want to stay on top of your credit report, this is a summary of your rights according to the CFPB:

You are allowed to see what is in your credit report: You are entitled to get a free copy of your credit report once a year from each major credit bureau, on request. Specialized credit reporting agencies must also provide you with a yearly report. You can also ask them for your credit score, but this won’t be free. Make sure to ask which credit score they’ll provide. It’s possible it won’t be the one used by creditors.

You are entitled to an additional free credit report in special instances:

-

An unfavorable action is taken against you based on information in your report

-

You’re a victim of identity theft

-

The file contains inaccurate information

-

You’re on public assistance

-

You’re unemployed and expect to apply for employment within 60 days

You can dispute inaccurate or incomplete information: Both credit reporting agencies and the entities (lenders or creditors) that provide them with information must correct inaccurate or incomplete information. If you discover an error and notify it, they must investigate the situation. If the information reviewed is in fact a mistake, it must be eliminated from the report, typically within 30 days.

You may place a security freeze on your report for free: A security freeze prevents creditors from opening lines of credit without your authorization. This is especially useful if you are a victim of identity fraud. You can also place a fraud alert, which remains on your report for a year and requires that creditors take extra steps to verify your identity before opening a new credit line in your name. The fraud alert can be extended for 7 years if you are a victim of identity theft.

The only person that doesn’t need permission to access your report is you: Your credit report can only be accessed by people or companies that have a valid need to see it and have your written consent. For instance, creditors, insurance companies, employers, and landlords may need to check your report before doing business with you.

You can opt out of receiving prescreened credit offers: You know those credit card offers you receive without asking? You get these because credit bureaus include your information on a list provided to creditors. These offers are based on certain creditworthy criteria you may have. You may opt out of receiving these offers by visiting www.optoutprescreen.com or calling 1-888-5-OPT-OUT (1-888-567-8688).

You can file legal action against violators: If a credit bureau, consumer reporting agency, employer, or any person or entity you are doing business with violates the FCRA, you might have the right to sue.

Banks are not the only ones who care about your credit history

Financial institutions are not the only ones who use your credit report to figure out how trustworthy you are when it comes to paying your dues. Insurance, utility, cellphone, internet companies, and even government agencies, may also want to check it out.

Your credit history helps these companies determine how reliable you will be with payments, if they should ask for a security deposit, how much to charge you for an insurance policy, or if you are eligible for government welfare.

“If you have poor credit or no credit at all you may have to pay a deposit for those types of services that somebody with good credit or excellent credit wouldn’t have to pay,” mentioned Lass.

It’s also likely that a landlord or property manager will ask for a credit report before renting out a property. “Many landlords look at credit history as one of their factors in terms of acceptance an applicant,” confirmed Lass. A survey from SmartMove, a tenant background screening service offered by Transunion, found that 90% of landlords run credit checks on prospective tenants.

Employers might also be interested in taking a look. A survey by the National Association of Professional Background Screeners, in partnership with HR.com's Research Institute, found that 16% of employers check every candidate’s credit report, while 31% check at least some candidates.

Potential employers are likely to be particularly interested in your report if you’re applying for a job in finance, for instance. After all, no one wants their money being managed by someone who seems like they don’t manage their own very well. Keep in mind though, employers are required by the FCRA to have your written permission before checking.

If you’re denied employment, a lease, an offer, or are given a worse deal than the one you originally applied for because of your credit report, you must be notified. The FCRA requires that the notification explain the reason you were denied and which credit bureau generated the report used against you. You also have the right to request a free copy of the credit report that was used, within 60 days of being informed.

Mastering the basics

Getting to know your credit report and monitoring it closely is the first step towards better financial opportunities. However, if you need to build your credit and/or significantly bump up your score, it’s important to master the basics— specifically, how to read a credit report. Also, what credit scores are, how they’re calculated, and what it takes to have an excellent one.

So, what are credit scores then?

As we’ve mentioned previously, a credit score is a three-digit “grade” credit bureaus give you based on your credit history. Since this grade can determine so many of your life’s big financial decisions - from buying a home to getting the job you want - it’s important to check your credit history regularly and be aware of what’s being taken into account when calculating your score.

Many people aren’t aware that they don’t have just one credit score, just as they don’t have one single credit report. FICO, for instance, has over 50 distinct credit score types corresponding to different industries--and there are other, lesser-known and lesser-used scoring models as well (TransRisk, Experian’s National Equivalency Score, Credit Xpert Credit Score, CE Credit Score, and the Insurance Credit Score used by insurers).

Credit scores — at least in the two most popular scoring models, FICO and VantageScore —usually range from 300 to 850, with 300 considered extremely poor and 850 excellent. The higher the number the more creditworthy you’re thought to be. People in the higher end of the scale will not only qualify for most loans and credit cards, but will also be offered the lowest interest rates.

FICO Score

The FICO Score was created by the Fair Isaac Corporation and is considered the most widely used credit score model. In fact, FICO states they are “used in more than 90% of lending decisions.”

FICO has developed different versions of their score throughout the years. As a result, you have more FICO scores than you probably imagine.

The company says their most widely used version is the FICO Score 8 even though Score 9 is already available. These two versions analyze your credit report information from the three main bureaus, and come up with a single score.

Other FICO scores are developed for specific industries. The FICO Auto Score aims to provide a more comprehensive score for auto-financing, for instance, and the FICO Bankcard Score is for credit card applications.

These are very similar to the primary score models with just a few modifications which are supposed to measure the risks commonly associated with specific industries. Each model is itself divided into several other versions, depending on which credit bureau information it uses.

There’s also the FICO Score 3 which is used primarily for credit card lending.

Beacon 5.0, FICO Risk Score Classic 04, and Fair Isaac Risk Model v2

These three are somewhat commonly used additional FICO score versions. Unlike Score 8 which uses all of your credit reports, they each take into account the report of only one bureau.

The Beacon 5.0 uses your credit report from Equifax, the FICO Risk Score Classic 04 from TransUnion, and the FairIsaac Risk Model v2 from Experian.

The FICO Score 2 (also known as Fair Isaac Risk Model v2) only uses your credit report information from Experian. FICO Score 4 (also called FICO Risk Score 04) uses data from TransUnion. Finally, the FICO Score 5 (also called Beacon 5.0) is based on Equifax.

VantageScore

VantageScore was developed through an alliance between the three major credit bureaus. Unlike FICO, there are only two versions of the system currently in use: VantageScores 3.0 and 4.0. The 3.0 version is the most used score, and it’s also the one shown by most free credit reporting services.

VantageScore fulfills the same purpose as a FICO score—grading your creditworthiness—but they do present some differences when it comes to their calculating formula.

VantageScore only asks for about a month of credit history and one account with registered activity within the last two years. They also treat late payments a bit differently— FICO treats them all equally, while VantageScore will be tougher on late mortgage payments.

To calculate your score, FICO requires that you have at least a six-month-old credit history. They also require that at least one of your accounts have some activity registered with one of the major credit bureaus within at least six months.

Educational Credit Scores

The three major credit bureaus also have their own scoring models. Equifax has the “Equifax Credit Score”, Experian has the “PLUS Score”, and TransUnion has the “TransRisk New Account Score.” According to the CFPB, these credit scores are not typically used by creditors and are only meant for educational purposes.

So, which score will my creditor use?

There’s no specific way of knowing which credit score your lender or creditor will actually use--most will look at the versions they consider best fits their needs.

Lass recommends asking your creditor, “the best way [to know]… is to just inquire with the creditor to see if they would share what credit database they’re pulling from and what score they're using to evaluate.” However, be aware that there’s no guarantee that they will share this information with you.

It’s likely you’ll only find out which score they used if you’re denied an offer you applied for and are sent the rejection notice required by law.

Lass recommends that people educate themselves about the different kinds of credit scores available before buying one through credit reporting services, “the score that they are getting might not be the same score that their creditor is using…That doesn’t mean the score is inaccurate, but it’s different.”

Back in 2017, TransUnion and Equifax were fined by the Consumer Financial Protection Bureau for tricking consumers into buying credit scores without being clear regarding which one they were selling and how useful they really were. “You can use those [scores] for tracking your general credit progress, but if you’re about to apply for credit … it’s good to figure out what score the creditor is using,” advised Lass.

FICO outlines the versions of their scores most commonly used in certain credit lending decisions:

· Most widely used: Score 8

· Auto-lending: Score 8, 2, 4, or 5.

· Credit cards: Score 3 or Bankcard Score 8, 2, 4 or 5.

· Mortgages: Score 2, 4 or 5

Another good tip, if you’re searching for the best mortgage options, is to concentrate on your FICO score. A 2018 report found that there’s been an increase of more than 20% in VantageScore usage, but this rise doesn’t apply to the mortgage market.

More ways of getting your credit score besides credit reporting services

The CFPB made a guide to inform consumers of how they can get free access to their credit reports. The guide outlines, credit card issuers and other creditors that offer free credit to their customers—they sometimes also offer scores to the general public. There are also nonprofit credit and financial counseling services that offer free credit scores.

As always, make sure to determine which credit score they offer.

Excellent Credit: What actually goes into it?

Credit reports and scores will inevitably vary from person to person, but there are some steps everyone can take to improve their credit health. Both FICO and VantageScore consider the same factors when scoring you. Learning what these factors are, and how to manage them, can help almost anyone build a good credit history or raise their score.

In addition to making a habit out of checking your credit reports regularly, you have to really understand what it includes, and how that information can make or break your credit score. Following, we outline some simple steps to take to raise your score.

Pay your bills on time

This one might seem obvious, but it’s crucial. After all, credit scores are meant to determine how trustworthy you are in paying back what you owe. If you have a lot of missed payments, creditors will see you as a risk. Period. Consistently paying your debts on time is a must.

Creditors report a late payment once if it’s 30 days late. After that, late payments will be marked as 90, 120, or 150 days late. The most severe late-payment mark is a charge-off. A charge-off happens when so much time has gone by that creditors think you won’t ever pay them back.

If you do miss a payment, not to worry! Pay it off as soon as possible and try not to miss another one again. Creditors won’t usually hold a single missed payment against you, and your credit score will rise again once you get back to your healthy credit habits.

The 30% or less rule

Using 30% or less of your available credit makes you stand out before creditors. This shows that even though you have a larger sum available, you don’t need to tap into it. The implication is that you manage your money well, whereas someone maxing out their cards will likely end up with multiple late or missed payments.

The goal is to use 30% or less of your available credit limit across all your cards and on each one individually. For example, if you have five credit cards, and together they add up to $10,000 in credit limits, you should aim to use $3,000 or less. Take the same precautions with each one of your credit cards as well.

There are financial experts that believe using 10% or less of your available credit is even better. In fact, research from FICO found that Americans with credit scores between 800 and 850—the exceptional score range—used around 4% to 10% of their credit.

Mix it up

Creditors like to see how well you manage different kinds of debt. By paying up different kinds of debt responsibly, you show them exactly that.

There are two types of credit accounts: revolving accounts and installment loans. Revolving accounts give you access to a certain amount of credit and, as you pay it back, you can keep drawing from it again and again. Your credit limit can increase or decrease over time depending on your payment history. For example, a credit card issuer could decrease your credit limit if you have a history of paying late, or they could offer you a higher credit limit if you’ve made all your payments on time.

Ideally, you could pay your balance in full every month (which will help you raise your credit score), but you can also make just the minimum payments required by the creditor. The latter option, however, means that you’ll end up paying much more due to the accrued interests. Aside from credit cards, personal lines of credit and home equity lines of credit (HELOC) are also revolving accounts.

Installment loans, on the other hand, let you borrow a certain amount and make fixed payments over time until both the principal and interest are paid off. Once you send the last payment, your installment loan account is automatically closed. Home mortgages, home equity loans, auto loans, student loans, and personal loans are all installment loans.

Oldies are definite goodies (as long as they don’t have a dark past)

Even though it’s not as important as paying on time or how much of your credit limit you use, the length of your credit history does matter. Your credit age is analyzed based on an average of how long all of your accounts have been open, when you opened your oldest account, and when you opened your newest account. They also consider how long it’s been since you’ve used your accounts. A long history of positive credit usage across your accounts will speak highly of your debt-management habits.

Open a couple of new credit accounts, but not too fast

Yes, having different types of credit accounts helps boost your credit, but don't rush to open up a lot of them in a short amount of time. This is even more important if your credit history is short. Opening up new credit accounts lowers your average credit age.

Additionally, trying to open a new credit account results in hard inquiries. A hard inquiry, or hard pull, happens when a creditor takes a detailed look into your credit report to decide if they want to give you a new line of credit or not. Too many hard inquiries on your credit report over a short period of time could make creditors think that you’re eager to open new credit accounts because you’re having money trouble.

-

Rate shopping exception:

When you want to buy a house or car, you might search around for a loan offer that best fits your budget. Credit reporting companies get that. To deal with this, they classify hard inquiries done in a short period of time as “rate shopping.”

FICO’s rate shopping period is 45 days. In this period you can search for a mortgage, auto loan, or student loan—to name just a few installment loans—without worrying about a drop in your score. You can’t search around for the ideal credit card though. VantageScore’s period is smaller—14 days—but they do allow rate shopping for credit cards.

Inquiries done during these time frames would count as a single inquiry.

Dispute anything that shouldn’t be in your report

Even if you manage your credit accounts diligently, keep in mind that your credit score could be seriously affected if incorrect or inaccurate information is included in your credit report.

“It’s worthwhile to find out what information the various credit bureaus have about you and whether or not it's accurate,” remarked Susan Grant, Director of Consumer Protection and Privacy at the Consumer Federation of America—an association of non-profit consumer organizations whose stated goal is to advance the consumer interest through research, advocacy, and education.

Some common mistakes found in reports include:

· Personal information unrelated to you

· Credit accounts that are not yours

· Duplicate accounts

· Late payments that you actually made on time

· Closed account reported as open

· Incorrect account balance

Whatever the case may be, if it’s wrong, it can be disputed and it must be deleted from your report. To dispute mistakes, the Consumer Financial Protection Bureau advises to first contact the credit bureau which produced the report where you found the mistake. Then, you should contact the creditor who provided the inaccurate information.

It’s possible the negative information was added by mistake, but it’s also possible that it might be due to more serious situations such as identity theft or fraud. Identity theft complaints were the second most received by the FTC in 2017. If this is the case, you could benefit from identity theft or credit monitoring services.

Make sure old, negative information is removed

If for any reason you fail to make payments on a credit card or loan, that information will be added to your credit report even if you ended up paying later on. The late payment—or delinquency—will continue to appear on your credit report for seven years. Foreclosures also stay on your credit report for seven years.

If an account does not receive a single payment for over 180 days, it’s going to be marked as a charge-off. Charge-offs are accounts that creditors consider won’t be paid—at least not in the near future. By this point, your account has been probably sold to a debt collector. Just like late payments, charge-offs also remain on your credit report for seven years.

Bankruptcies are the most troublesome of the negative information bunch. They stay on your report for up to ten years.

Judgments and tax liens can be included in credit reports but, since 2017, credit bureaus changed their requirements for including them. If the information can’t be verified with name, address and Social Security Number (or date of birth), it won't be included in an individual's credit report. In fact, many people experienced a boost in their credit scores as judgements and tax liens were removed from their reports because they couldn't be verified.

When you go through your credit report, make sure to verify the dates of any negative information that may show up. If it’s outdated, contact the credit bureau who is reporting the information to have it removed.

Take Advantage of Credit Freezes and Fraud Alerts

The Equifax data breach is evidence of how our information is never entirely safe, but there are tools we can use to take matters into our own hands and make it less vulnerable. It’s always a good idea to be extra careful, especially when it comes to sensitive information like the one included in your credit report.

“While it’s very important that credit bureaus have security, it’s also important that consumers have good tools to use in case their information is exposed,” said Grant.

Credit freezes and fraud alerts are essential credit security tools. Grant considers them one of “the best protection consumers can have against … [some of] the most common types of identity theft.”

-

Credit freeze: keeps creditors from accessing your credit report. Since no one can access your report, no one can give you new lines of credit. So, if someone stole your identity and tried to open a credit account with your information they wouldn't succeed. When the time comes when you need to access your report, you can provide the PIN you chose when initially placing the freeze and it will temporarily unfreeze. Unfreezing your report is sometimes also called thawing your report.

-

Fraud alert: when a fraud alert is placed on your report, creditors must take extra steps to verify your identity before opening any new credit account on your name. If someone tries to open an account with your information, a creditor must contact you and inform you of the situation. Fraud alerts remain on your report for one year. If you were a victim of identity theft, that period can be extended to seven years. Credit bureaus also offer credit lock services. Just like freezes, locks block access to your report whenever they are enabled. Grant explained “there’s not really a difference” between what each one does.

The only difference between a lock and a freeze is how they are placed and lifted. Credit locks are advertised basically as being user-friendly credit freezes. Instead of contacting the bureaus to have them freeze or thaw your report, you can do it yourself through the bureau's site or mobile app.

The issue with credit locks is that they are not enforced by law, so each credit bureau manages their service on their own terms. The services sometimes include arbitration clauses and class-action waivers that make you give up your right to sue if the lock service ever fails to do what it’s supposed to.

Additional credit security tips

Aside from regularly checking your credit report, Grant recommends checking your monthly account statements for any irregular payments. “Monitor your own accounts… If there’s any problem with a charge you didn’t make or an amount being incorrect, you can correct that with the creditor so they can insure that the information they share with the credit bureaus is accurate.”

Making sure your personal computer has an adequate security system installed is also necessary. “If you’re going to be checking any kind of financial accounts online you want to make sure that fraudsters can't hack into your computer,” mentioned Grant.

Lastly, you must be vigilant of what information you share as well as with whom. “You have to be very careful yourself no to potentially expose your information to account takeovers; … you also have to be vigilant against things like phishing,” said Grant.

What To Watch Out for With Credit Reporting Services

Check Your Credit Report From Each Bureau

Free credit reporting services provide information from a single credit bureau. Remember that there are still two other reports you absolutely have to check out. It’s possible the information across all three reports could be slightly different.

Creditors don’t always send your information to all the bureaus. It’s possible they don't even send your information to any of the three. This is the reason why your TransUnion report, for example, could be showing one additional open credit account than the one from the other bureaus.

Most importantly, the credit report you’re seeing could be squeaky clean while the one from the other bureaus includes inaccurate or outdated information. These errors could potentially affect your credit health. It’s of utmost importance to compare the information across all three reports. Anything that shouldn't be there can and must be removed.

Keep in mind, though, that information won't be removed if you can't provide enough evidence to the bureaus of its inaccuracy.

Read the fine print

There are many credit reporting services out there that aren’t completely clear about their advertised offers. The “get your credit reports and scores from all three bureaus for $1” is one of those confusing offers.

People jump at the idea of such a cheap offer without realizing the $1 payment is actually just covering a 7-day free trial. Once that period ends, the companies begin charging a subscription fee, often upwards of $20 a month. If you don’t check your credit card statements regularly, you could end up paying a lot more than that one dollar.

We recommend you avoid credit reporting services that offer trial periods if you’re not sure how their trial cancellation policies work, or if you’re likely to forget to cancel it. We found numerous reviews online where people said they tried cancelling their trials online and over the phone and still ended up getting billed.

Another important detail is to be clear on what type of credit scores they’ll show you.

FAQs about Credit Reporting

Does using a credit reporting service affect my credit score?

Am I still entitled to a free annual credit report even if I got one through a credit reporting service?

Our Credit Reporting Review Summed Up

| Company Name | The Best |

|---|---|

| FreeCreditReport.com Credit Reporting | Overall |

| MyFICO Credit Reporting | For 3 Bureau Official FICO Scores |

| Identity Force Credit Reporting | For Identity Theft Protection |

| TransUnion Credit Reporting | Personalized Debt Analysis and Reporting |